Is Berkshire Hathaway (BRK.B) Still A Bargain Under Greg Abel?

Berkshire Hathaway Inc. Class B BRK.B | 0.00 |

Berkshire Hathaway stock has returned 80.4% over the past five years, yet current valuation checks suggest the market price may still sit below an estimate of intrinsic value based on the Excess Returns model and earnings multiples.

- The 80.4% five year return points to solid wealth creation for long term shareholders, but it also raises the bar for any further mispricing to remain.

- Greg Abel’s recent capital moves, including the agreed Taylor Morrison acquisition and resumed share buybacks, can support the intrinsic value case. However, execution risk around large housing and AI related investments may limit how much of that value the market is willing to pay for.

- Berkshire Hathaway screens as undervalued on most checks, with the broader toolkit indicating the stock looks cheap against fundamentals in 5 of 6 valuation tests.

The issue now is whether Berkshire Hathaway’s current price already reflects this intrinsic value case or if the recent moves under Abel leave further room for upside before the valuation gap closes.

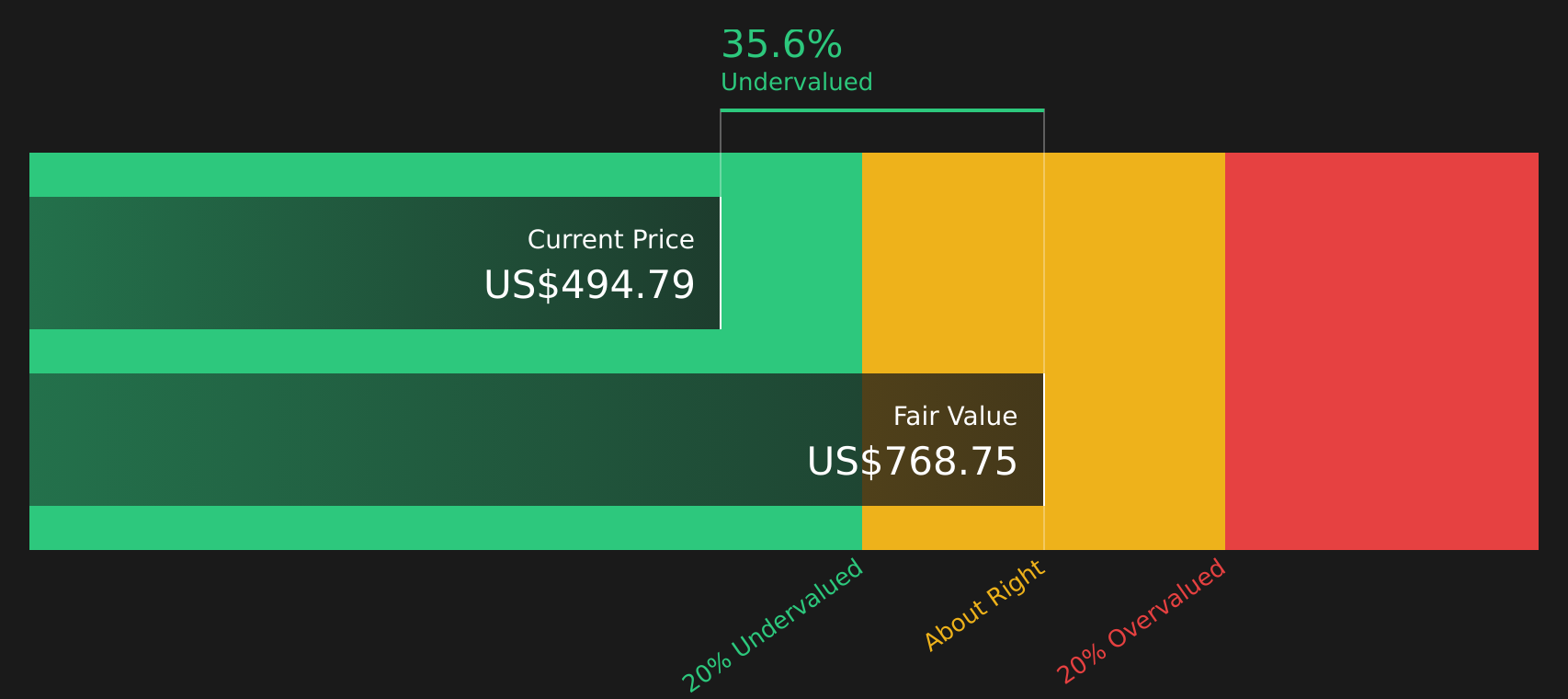

Is Berkshire Hathaway a Bargain on Excess Returns?

The Excess Returns model for Berkshire Hathaway looks at how much profit the company can generate on its equity above its estimated cost of capital, then capitalizes that surplus. Berkshire’s book value is set at $505,559.42 per share and its stable earnings per share at $63,684.58, based on the median return on equity from the past 5 years.

Against a cost of equity of $40,103.60 per share, this points to an excess return of $23,580.97 per share and an average return on equity of 11.75%. The model assumes stable book value moves toward $542,107.44 per share, using estimates from two analysts, and arrives at an intrinsic value of about $770.70 per share. With that estimated intrinsic value about 35.1% above the current share price, Berkshire Hathaway screens as undervalued on this method.

Because Greg Abel’s recent Taylor Morrison deal and large AI related investments rely heavily on Berkshire’s equity base, the Excess Returns framework helps explain why the stock still screens undervalued even as capital is being put to work more aggressively.

On this Excess Returns view, Berkshire Hathaway stock currently looks undervalued relative to its estimated intrinsic value.

Our Excess Returns analysis suggests Berkshire Hathaway is undervalued by 35.1%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Does Berkshire Hathaway Look Undervalued on Earnings?

