Is Boeing (BA) Using Riyadh Air’s 787 Order to Reframe Its Widebody Investment Narrative?

Boeing Company BA | 0.00 |

- Boeing and Riyadh Air recently announced that the new Saudi carrier’s first two 787 Dreamliners have been delivered to Riyadh, marking an early step toward a planned fleet of up to 72 aircraft serving more than 100 destinations by 2030.

- This delivery milestone underlines how Boeing’s widebody program is tied into Saudi Arabia’s broader aviation push to attract 150 million visitors and serve 330 million passengers annually by the end of the decade.

- Next, we’ll examine how the Riyadh Air 787 deliveries and expanding Middle Eastern widebody demand affect Boeing’s broader investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Boeing Investment Narrative Recap

To own Boeing today, you generally have to believe the company can turn a large commercial backlog and planned 737/787 rate increases into sustained cash generation while managing high debt and ongoing certification and quality issues. The Riyadh Air 787 deliveries support the widebody demand narrative, but they do not materially change the near term focus on stabilizing 737 production and addressing program delays and safety concerns, which remain the key catalyst and primary risk.

Among recent updates, Boeing’s plan to open a fourth 737 MAX final assembly line and lift output toward 47 jets per month speaks most directly to this. If execution and regulatory oversight align, higher narrowbody volumes could be a major driver of improved profitability, but they also increase exposure to supply chain strain and quality lapses, so investors may see this alongside Riyadh Air’s 787s as a test of operational discipline.

Yet behind the optimism on orders, investors should be aware that Boeing’s high debt load and ongoing certification challenges could still...

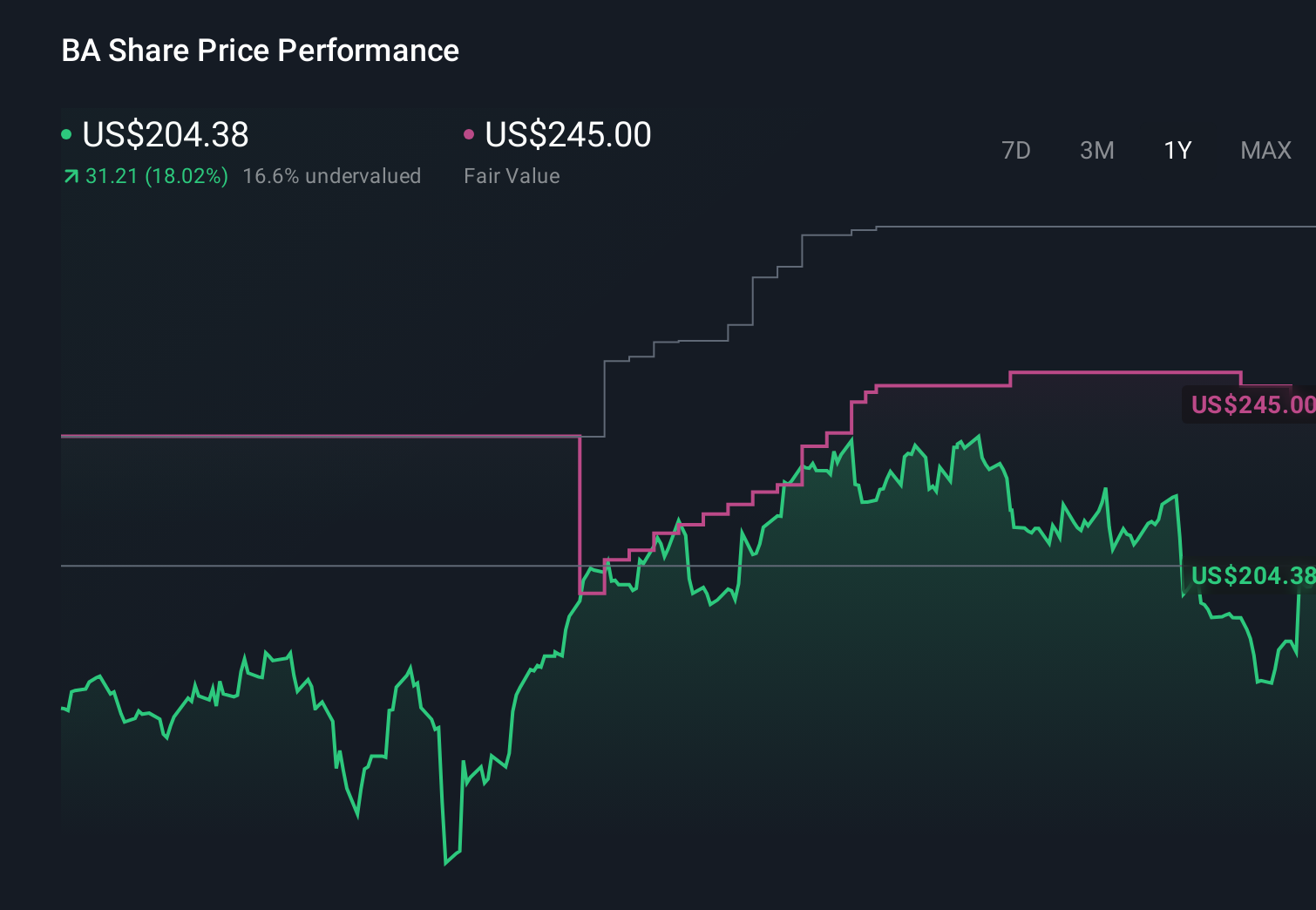

Boeing's narrative projects $125.3 billion revenue and $7.9 billion earnings by 2029. This requires 10.8% yearly revenue growth and a $6.0 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $269.52 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming only about 8.7 percent annual revenue growth to roughly US$118.4 billion and a PE near 49 times, which is far more cautious than the consensus and could shift further as events like the Riyadh Air deliveries and production ramp up plans test whether Boeing can truly overcome its quality control and certification issues.

Explore 7 other fair value estimates on Boeing - why the stock might be worth as much as 69% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.