Is American Electric Power Company (AEP) Undervalued As 7 GW Deals And CapEx Rise?

American Electric Power Company, Inc. AEP | 0.00 |

Fresh capital plans and data center demand put American Electric Power Company (AEP) in focus

American Electric Power Company (AEP) is back on investor radars after filing a US$274 million shelf registration for 2,000,000 common shares tied to an employee stock ownership plan, alongside 7 GW of new energy project agreements.

After briefly slipping 0.84% over the last trading day, American Electric Power Company’s share price has a 30 day share price return of 8.01% and an 18.13% year to date share price return. Its 1 year total shareholder return of 35.21% and 5 year total shareholder return of 92.27% point to momentum that has aligned with renewed interest around fresh capital plans, data center driven load growth and recent positive brokerage commentary.

If the data center theme has you looking beyond AEP, this is a good moment to scan for other grid focused opportunities using our power grid technology and infrastructure stocks screener via the 35 power grid technology and infrastructure stocks.

With American Electric Power Company trading at US$136.81 against an average analyst price target of US$144.76 and an intrinsic estimate that sits higher than today’s quote, is there still a buying opportunity here, or is the market already pricing in the future growth story?

Most Popular Narrative: 21.1% Overvalued

According to a widely followed narrative for American Electric Power Company, the fair value sits at $113, which is below the last close of $136.81 and frames the current price as rich against that reference point.

The most compelling driver is the unprecedented surge in data center load commitments. AEP’s incremental load pipeline has skyrocketed to 56 GW, a staggering 100% increase from just six months ago. This visibility into the next decade of demand allows AEP to expand its $72B+ capital plan, shifting from a focus on “projected growth” to an emphasis on “rate-base expansion.”

Want to see how a decade long project pipeline, higher regulated earnings mix and a premium future P/E all come together in one valuation story? The narrative sketches a detailed bridge between expected revenue growth, margin assumptions and what investors are currently paying for every dollar of future profit.

Result: Fair Value of $113 (OVERVALUED)

However, American Electric Power Company’s narrative could be challenged if data center load materialises more slowly than expected, or if regulators constrain allowed returns on new grid investments.

Another view on American Electric Power Company’s valuation

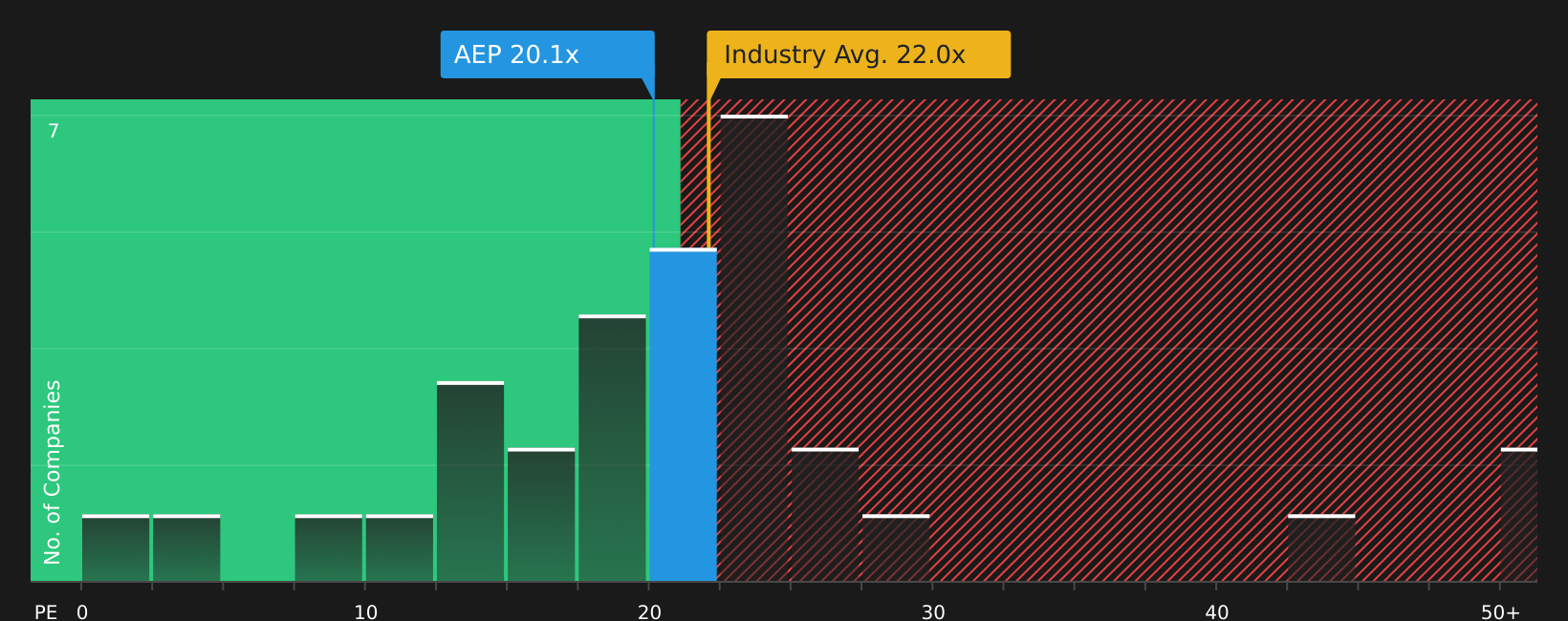

The user narrative leans on a fair value of $113, but the market is also looking at how American Electric Power Company stacks up against peers on earnings. On a P/E of 20.4x versus 22.4x for the Electric Utilities industry and 24.3x for peers, plus a fair ratio of 24.2x, the current price appears to carry less obvious multiple risk than the $113 narrative suggests. This raises the question of which signal matters more to you right now.

Next Steps

With sentiment on American Electric Power Company split between opportunity and caution, this is a good time to examine the data yourself and move quickly to form your own view by weighing the 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond American Electric Power Company?

If you are serious about sharpening your next move after American Electric Power Company, do not stop here. Fresh opportunities are already lining up in the screener.

- Spot potential mispriced opportunities early by reviewing companies highlighted in the screener containing 19 high quality undiscovered gems before they appear on everyone else's radar.

- Strengthen your defensive side by scanning stocks in the 74 resilient stocks with low risk scores that combine resilience with controlled downside risk scores.

- Target quality and value together by filtering companies featured in the solid balance sheet and fundamentals stocks screener (48 results) that pair financial strength with fundamental support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.