The P/E ratio fits Berkshire Hathaway because earnings are a central yardstick for a mature, diversified conglomerate with many operating businesses. Right now, Berkshire Hathaway trades on a P/E of 14.9x, compared with a Diversified Financial industry average of about 15.3x and a broader peer average of 23.9x, so the stock sits below both reference points.

The fair P/E ratio for Berkshire Hathaway, based on its profile and risk mix, is estimated at 18.1x. That is comfortably above the current 14.9x, indicating the stock would need a higher multiple to align with this tailored benchmark. Even after Greg Abel’s recent capital deployment into Taylor Morrison and AI related holdings, the market is pricing Berkshire Hathaway at a discount to what this framework suggests.

On the P/E multiple, Berkshire Hathaway stock appears undervalued relative to both its tailored fair ratio and key benchmarks.

The Berkshire Hathaway Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Berkshire Hathaway valuation puzzle leaves off by spelling out which paths for growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price, and they sit on the company’s Community page. Rather than centering everything on a single multiple or model, each narrative lays out the assumptions behind its fair value so you can compare them with Berkshire Hathaway’s actual results over time.

Be one of the first voices in the Simply Wall St community to set out a number driven Narrative on Berkshire Hathaway, weighing in on how moves like the Taylor Morrison acquisition and the larger AI related allocations might shape the story from here. Share your view, define your assumptions, and then track how they compare with Berkshire Hathaway's actual results over time.

Do you think there's more to the story for Berkshire Hathaway? Head over to our Community to see what others are saying!

The Bottom Line

Berkshire Hathaway looks undervalued on both the Excess Returns intrinsic value estimate and current earnings multiples, which broadly point in the same direction. The market is pricing the stock below what these frameworks suggest, but that gap likely hinges on how confidently investors view Greg Abel’s capital deployment, especially around housing and AI related investments. For now, the key question is whether the discount reflects lingering execution and allocation risk or an opportunity if Berkshire’s returns on its large equity base hold up under the new playbook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.