Is Akamai Technologies (AKAM) Undervalued On Its $1.8b AI Cloud Deal?

Akamai Technologies, Inc. AKAM | 0.00 |

Akamai Technologies (AKAM) is back in focus after securing a US$1.8 billion, seven-year cloud computing agreement with an AI startup, the largest customer contract in the company’s history.

The recent 1-day share price return of 3.88% and year to date share price return of 38.91% sit against a 30 day share price decline of 20.95%. The 1 year total shareholder return of 48.49% points to momentum that has been building over a longer period despite the stock being dropped from two Russell 1000 indices and a mixed stretch of short term trading.

If Akamai Technologies’ AI cloud deal has caught your attention, it could be worth widening your search to other AI infrastructure plays via the 51 AI infrastructure stocks

With Akamai Technologies trading at US$118.21 and Oppenheimer arguing that its AI cloud potential is not fully reflected in today’s valuation, the key question is whether the recent pullback leaves a genuine opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 25.8% Undervalued

With Akamai Technologies at $118.21 against a widely followed fair value anchor of $159.30, the current narrative frames today’s price as a material discount built on AI infrastructure and security demand assumptions.

The proliferation of AI applications requiring secure, ultra-low-latency infrastructure benefits Akamai's globally distributed platform, evidenced by new AI Gateway and Firewall for AI offerings, which positions the company to capture new AI-driven workloads, supporting both future top-line growth and potentially higher net margins via value-added solutions.

Read the complete narrative. Read the complete narrative.

Want to understand why this fair value sits well above today’s price? The narrative leans heavily on compounded revenue gains, a fatter margin profile, and a premium future earnings multiple. Curious which assumptions really do the heavy lifting in that model?

Result: Fair Value of $159.30 (UNDERVALUED)

However, Akamai Technologies still faces real pressure if capital spending on AI infrastructure hits margins harder than expected or if a few large contracts fail to ramp up.

Another View On Akamai Technologies’ Valuation

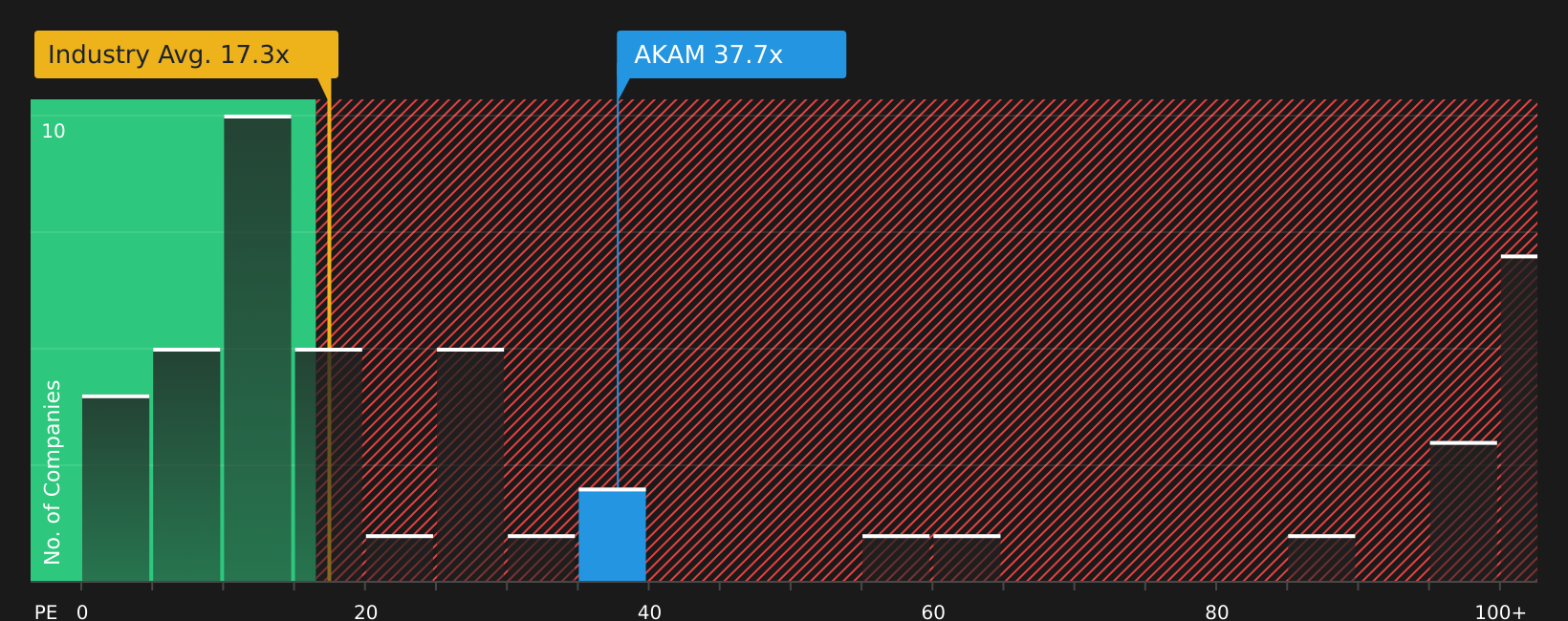

The analyst narrative frames Akamai Technologies as 25.8% undervalued against a fair value anchor of $159.30, but the current P/E of 39.5x tells a tougher story. That is well above the US IT industry average of 16.6x and still higher than a fair ratio of 34.4x, which implies some valuation risk if sentiment cools.

This second lens suggests investors are already paying up for Akamai Technologies compared to both its sector and that fair ratio the market could move toward, even while the narrative highlights upside to $159.30. Which signal matters more for you right now depends on how you weigh relative valuation against that fair value anchor.

Next Steps

If the mixed signals around Akamai Technologies leave you torn between optimism and caution, take a closer look now and decide where you stand based on the company’s specific risks and potential rewards, starting with the 1 key reward and 2 important warning signs.

Looking for more investment ideas beyond Akamai Technologies?

Do not stop with Akamai Technologies. Broaden your watchlist now so you are not looking back later wishing you had checked a few more options.

- Zero in on potential mispricing by reviewing companies that screen as 43 high quality undervalued stocks before attention and liquidity potentially shift elsewhere.

- Strengthen your defense by focusing on businesses that qualify for the 74 resilient stocks with low risk scores, so choppy markets do not dictate every move you make.

- Get ahead of the crowd by scanning the screener containing 19 high quality undiscovered gems that pair solid fundamentals with lower visibility on many investors' radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.