Is American Electric Power Company (AEP) Still Attractive After Strong Multi Year Share Price Gains

American Electric Power Company, Inc. AEP | 0.00 |

- Wondering if American Electric Power Company at about US$136.91 is offering fair value or if you might be paying over the odds? This article breaks down what the current pricing could mean for you.

- The stock last closed at US$136.91, with returns of 1.6% over 7 days, 4.0% over 30 days, 18.2% year to date, 31.4% over 1 year, 66.4% over 3 years, and 86.7% over 5 years. This provides useful context before assessing any valuation metrics.

- Recent trading interest has been shaped by ongoing attention on regulated utilities in the US and how investors view companies that provide essential electricity infrastructure. At the same time, American Electric Power Company continues to feature in broader sector coverage that often focuses on income, regulation, and capital investment needs rather than short term headlines.

- Simply Wall St currently assigns American Electric Power Company a value score of 3 out of 6. This suggests that some valuation checks look supportive while others raise questions. The next sections will walk through those methods before finishing with a more holistic way to think about what the stock is worth.

Approach 1: American Electric Power Company Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what a share could be worth by projecting future dividends and growing them at a steady rate, then discounting those payments back to today.

For American Electric Power Company, the recent annual dividend per share used in the model is about US$4.19. Based on a return on equity of 10.42% and a payout ratio of 69.92%, the implied dividend growth rate is 3.13%, calculated from the earnings retained in the business and the return earned on that capital.

