Is ASML Still a Smart Pick After Its 44% Surge and Semiconductor Demand News?

ASML Holding NV ADR ASML | 1359.76 1306.00 | +2.95% -3.95% Pre |

- Wondering if ASML Holding is still a buy after its impressive run, or if it is priced for perfection? Here is a breakdown of what’s behind its market value.

- This year alone, ASML shares have soared 43.8%, delivering gains of 52.6% over the past 12 months, even after slight dips of -3.1% over the last week and -2.2% this month.

- Much of this recent price movement has been driven by growing optimism around demand for advanced semiconductor equipment, especially after news highlighting increased investments across the chip industry and global efforts to secure supply chains.

- Our current check gives ASML Holding a 2 out of 6 on our value score. Before drawing any hasty conclusions, let’s explore the different ways to value the stock, along with an approach that might surprise you by the end of the article.

ASML Holding scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

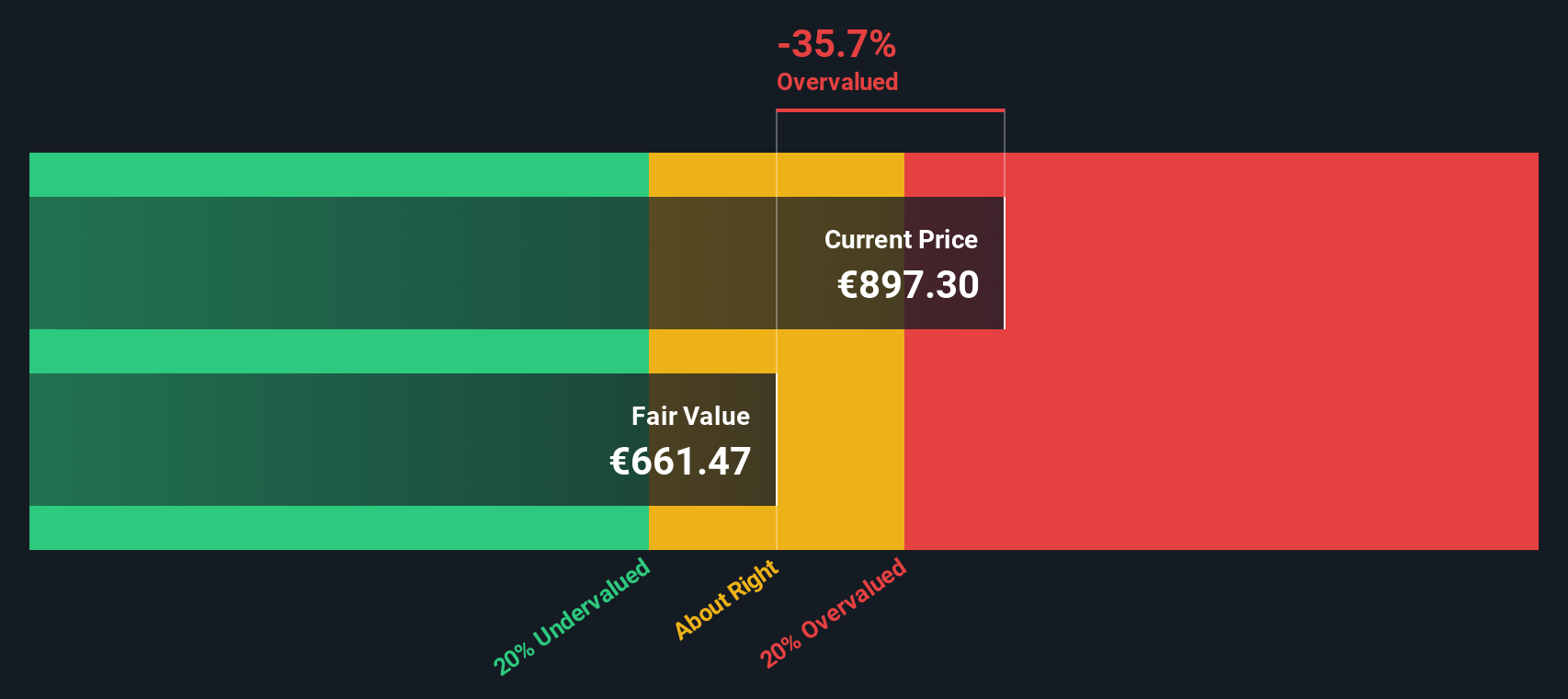

Approach 1: ASML Holding Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a commonly used valuation approach that estimates a company's intrinsic value by projecting its future cash flows and discounting them back to their present value. For ASML Holding, this involves forecasting how much cash the business will generate each year and then calculating what that stream of money is worth in today's terms.

