Is Block (SQ) Offering An Opportunity After Recent Share Price Pullback?

Block XYZ | 0.00 |

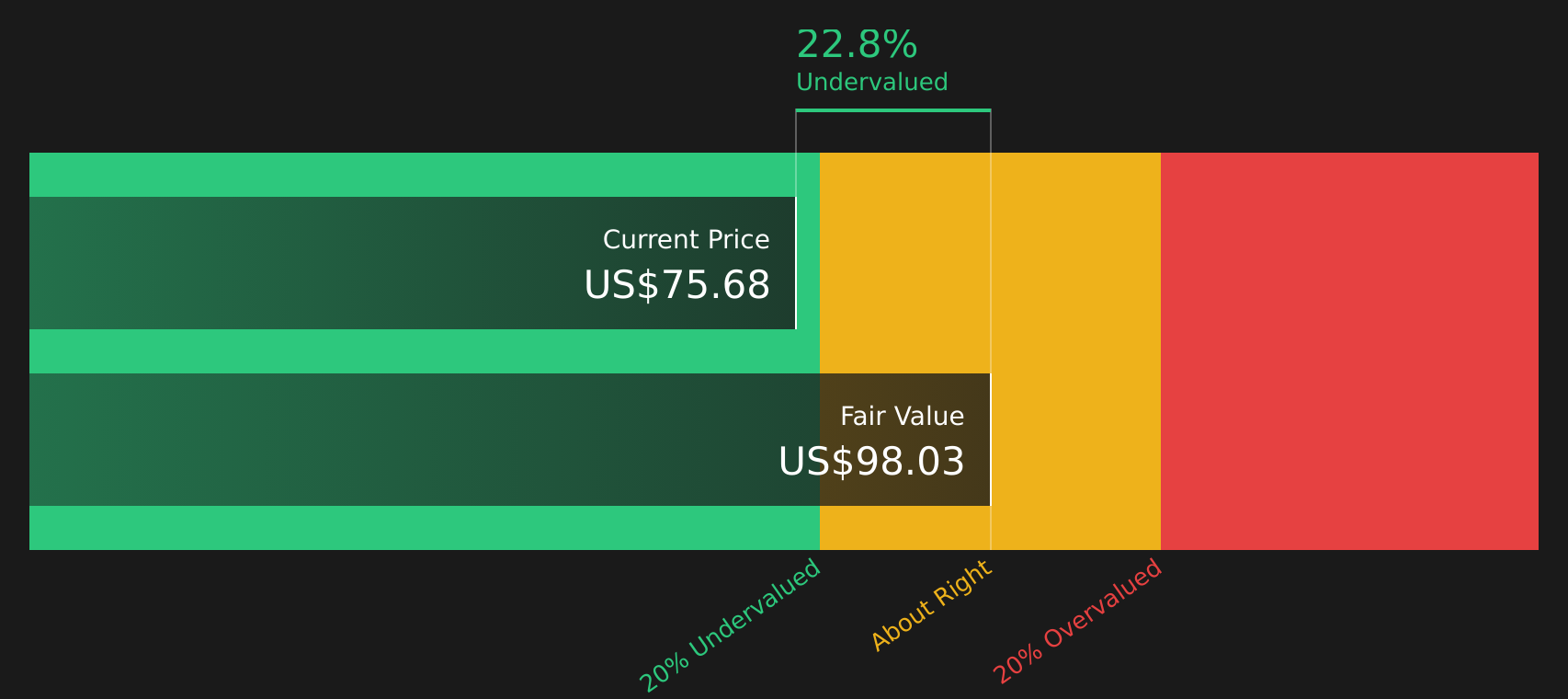

- Wondering whether Block at around US$68.08 is offering fair value right now, or if the stock is pricing in more than it should.

- The share price is up 4.5% year to date and 9.5% over the last year, but has fallen 5.0% over the past month and 1.6% over the past week, which can shift how the market is thinking about both upside and risk.