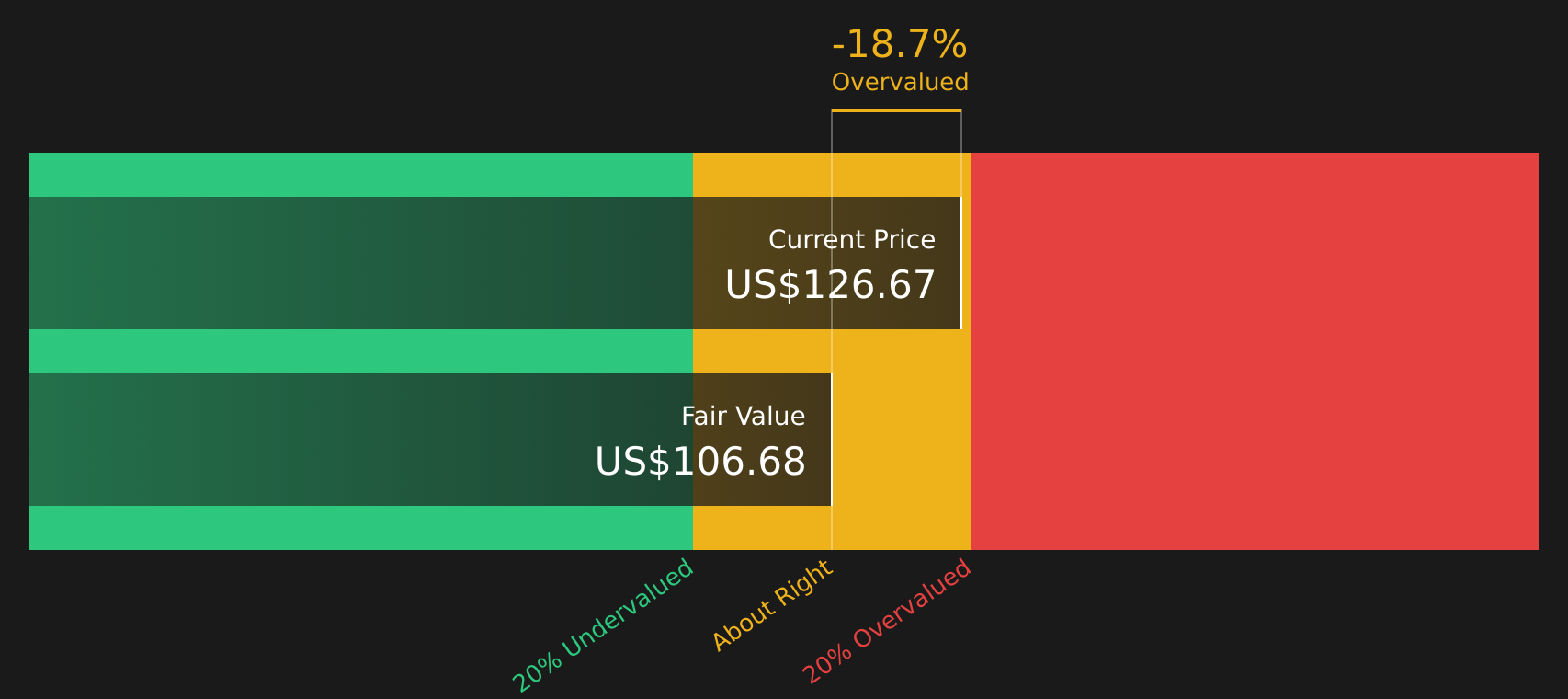

Simply Wall St uses these inputs to project dividends forward and discount them to a present value, which results in an estimated intrinsic value of about US$109.01 per share. Compared with the recent share price of US$136.91, this implies the stock is around 25.6% above the DDM estimate. According to this model, American Electric Power Company appears to be trading on the expensive side based purely on its dividend stream.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests American Electric Power Company may be overvalued by 25.6%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: American Electric Power Company Price vs Earnings