ASML reported trailing twelve-month Free Cash Flow (FCF) of approximately €8.56 billion. Analyst forecasts suggest FCF could reach €17.1 billion by 2029. While professional estimates typically only extend a few years, Simply Wall St extrapolates these further based on growth trends. This method helps gauge how ASML’s cash-generating power may develop over the next decade, using a two-stage model that reflects different growth periods.

The DCF model currently estimates ASML’s intrinsic value at €740.74 per share. When compared to the current market price, the stock appears to be trading at a 35.9% premium relative to its calculated fair value. According to the DCF approach, this indicates that ASML is overvalued at present.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ASML Holding may be overvalued by 35.9%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

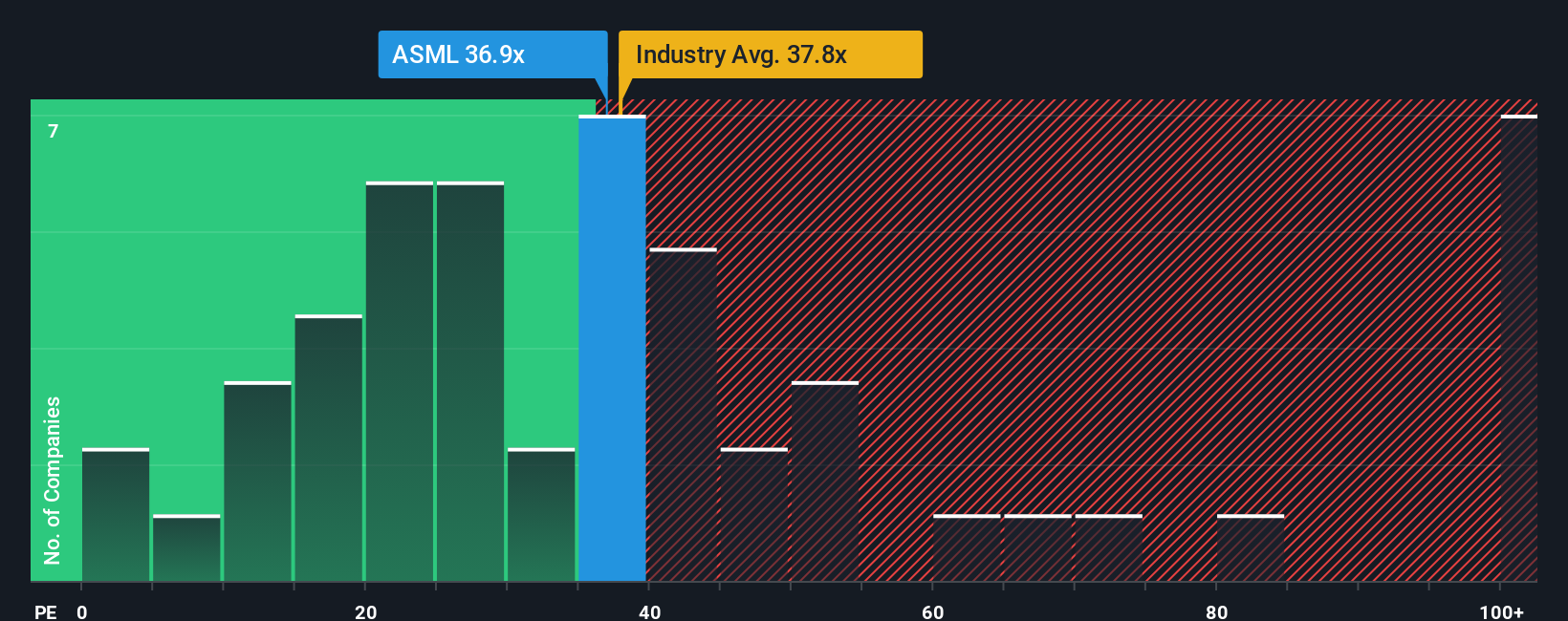

Approach 2: ASML Holding Price vs Earnings

The Price-to-Earnings (PE) ratio is a favored valuation measure for profitable companies because it directly connects a company’s market value to its earnings generation. Investors often use it to gauge whether they are paying a reasonable price for each dollar of profit a company makes.

