Is ArcBest’s (ARCB) Award-Winning Security Masking Deeper Strains in Its Profitability Story?

ArcBest Corporation ARCB | 0.00 |

- In recent years, ArcBest has faced softer customer demand, with purchases postponed and revenue declining by 4.8% annually over the past two years, while earnings per share fell even faster.

- At the same time, ABF Freight’s twelfth American Trucking Associations’ Excellence in Security Award signals operational strengths that contrast with ArcBest’s weakening returns on capital.

- We’ll now examine how ArcBest’s declining profitability and returns on capital may reshape the company’s broader investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

ArcBest Investment Narrative Recap

To own ArcBest, you need to believe its investments in technology, safety, and Managed Solutions can offset softer freight demand, thinner margins, and weaker returns on capital. The recent dip in revenue and faster EPS decline underline near term pressure on profitability, while the main risk remains prolonged freight softness that keeps pricing power limited. These developments may also test the near term catalyst of margin improvement from AI driven efficiency and mix shift toward higher value services.

Against this backdrop, ABF Freight’s 2025 ATA Excellence in Security Award highlights an operational edge that could support customer retention and pricing conversations, even as profitability lags. The focus on security and network hardening, including solar powered lighting and breach detection, aligns with ArcBest’s push to differentiate its LTL network as it seeks to convert new accounts and defend yields in a competitive, capacity heavy market.

Yet in contrast, investors should be aware that prolonged weak returns on capital and soft freight conditions could...

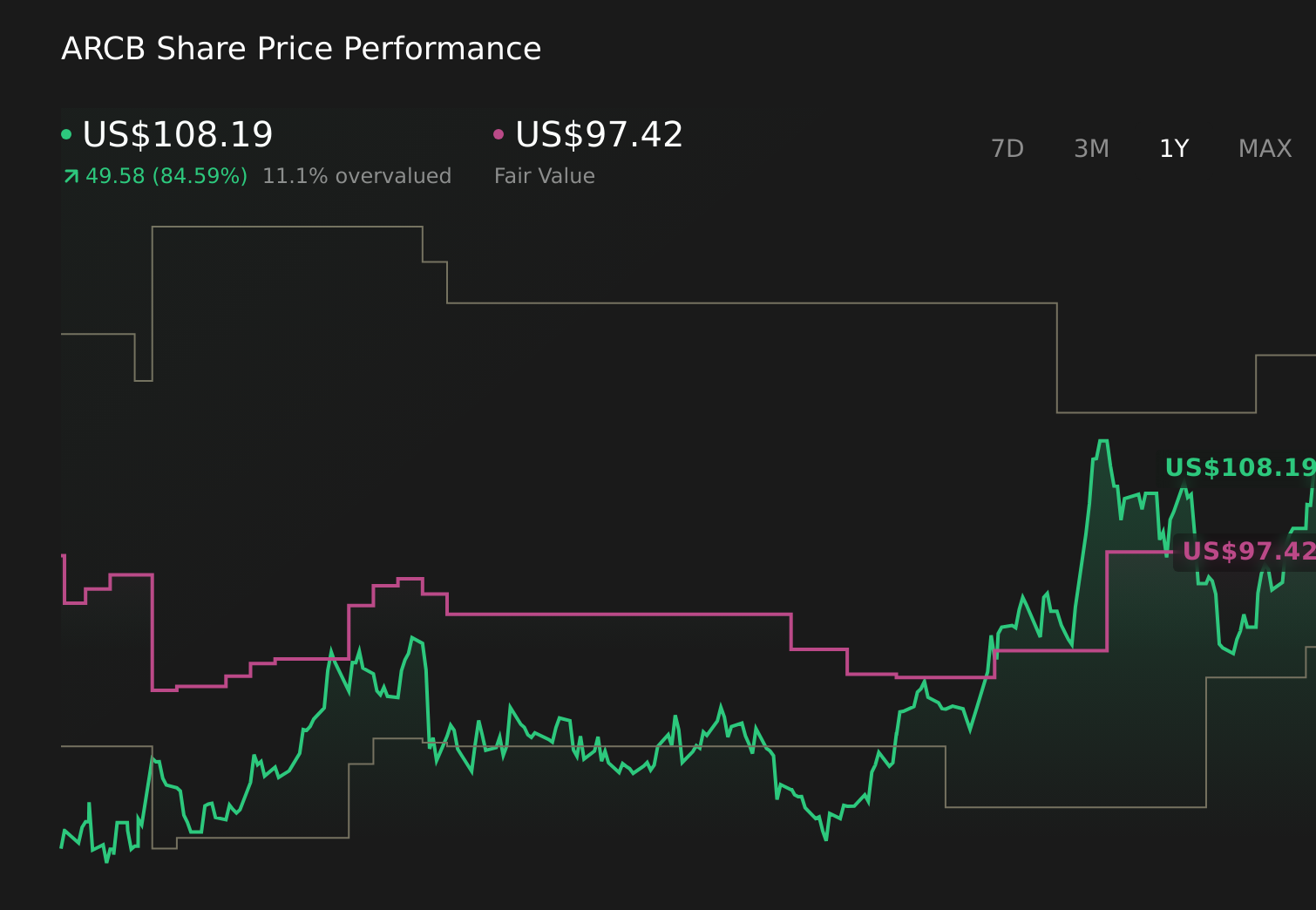

ArcBest's narrative projects $4.5 billion revenue and $147.2 million earnings by 2028. This requires 3.9% yearly revenue growth and an earnings decrease of $11.1 million from $158.3 million today.

Uncover how ArcBest's forecasts yield a $97.42 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a far more cautious view than consensus, even before this news, assuming revenue of about US$4.6 billion and earnings of roughly US$178 million by 2029, which may prove too optimistic or too low once weaker returns on capital and automation risks are fully reflected.

Explore 3 other fair value estimates on ArcBest - why the stock might be worth 32% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ArcBest research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ArcBest research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ArcBest's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 58 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.