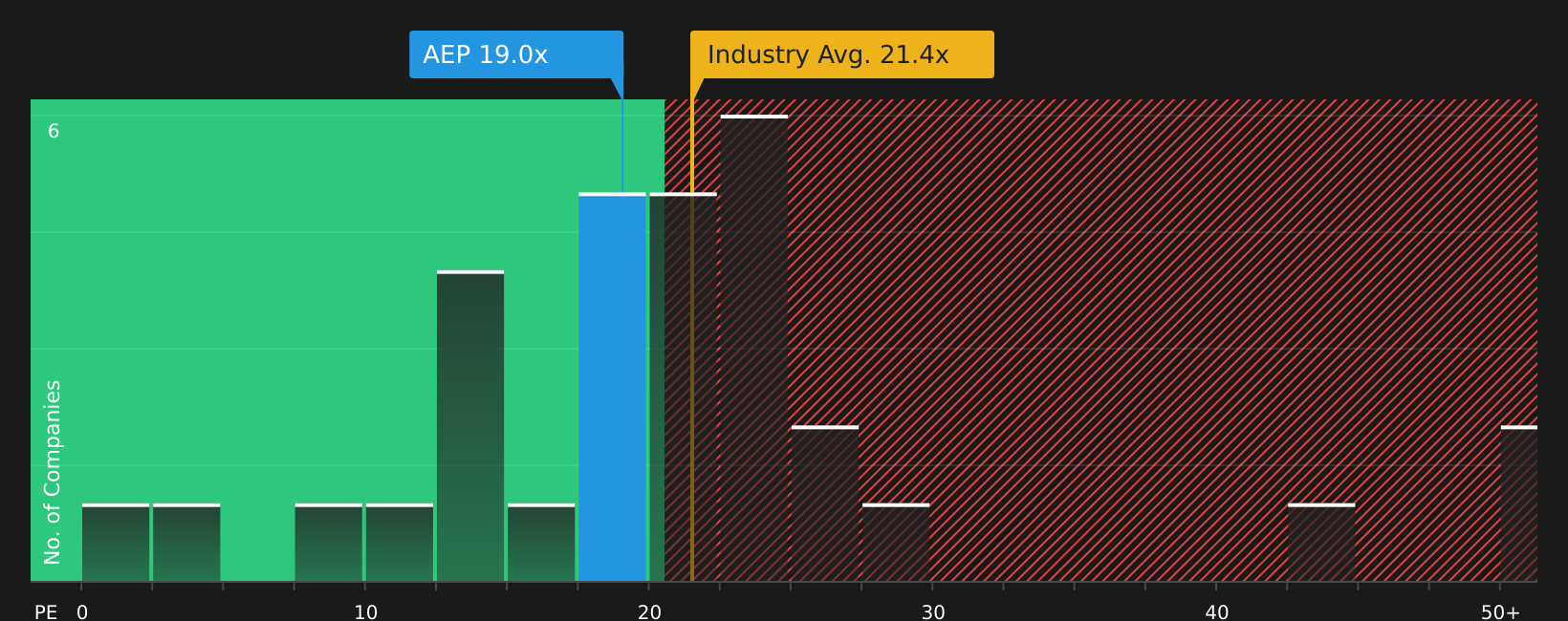

For profitable companies, the P/E ratio is a useful way to think about value because it directly links what you pay for each share to the earnings that company is currently generating.

What counts as a "normal" P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk often goes with a lower one.

American Electric Power Company currently trades on a P/E of 20.7x, compared with the Electric Utilities industry average of about 22.0x and a peer group average of 23.2x. Simply Wall St also calculates a proprietary Fair Ratio of 25.0x, which reflects factors such as earnings growth, industry, profit margin, market cap and company specific risks. This Fair Ratio can be more informative than a simple comparison with peers or the broad industry because it attempts to tailor the "appropriate" multiple to the company’s own profile rather than treating all utilities as the same.

Since the current P/E of 20.7x is below the Fair Ratio of 25.0x, the shares screen as potentially undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your American Electric Power Company Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are worth introducing as a simple way for you to attach a clear story about American Electric Power Company, including your assumptions for future revenue, earnings and margins, to a forecast and a fair value that you can then compare with the current price.

A Narrative on Simply Wall St, available within the Community page that is used by millions of investors, links three pieces together: the business story you believe, the numbers that story implies, and the fair value that drops out of those numbers so you can quickly see whether your view points to a price above or below where the shares trade today.

Because Narratives on the platform are refreshed when new information such as news, earnings or regulatory updates comes through, you can see your fair value and the gap to the live share price update without rebuilding a model from scratch.

For American Electric Power Company, one investor might build a Narrative that focuses on the company as a core grid owner with a fair value close to US$113 based on a more conservative view of load growth and capital deployment, while another might lean closer to the analyst group that collectively sits around US$141 and even up to US$169, reflecting a stronger view on data center demand and the earnings that could support those higher values.

For American Electric Power Company however we will make it really easy for you with previews of two leading American Electric Power Company Narratives:

Fair value: about US$141.38 per share

Gap to this fair value: around 3.3% below the narrative fair value at the recent price of US$136.91

Revenue growth assumption: 7.48% a year

- Focuses on data center driven load growth and a US$54b plus potential US$10b capital plan aimed at transmission and distribution.

- Highlights regulatory work on large load tariffs and energy mix changes, along with funding plans that are intended to support the balance sheet.

- Flags risks around lower margin commercial load, regulation in Ohio, tax changes, large capital needs and supply chain pressures.

Fair value: about US$113.00 per share

Gap to this fair value: around 21.2% above the narrative fair value at the recent price of US$136.91

Revenue growth assumption: 4.51% a year

- Views AEP as having shifted from an income stock to a growth name, with the share price already reflecting a higher P/E and strong grid demand expectations.

- Points to a 56 GW load backlog and a US$72b plus capital plan, with a large tilt toward regulated transmission and distribution.

- Frames US$113 as a conservative value anchor, with the higher current price linked to the role AEP plays in serving AI related power needs.

If you want to see how other investors are joining these pieces together, including different assumptions for growth, margins and required returns, it is worth reading the full Narratives side by side before deciding how American Electric Power Company fits into your own portfolio and risk tolerance. To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for American Electric Power Company on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for American Electric Power Company? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.