It is important to note that what counts as a “fair” PE ratio varies by sector and company type. Higher growth rates, lower risk profiles, or dominant market positions can all justify PE ratios above the industry average. Conversely, slower growth or heightened risks should generally command a discount.

ASML Holding currently trades at a PE ratio of 35.77x. For context, this compares to a semiconductor industry average of 34.75x and a peer group average of 38.26x. These benchmarks are useful but can sometimes overlook company-specific factors that drive value.

This is where Simply Wall St's proprietary “Fair Ratio” comes in. The Fair Ratio for ASML is 37.86x. This figure is calculated based on the company’s unique earnings growth prospects, robust profit margins, size, risk exposure, and industry outlook. Unlike broad industry or peer comparisons, this metric provides a more tailored and dynamic assessment of fair value.

Since ASML’s actual PE ratio is very close to its Fair Ratio, the stock appears to be valued about right according to this approach.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1413 companies where insiders are betting big on explosive growth.

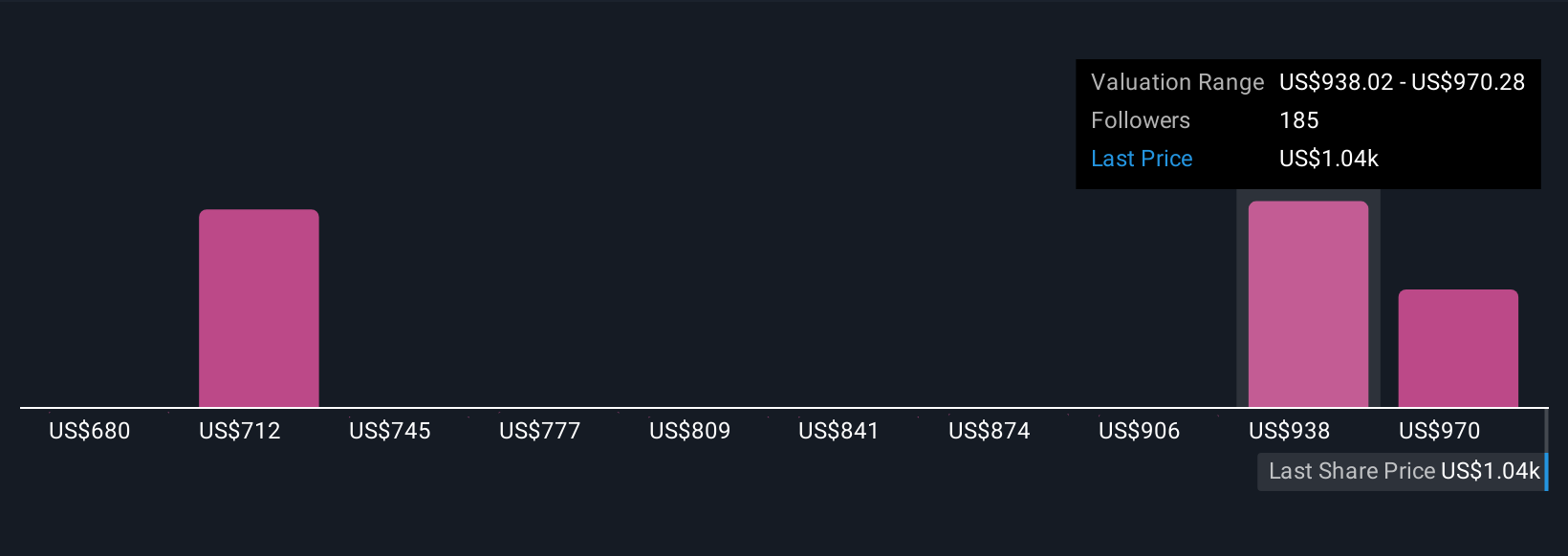

Upgrade Your Decision Making: Choose your ASML Holding Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is more than just numbers; it is your perspective on a company’s future, connecting your assumptions about fair value, future revenue, earnings, and profit margins into a coherent story.

Narratives link a company's story to financial forecasts and, ultimately, to a calculated fair value. They are easy to use and available to everyone on Simply Wall St's Community page, where millions of investors share and adjust their perspectives in real time.

This tool can help you decide when to buy or sell by making it easy to compare your Narrative's Fair Value with the current Price. Plus, since Narratives update automatically when big news or earnings releases come out, your view stays current and relevant.

For example, some investors see ASML Holding’s fair value over €1,000 based on strong market demand and technological leadership. Others set fair value around €740, reflecting concerns about industry risks or slower near-term growth.

Do you think there's more to the story for ASML Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.