Is American Airlines a Bargain After a 15.5% Surge Despite 2025 Headwinds?

American Airlines Group Inc. AAL | 10.84 | -2.61% |

- Wondering if American Airlines Group is really a bargain or just looks cheap on the surface? You are not alone, and this could be the perfect time to look under the hood.

- The stock has climbed 15.5% in the past 30 days, yet is still down 21.7% year-to-date, making for an intriguing setup for investors weighing recent momentum against longer-term challenges.

- Headlines recently have highlighted American Airlines' strategic updates around its network and ongoing operational improvements. Both factors have fueled conversations about a possible turnaround. Investors are also weighing broader industry trends, such as shifting travel demand and fuel price movements, as they make sense of these price swings.

- The company scores a 4 out of 6 on our quick valuation checks, suggesting it may be undervalued on several fronts. Next, let us break down the main valuation methods investors use to analyze American Airlines. There is also another way to think about American Airlines’ value at the end of this article.

Approach 1: American Airlines Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future free cash flows and discounting them back to today’s value. Essentially, it asks, “How much are the cash profits American Airlines Group is expected to generate over time worth in today’s dollars?”

American Airlines Group’s last twelve months free cash flow stands at $1.03 Billion. Analyst estimates suggest this could rise to $1.14 Billion by 2028. Since forecasts usually only look out five years, Simply Wall St extrapolates further ahead with projections exceeding $2.2 Billion in 2035.

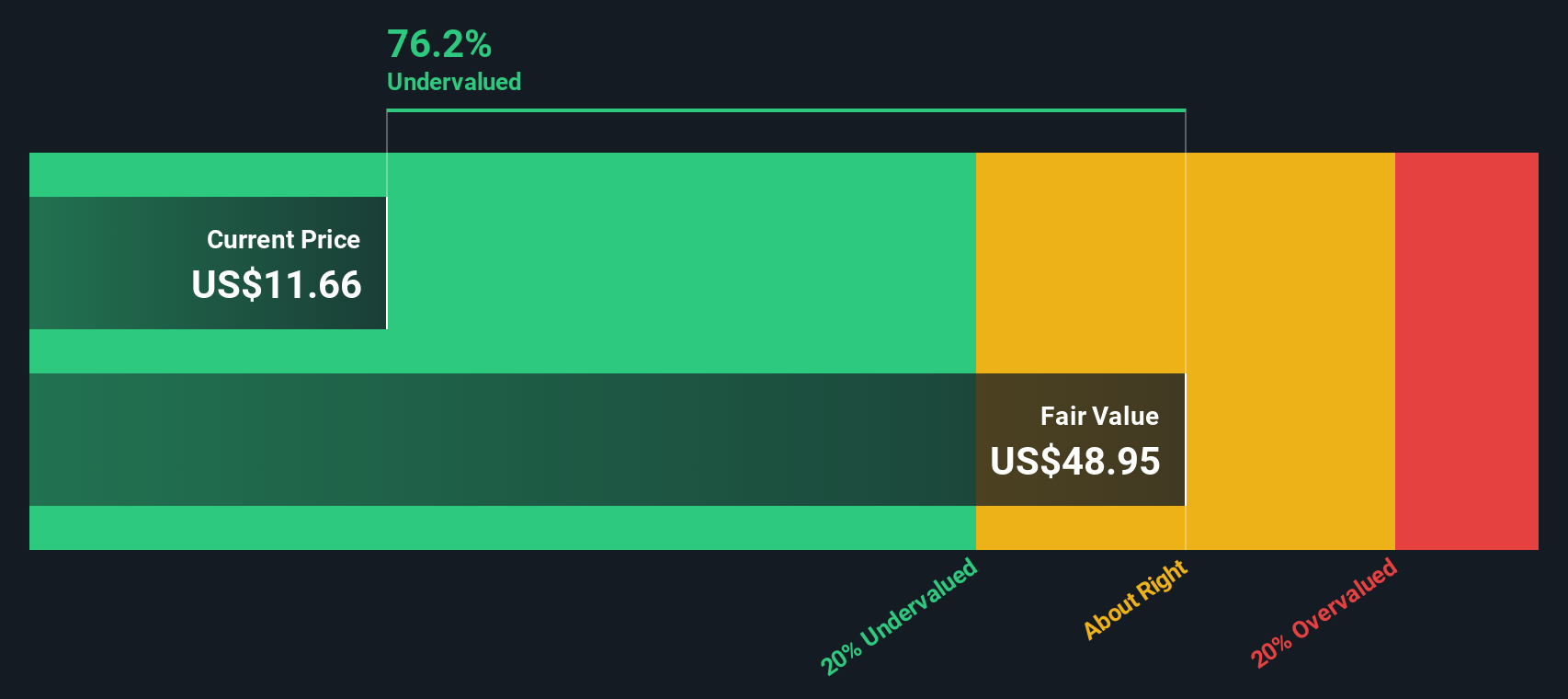

Taking these cash flow estimates and discounting them, the DCF analysis yields an intrinsic value of $23.15 per share for American Airlines Group. With the stock trading at a 42.5% discount to this estimate, the share price appears significantly undervalued according to DCF.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests American Airlines Group is undervalued by 42.5%. Track this in your watchlist or portfolio, or discover 865 more undervalued stocks based on cash flows.

