Is Camden Property Trust a Bargain After Shares Drop 13% in 2025?

Camden Property Trust CPT | 104.02 | +2.38% |

- Thinking about whether Camden Property Trust might be a value opportunity? If you have been on the fence, now is a great time to take a closer look at how fairly the shares are priced.

- Camden’s stock has slipped, with a -4.0% change in both the past week and month, and is now down -12.8% year-to-date and -10.5% over the last year, despite a longer-term 19.7% gain over five years.

- Recent headlines have put a spotlight on the real estate sector, highlighting shifting demand in residential properties and ongoing interest rate uncertainty, both of which have fueled market volatility for REITs like Camden. Industry news around multifamily developments and urban migration trends has added further context to the moves in Camden’s share price.

- Camden Property Trust checks the undervalued box in 3 out of 6 key valuation factors, giving it a score of 3. However, there is more to the story than just the numbers. Next, we will break down exactly how Camden Property Trust’s valuation stacks up using several common analysis methods and reveal an even more insightful way to judge value at the end of the article.

Approach 1: Camden Property Trust Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a popular valuation approach that estimates the present value of a company by projecting its adjusted funds from operations into the future and discounting those cash flows back to today's value. This helps investors gauge what the business is intrinsically worth, based on its future cash-generating ability rather than short-term market swings.

For Camden Property Trust, the DCF model uses adjusted funds from operations as a proxy for free cash flow. The company reported free cash flow of $738.02 million over the last twelve months. Analysts have projected this figure to continue rising, with estimates gradually increasing to $810.79 million by 2029. Beyond 2029, further forecasts are generated using trend-based extrapolation. All values are stated in US dollars as the company reports and is listed in USD.

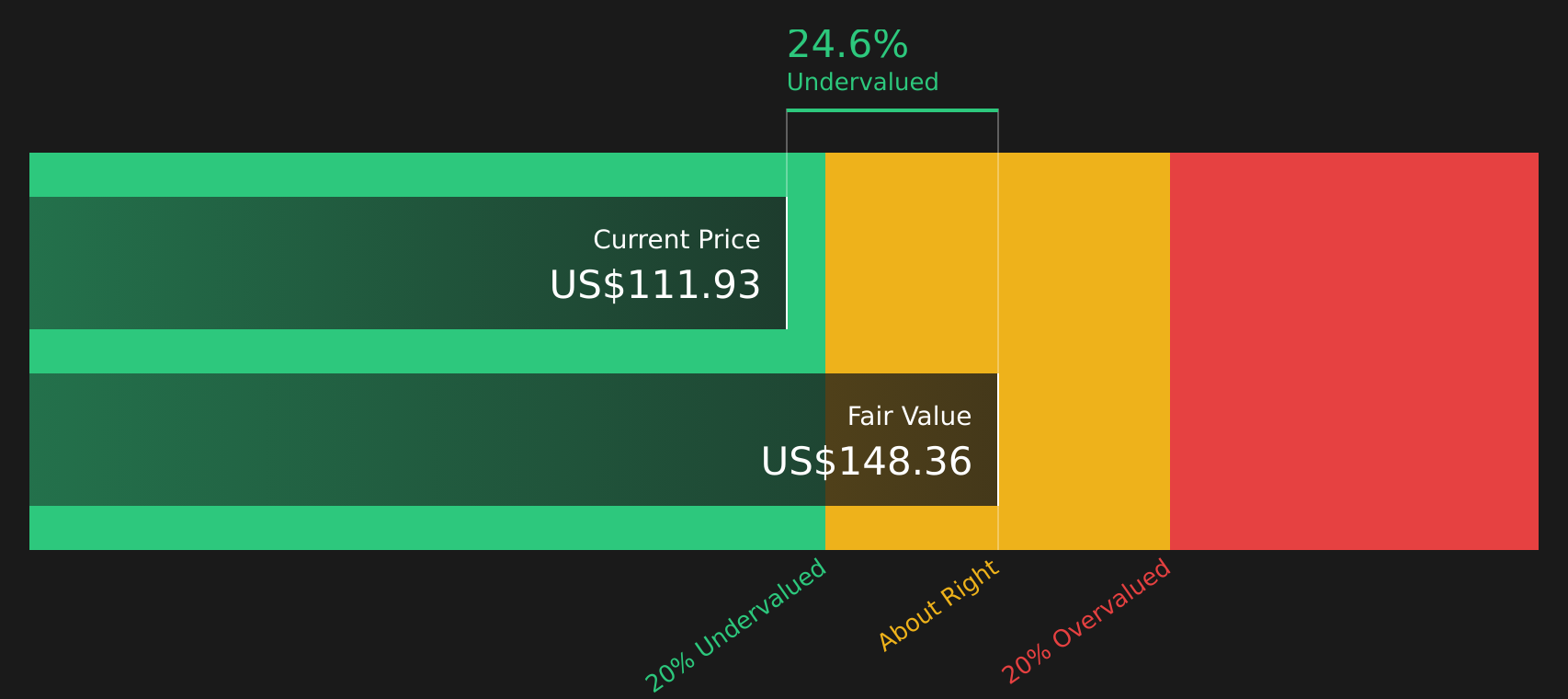

Based on this model, the estimated intrinsic value per share is $177.37. Compared to Camden’s current share price, this implies the stock is trading at a 43.6% discount. This suggests significant undervaluation according to the DCF approach.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Camden Property Trust is undervalued by 43.6%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

Approach 2: Camden Property Trust Price vs Earnings

For profitable companies, the Price-to-Earnings (PE) ratio is a widely used valuation tool because it measures how much investors are willing to pay for each dollar of a company's earnings. This metric makes it easier to compare companies regardless of their scale, and it is especially meaningful for businesses generating consistent profits like Camden Property Trust.