- Recent coverage has focused on Block's role as a diversified financial stock and how its long term share price record, including a 15.7% return over three years and a 69.3% decline over five years, frames expectations today. This context is useful when weighing whether the current price is reflecting business fundamentals or just changing sentiment.

- On Simply Wall St's 6 point valuation checklist, Block scores 3 out of 6, so the next sections will break down what that means across different valuation methods and then finish with a way to look at value that goes beyond the usual metrics.

Approach 1: Block Excess Returns Analysis

The Excess Returns model looks at how much profit a company can generate above the return that shareholders are assumed to require, and then values the stock based on those surplus profits over time.

For Block, the model starts with a Book Value of $36.48 per share and a Stable EPS of $5.45 per share, based on weighted future Return on Equity estimates from 9 analysts. The Cost of Equity is $3.41 per share, which implies an Excess Return of $2.03 per share. In other words, the model assumes Block earns more on its equity than shareholders require, with an Average Return on Equity of 12.03%.

The Stable Book Value is set at $45.27 per share, using weighted future Book Value estimates from 7 analysts. Feeding these inputs into the Excess Returns framework produces an estimated intrinsic value of $96.08 per share in $.

Against a recent share price of about $68.08, this implies Block is 29.1% undervalued according to this model.

Result: UNDERVALUED

Our Excess Returns analysis suggests Block is undervalued by 29.1%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: Block Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of earnings. This is often more intuitive than cash flow or book value for many investors.

A "normal" or "fair" P/E typically reflects what the market expects for future earnings growth and how risky those earnings are perceived to be. Higher expected growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk usually points to a lower multiple.

Block currently trades on a P/E of 50.21x, compared with the Diversified Financial industry average of 17.90x and a peer average of 11.27x. This suggests the stock trades at a higher multiple than many sector peers.

Simply Wall St's proprietary Fair Ratio for Block is 27.70x. This metric aims to estimate what P/E might be appropriate once factors like earnings growth, profit margins, company size, industry characteristics and key risks are considered, instead of relying only on simple peer or industry comparisons.

On this basis, Block's current P/E of 50.21x sits above the Fair Ratio of 27.70x. This indicates the stock screens as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Block Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story to the numbers by spelling out how you think Block's revenue, earnings and margins play out. This turns that story into a financial forecast, a fair value, and a simple comparison with the current share price that updates automatically as new news or earnings arrive. This is why one investor in the Community page might build a bullish Block Narrative around a Fair Value near US$112.45, while another might build a more cautious one closer to US$60.88 or US$85.16, and then use those different fair values to judge whether the current price looks attractive or expensive for their own plan.

For Block, here are previews of two leading Block narratives:

Fair value in this narrative: US$85.52 per share

Implied pricing vs this fair value: Block trades about 20.4% below this narrative fair value based on the recent US$68.08 share price

Revenue growth assumption: 10.77% a year

- Sees AI driven efficiency plans, workforce reductions and product focus as a way to support stronger profitability over time, even if the sector applies a lower future P/E multiple.

- Assumes long term revenue growth of around 10.8% a year and net profit margins of about 10.2%, with a future P/E of 17.6x applied to those earnings.

- Anchors fair value around US$85.52, with analysts citing Q4 profitability focus, Cash App engagement and international expansion as key supports for that outlook.

Fair value in this narrative: US$60.88 per share

Implied pricing vs this fair value: Block trades about 11.8% above this narrative fair value based on the recent US$68.08 share price

Revenue growth assumption: 8.24% a year

- Frames higher regulatory costs, cyber security spending, crypto exposure and fee pressure as constraints on how much value investors might be willing to ascribe to future earnings.

- Builds in revenue growth of about 8.2% a year and profit margins of roughly 8.4%, with a future P/E of 16.3x and a discount rate of 7.6%.

- Arrives at a fair value of US$60.88, with the bearish analyst cohort seeing current pricing as ahead of what those assumptions support.

Taken together, these two narratives outline a band of outcomes you can use to stress test your own expectations for Block's growth, margins and valuation multiples before assessing how the current share price aligns with your risk and return goals.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Block on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Block? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.