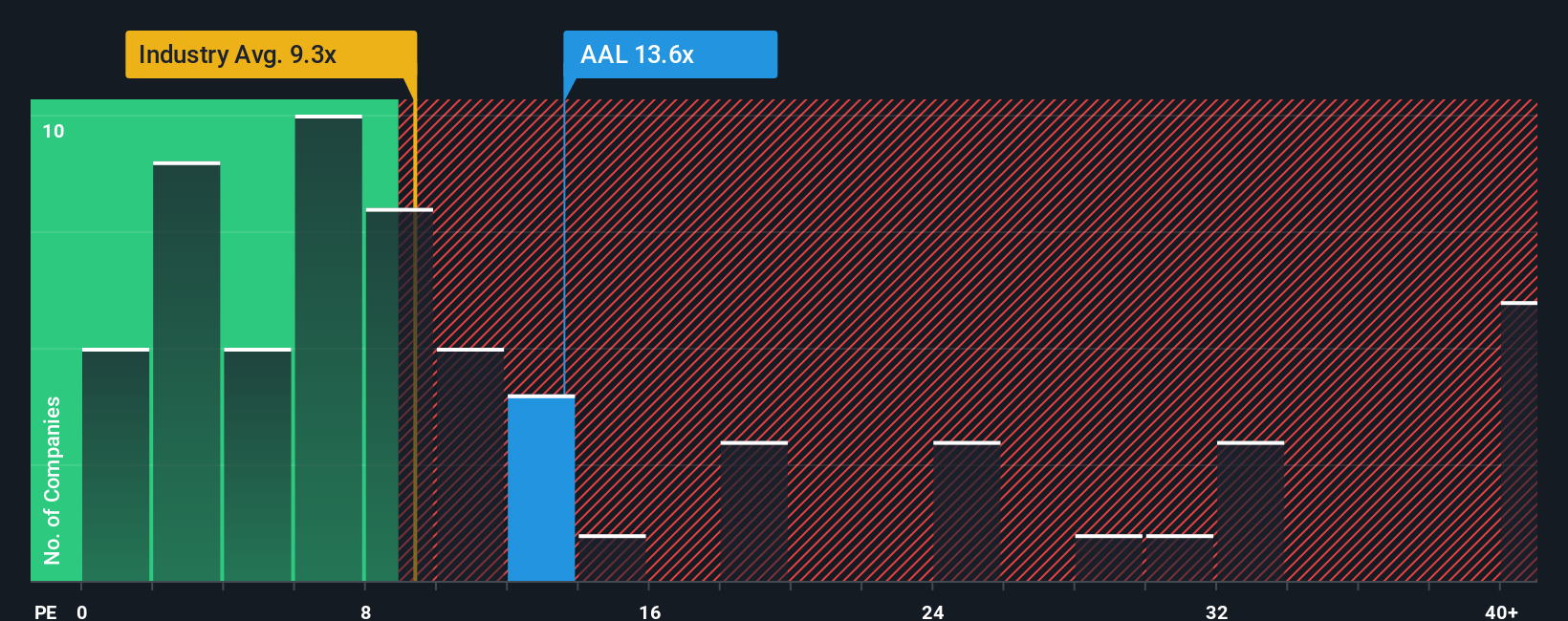

Approach 2: American Airlines Group Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used valuation metrics for companies that are profitable, like American Airlines Group. It compares a company’s share price to its earnings per share and helps investors gauge how much the market is willing to pay today for a dollar of earnings.

When considering a “normal” or “fair” PE ratio, it is important to account for how quickly a company is expected to grow and the risks it faces. Higher growth and lower risk often justify a higher PE ratio, while the opposite can result in a lower fair value.

American Airlines Group currently trades at a PE ratio of 14.6x. This is higher than the industry average PE of 9.0x, which indicates that investors are willing to pay more for its earnings compared to average airline peers. However, its PE is below the broader peer average of 23.6x, which suggests the stock is still priced conservatively relative to its closest competitors.

Simply Wall St’s proprietary “Fair Ratio,” which integrates not just earnings but also factors like growth prospects, profit margins, industry standing, market capitalization and company-specific risks, gives a value of 22.8x. Unlike industry or peer comparisons that may miss unique company traits, the Fair Ratio is tailored to American Airlines’ specific outlook.

