Is Booz Allen (BAH) Turning a Modest Earnings Outlook Into a Test of Its Strategy?

Booz Allen Hamilton Holding Corporation Class A BAH | 0.00 |

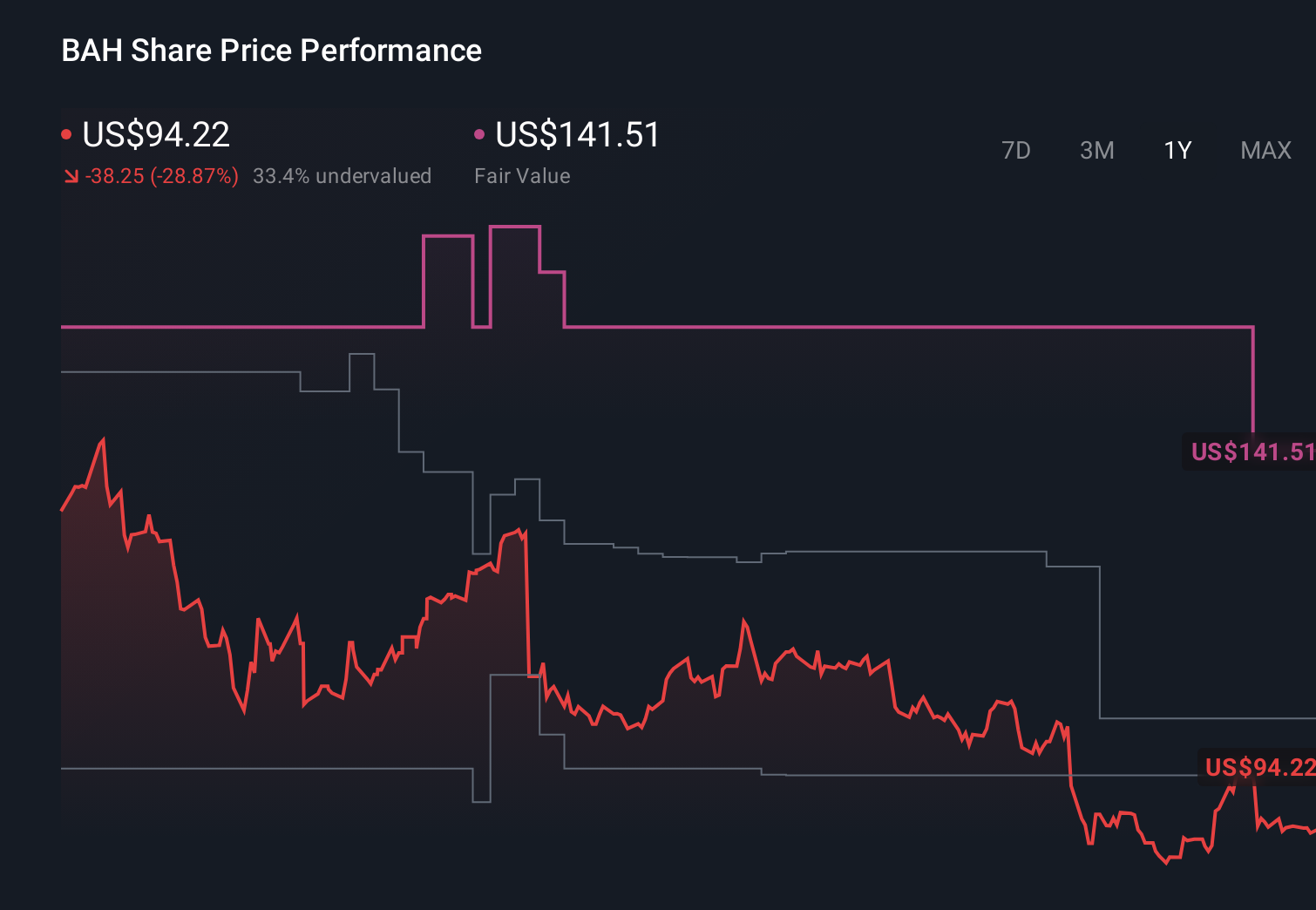

- In recent days, Booz Allen Hamilton drew investor attention as its shares lagged a rising market while anticipation built for its July 24, 2026 earnings report, which is expected to show modest earnings growth alongside a projected revenue decline.

- This combination of softer revenue expectations and upcoming results has sharpened focus on how closely analyst forecasts and management’s outlook align.

- Next, we’ll examine how concern over a projected revenue decline ahead of earnings may reshape Booz Allen Hamilton’s investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Booz Allen Hamilton Holding Investment Narrative Recap

To own Booz Allen Hamilton, you generally need to believe that its government focused AI, cyber, and consulting capabilities can continue to convert a large contract backlog into steady cash flows, even as contract structures and client needs evolve. The recent share pullback and expectation of modest earnings growth alongside lower revenue do not, by themselves, appear to alter the key near term catalyst, which is how management addresses revenue softness and backlog conversion on the upcoming earnings call, or the central risk around funding delays and procurement timing.

Among recent announcements, the May 18, 2026 expansion of Booz Allen’s collaboration with Anduril stands out as particularly relevant. It ties directly to one of the main upside catalysts: deeper integration into AI enabled defense and cyber missions. As investors weigh concerns about a projected revenue decline, this kind of partnership highlights how Booz Allen is embedding its software, zero trust, and mission systems into modern defense infrastructure, which may influence how you think about the resilience of its pipeline and backlog ahead of earnings.

Yet, beneath the focus on earnings timing, one risk in particular could matter much more for investors who are not watching closely...

Booz Allen Hamilton Holding’s narrative projects $12.3 billion revenue and $793.8 million earnings by 2029. This requires 3.0% yearly revenue growth and an earnings decrease of $51.2 million from $845.0 million today.

Uncover how Booz Allen Hamilton Holding's forecasts yield a $93.77 fair value, a 41% upside to its current price.

Exploring Other Perspectives

Compared with the baseline, the most bearish analysts sound far more cautious, assuming revenue grows only about 2.1 percent a year and earnings slip toward about US$764 million, so you may want to weigh their concerns about tighter budgets and shifting contract terms against the backlog story before deciding which version of Booz Allen’s future feels more realistic.

Explore 7 other fair value estimates on Booz Allen Hamilton Holding - why the stock might be worth just $93.77!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Booz Allen Hamilton Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Booz Allen Hamilton Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Booz Allen Hamilton Holding's overall financial health at a glance.

No Opportunity In Booz Allen Hamilton Holding?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.