Is Allstate's (ALL) Surge in Earnings and Buybacks Reshaping Its Shareholder Value Proposition?

Allstate Corporation ALL | 0.00 |

- The Allstate Corporation recently reported second quarter 2025 results, highlighting a sharp increase in net income to US$2.11 billion and basic earnings per share of US$7.86, alongside the completion of a share repurchase program totaling over 2.22 million shares for US$445.08 million.

- These developments reflect both a significant improvement in operational performance and the company's ongoing commitment to capital returns for shareholders.

- We'll now examine how Allstate's substantial earnings growth and accelerated buybacks may influence its future investment narrative.

AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Allstate Investment Narrative Recap

To be a shareholder in Allstate today, you have to believe in the strength of its property-casualty insurance model, particularly its ability to grow profitably through digital products, advanced pricing, and a disciplined capital return approach. The recent strong earnings report and completion of a major share buyback program underscore management’s focus on profitability and shareholder returns. However, these announcements don’t materially change the near-term catalyst of scaling digital offerings or alter the biggest risk of margin pressure from intensifying competition and technology shifts.

Among recent announcements, the completion of a US$445.08 million share repurchase stands out. This buyback, combined with robust Q2 earnings, reinforces confidence in Allstate’s current earnings power and capital return capacity, a key support for the narrative that technology investment and product rollout can drive top-line growth while supporting returns. But risks remain, especially as the industry faces evolving competition and pricing strategies.

Yet, even with earnings momentum, investors should never lose sight of growing competition from digital-first insurance providers and direct carriers, since...

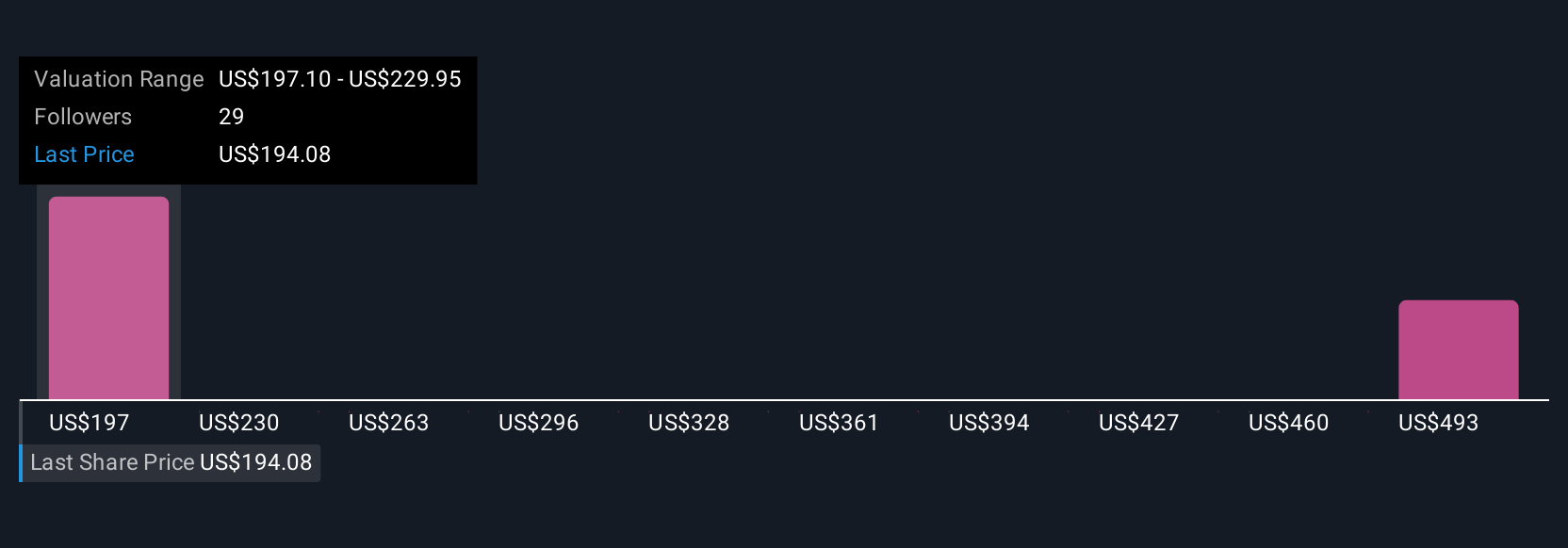

Allstate's outlook forecasts $76.4 billion in revenue and $4.3 billion in earnings by 2028. This is based on an assumed yearly revenue growth rate of 4.9% and a decrease in earnings of $1.4 billion from the current $5.7 billion.

Uncover how Allstate's forecasts yield a $230.59 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Fair value estimates from five Simply Wall St Community members span US$174 to US$552 per share, highlighting strong variation in individual outlooks. With such disparity, it’s clear you should consider how persistent competition and technology innovation might shape Allstate’s profits across different market cycles.

Explore 5 other fair value estimates on Allstate - why the stock might be worth over 2x more than the current price!

Build Your Own Allstate Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Allstate research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Allstate research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Allstate's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.