Since the company’s current PE of 14.6x is well below its Fair Ratio of 22.8x, shares appear undervalued according to this approach.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1402 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your American Airlines Group Narrative

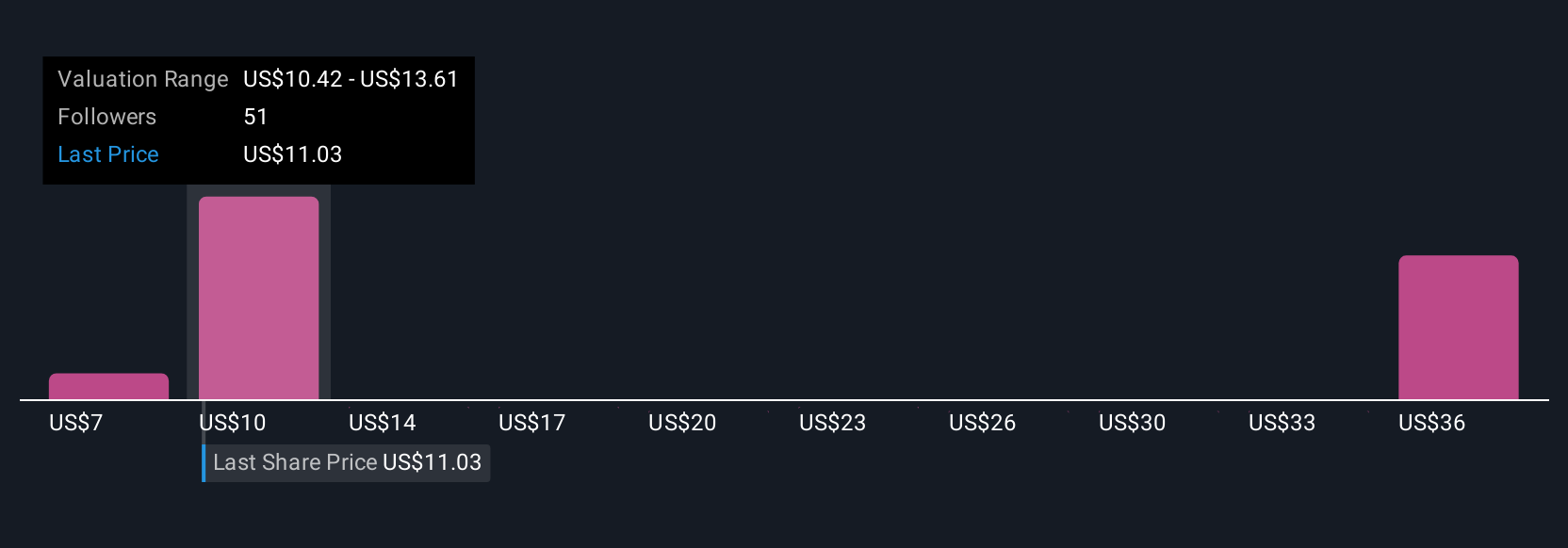

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is your story or perspective on a company, built by linking together how you see its future, such as expected revenues, profit margins, and risks, and translating that into a fair value range. Instead of just looking at the numbers, Narratives let you express the “why” behind those estimates, combining your outlook with financial forecasts in a way that’s easy to follow and share.

On Simply Wall St’s Community page, trusted by millions of investors, Narratives are accessible and simple to create or review, helping you frame your own investment thesis and see how others are thinking. Narratives also recalculate and adapt in real time as new data or company news emerges, so you can make confident, up-to-date decisions.

Most importantly, Narratives empower you to decide when the price is right to buy or sell by always comparing Fair Value (from your assumptions) to the company’s current share price. For example, some see American Airlines Group’s fair value at $10.61 based on debt concerns and margin pressures, while others place it at $15.02 factoring in premium service growth and improving industry trends. Your Narrative can reflect your unique viewpoint.

For American Airlines Group, here are previews of two leading American Airlines Group Narratives:

- 🐂 American Airlines Group Bull Case

Fair Value: $15.02

Current Price is 11.4% below this fair value

Revenue Growth Rate: 4.90%

- Recent domestic demand recovery, premium enhancements, and loyalty program expansion support long-term revenue growth and stable margins.

- Fleet upgrades and strategic international alliances are expected to boost efficiency and capitalize on global travel trends.

- Balance sheet risks remain with high debt and labor costs limiting financial flexibility and exposing the company to operational challenges.

- 🐻 American Airlines Group Bear Case

Fair Value: $10.61

Current Price is 25.4% above this fair value

Revenue Growth Rate: 2.5%

- American Airlines’ negative equity and large debt load make its financial position precarious, especially versus other legacy carriers.

- The company’s profitability and margins are highly sensitive to demand shocks and intense industry competition.

- While operational improvements like Premium Economy could help, American remains vulnerable to adverse economic and refinancing trends.

Do you think there's more to the story for American Airlines Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.