That said, what counts as a "normal" or "fair" PE ratio depends on company-specific growth prospects and risks. Investors are often willing to pay a higher PE for companies with faster expected earnings growth or lower risk. Slower growth or higher risk typically warrants a lower multiple.

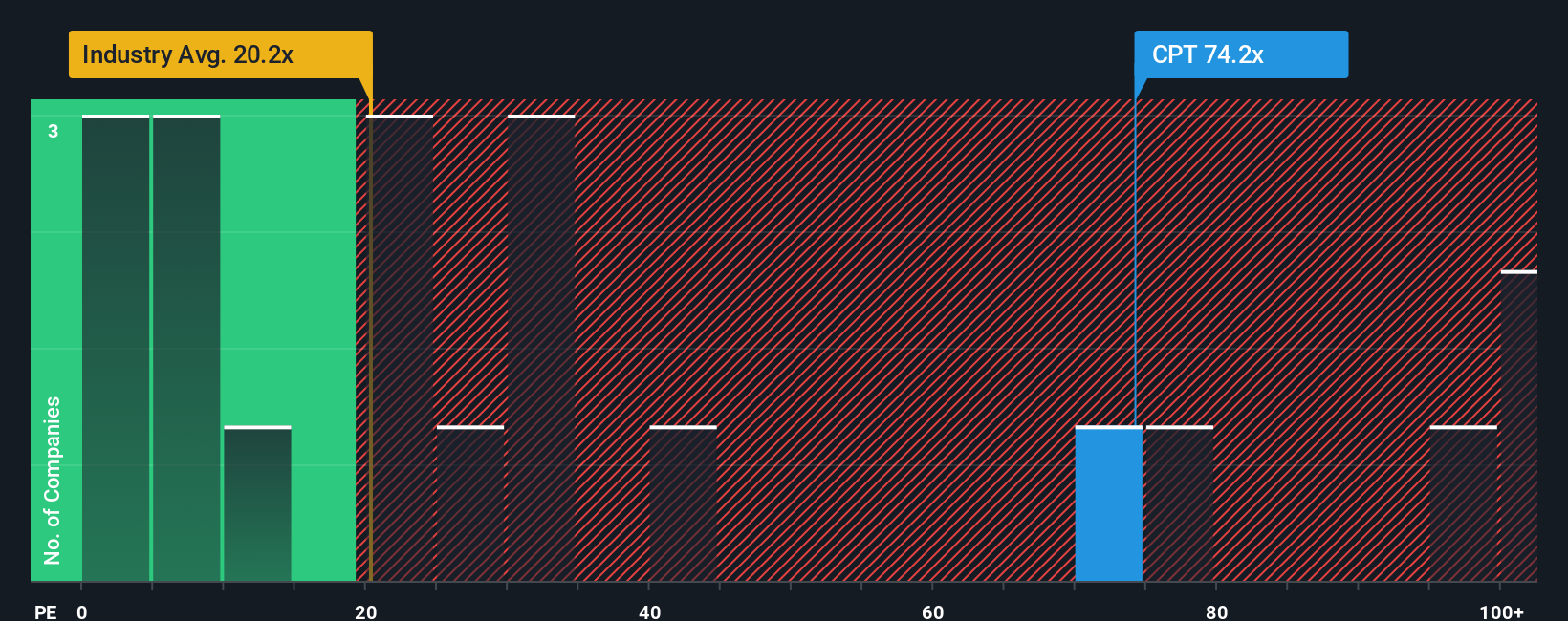

Camden Property Trust currently trades at a PE ratio of 68.6x. This is well above the average PE for Residential REITs at 19.3x and the peer group average of 35.7x. At first glance, this suggests Camden appears expensive versus its direct competition and the broader industry.

However, relying solely on these broad averages can be misleading. Simply Wall St's “Fair Ratio” takes a more nuanced approach by factoring in Camden’s specific growth outlook, profit margins, market cap, risks, and where it fits within its industry peers. This tailored assessment puts Camden’s fair PE ratio at 32.8x, a more accurate reflection of what a reasonable investor might pay for its shares today.

Comparing Camden’s current PE of 68.6x with its Fair Ratio of 32.8x, the stock looks significantly overvalued based on this approach.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Camden Property Trust Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Unlike traditional ratios and models, a Narrative is a powerful, yet approachable way to capture your own view of a company by telling its story. It combines your perspective on future revenue, earnings, and margins with what you believe is fair value.

A Narrative links Camden Property Trust’s unique story and business drivers to an informed financial forecast, then translates that into a fair value tailored to your outlook. Narratives are at the heart of the Simply Wall St Community page, where millions of investors can quickly build, revise, and share their views. This tool is designed to make investment decisions more personal and actionable, empowering you to compare your Narrative's fair value with the current share price so you can decide for yourself when to buy or sell.

The real advantage is that Narratives update as soon as key news or earnings data changes, keeping your assumptions and estimated value current without extra work. For Camden, for example, some investors are optimistic, forecasting robust Sun Belt growth, margin expansion, and setting 2028 price targets as high as $142. More cautious users highlight economic and supply risks with targets as low as $112. Narratives let you see and refine both sides, and find your own edge.

Do you think there's more to the story for Camden Property Trust? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.