Is Booz Allen (BAH) Quietly Recasting Its Identity From Consultant To Cybersecurity Platform With Vellox Reverser?

Booz Allen Hamilton Holding Corporation Class A BAH | 83.13 | +3.43% |

- Booz Allen Hamilton Holding recently launched Vellox Reverser, an AI-driven malware reverse engineering and threat intelligence product now broadly available to federal and commercial customers, while also expanding its role in Halcyon’s new Incident Response Partner Program alongside Beazley Security.

- The combination of automated malware analysis, historical campaign linkage, and integrated incident response positions Booz Allen more firmly as a full-spectrum cybersecurity solutions provider rather than only a traditional consultant.

- We will now examine how Vellox Reverser’s AI-powered threat analysis capability shapes Booz Allen Hamilton’s broader investment narrative for investors.

The latest GPUs need a type of rare earth metal called Terbium and there are only 33 companies in the world exploring or producing it. Find the list for free.

What Is Booz Allen Hamilton Holding's Investment Narrative?

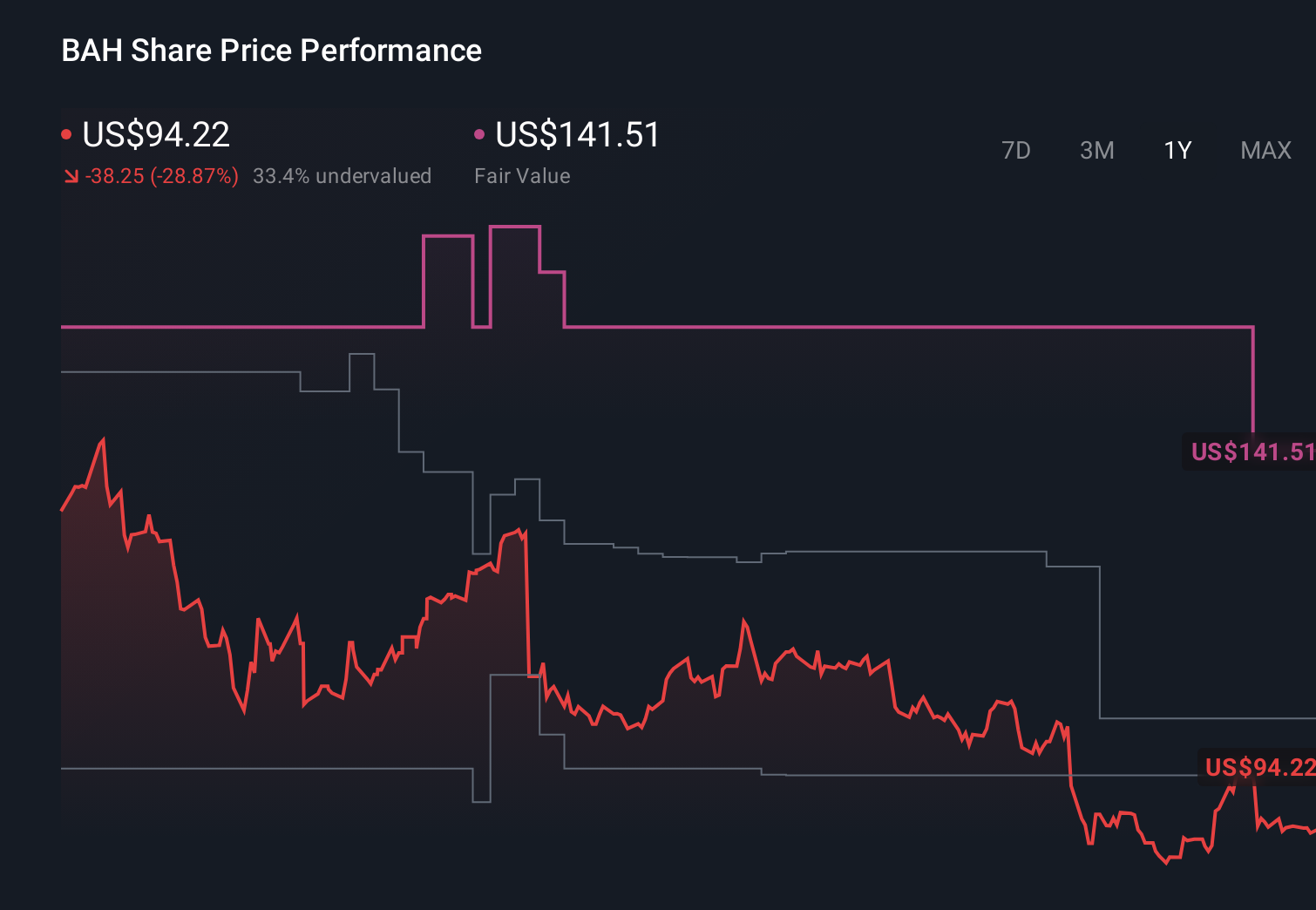

For Booz Allen Hamilton, you have to believe in a story where a traditional government-focused consultant steadily leans into higher-value, tech-driven cybersecurity solutions while managing uneven earnings and a heavy debt load. The launch of Vellox Reverser and the deeper role in Halcyon’s Incident Response Partner Program sharpen that story, reinforcing Booz Allen’s push to be seen as a full-spectrum cyber defense partner for both federal and commercial clients. In the near term, the bigger catalysts still sit around contract wins, margin discipline, and how management balances dividends, buybacks, and investment in AI tools like Vellox. Given recent share price weakness and forecasts for earnings to decline, these AI initiatives look more like incremental support for the investment case than a clear, near-term game changer, but they may slowly shift the risk balance away from pure consulting exposure.

However, Booz Allen’s high debt and forecast earnings decline remain issues investors should be aware of. Despite retreating, Booz Allen Hamilton Holding's shares might still be trading 46% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Explore 8 other fair value estimates on Booz Allen Hamilton Holding - why the stock might be worth 6% less than the current price!

Build Your Own Booz Allen Hamilton Holding Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Booz Allen Hamilton Holding research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Booz Allen Hamilton Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Booz Allen Hamilton Holding's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've found 11 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 106 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.