Is Align Technology (ALGN) Fully Priced As EU Antitrust Scrutiny Clouds Its Valuation?

Align Technology, Inc. ALGN | 0.00 |

The European Commission’s new antitrust investigation into Align Technology (ALGN), focused on its iTero scanners and Invisalign ecosystem, has sharpened attention on the stock’s risk profile and how potential regulatory outcomes could affect investor sentiment.

Against the backdrop of the European Commission probe, Align Technology’s recent share price performance has been relatively firm, with a 10.0% 1 month share price return and an 18.3% year to date share price return. This contrasts with a 6.3% decline in 1 year total shareholder return and a 44.0% decline in 3 year total shareholder return, suggesting short term momentum has picked up while longer term holders remain under pressure.

If this regulatory spotlight has you reassessing your watchlist, it can help to see how other dental and medical technology stocks are trading by running the 40 healthcare AI stocks.

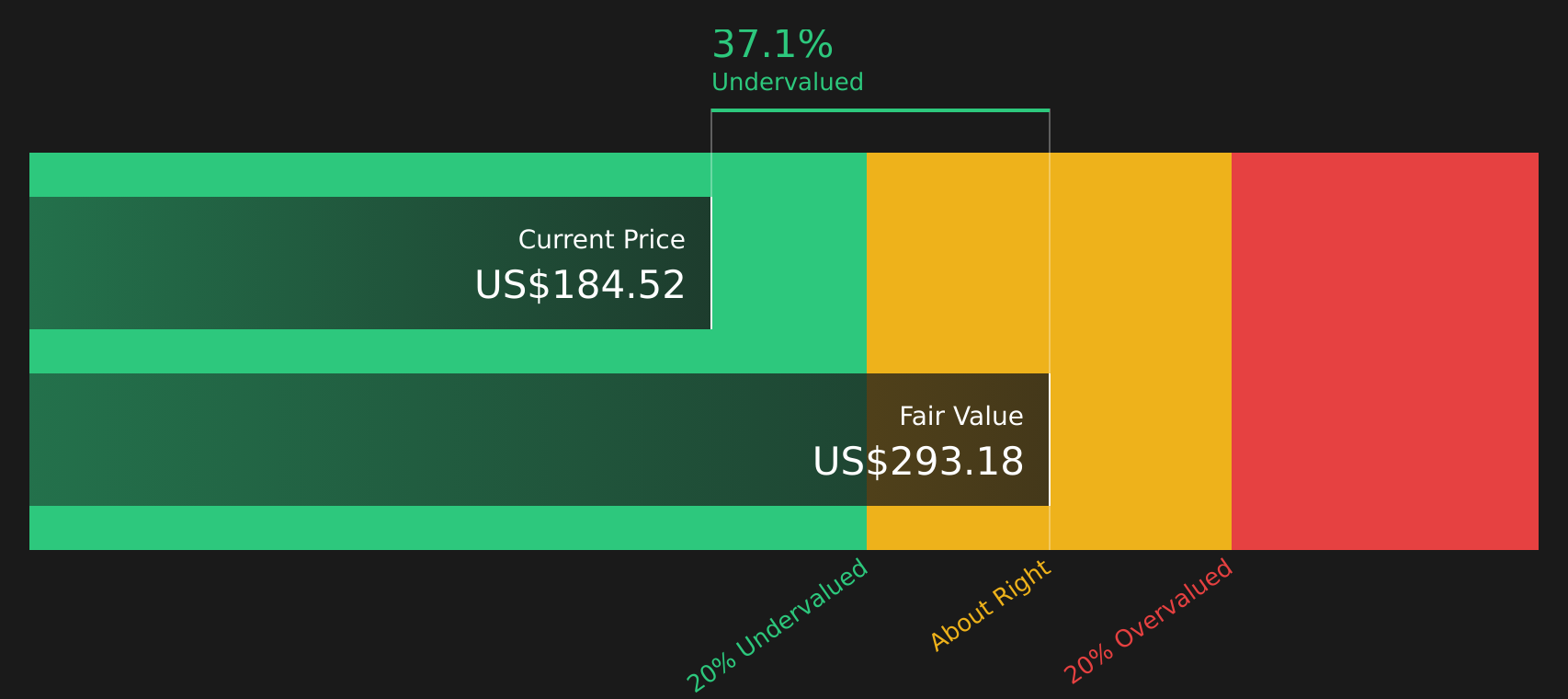

With Align Technology trading at US$184.52 and reference estimates pointing to both an intrinsic discount and a gap to analyst targets, the key question is whether current risks are already reflected in the price, or if markets are still assuming stronger growth ahead.

Most Popular Narrative: 19.3% Overvalued

The most followed narrative on Align Technology currently points to a fair value of $154.62, which sits below the last close of $184.52, and uses a discount rate of 7.696336% to frame future cash flows.

Today, Align operates in a different environment. Inflation, discretionary spending pressure, and rising competition are testing whether premium orthodontics can sustain growth without sacrificing margins.

Want to understand why this narrative still assigns a premium to Align Technology? It leans heavily on margin resilience, disciplined investment, and a future earnings profile that assumes premium orthodontics keep their pricing power. Curious which revenue mix and profitability path underpin that $154.62 figure and tie back to those cash flow assumptions? The full narrative lays out the numbers behind that conviction.

Result: Fair Value of $154.62 (OVERVALUED)

However, this depends on Align Technology maintaining clinical trust and premium positioning while managing the European Commission investigation without meaningful disruption to its iTero and Invisalign ecosystem.

Another View: Align Technology Through a Cash Flow Lens

That 19.3% overvalued narrative sits awkwardly beside our DCF model, which points to a fair value of $293.18, implying Align Technology at $184.52 is trading at a 37.1% discount and screens as undervalued. When two frameworks disagree this sharply, which one do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Align Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split on Align Technology, use that tension as a prompt to move quickly, review the underlying data, and weigh the 2 key rewards.

Looking for more investment ideas beyond Align Technology?

If you are reassessing Align Technology, do not stop there. Broaden your opportunity set with fresh stock ideas tailored to different risk levels and income goals.

- Spot potential rebound stories early by reviewing 20 elite penny stocks with strong financials that already pair tiny market caps with stronger financial profiles.

- Focus on quality at a discount by scanning the 44 high quality undervalued stocks that blend healthier cash flows with sturdier balance sheets.

- Prioritise resilience and capital preservation by filtering for 74 resilient stocks with low risk scores that stand out on stability, not just headline growth potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.