Is Camtek (CAMT) A Bargain Following Its Shelf Registration And Earnings Caution?

Camtek Ltd CAMT | 0.00 |

Why Camtek's Shelf Registration Is Drawing Investor Attention

Camtek (NasdaqGM:CAMT) recently filed a US$182.24 million shelf registration for 1,000,000 common shares linked to an ESOP related offering, a move that can influence how investors think about future dilution.

This filing arrives shortly after Camtek stock declined 8.44% in a single session, with analysts expecting upcoming results to show slightly lower EPS but higher revenue, which is adding another layer of attention to the shares.

For context, Camtek's share price has retreated sharply in the short term, with a 1-day share price return of 8.53% and a 7-day return of 21.23% both declining. Meanwhile, the 1-year total shareholder return of 82% and 3-year total shareholder return of more than 3x suggest longer term momentum has been strong even as recent sentiment cools around the shelf registration and upcoming earnings.

If you are reassessing your semiconductor exposure after Camtek's recent moves, it could be worth scanning other chip-related opportunities through a focused list of 51 AI infrastructure stocks

With Camtek shares pulling back in the short term but still carrying strong multi year returns and analysts setting a higher price target than the last close, the key question is whether this recent weakness is a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 12% Undervalued

Compared with the last close at $153.72, the most widely followed narrative pegs Camtek's fair value higher, framing the recent pullback as part of a longer term story grounded in earnings and margin assumptions.

Accelerating demand for high-performance computing (HPC) and AI-driven applications is expanding the need for advanced packaging, micro-bump, and hybrid bonding inspection, directly growing Camtek's total addressable market and supporting multi-year revenue growth.

Curious what revenue pace, margin profile, and future P/E multiple are baked into that fair value tag for Camtek? The narrative leans on ambitious growth, richer profitability and a premium earnings multiple to keep that valuation in balance.

Result: Fair Value of $174.67 (UNDERVALUED)

However, the Camtek narrative could be tested if Asian revenue concentration encounters tougher geopolitics, or if large HPC customers trim spending or shift suppliers.

Another View on Camtek: Valuation Tension

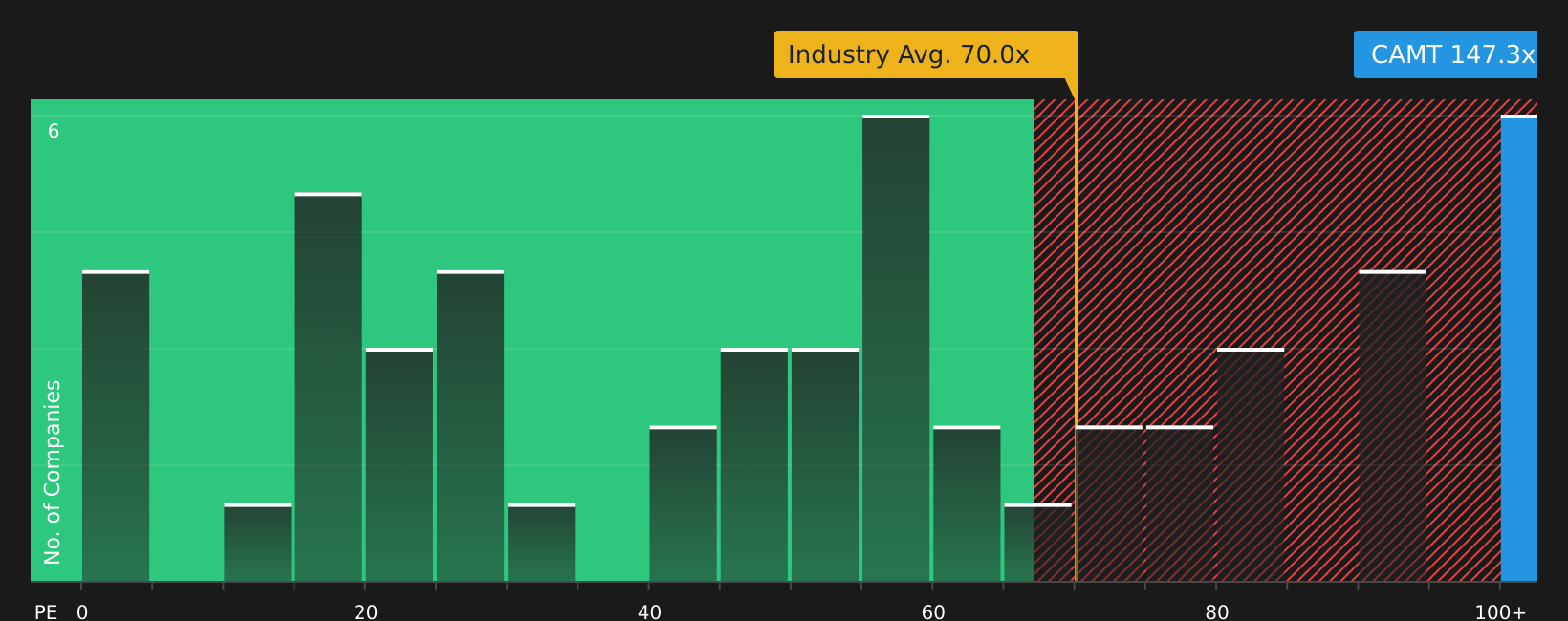

While the popular narrative tags Camtek as around 12% undervalued based on future earnings and margins, the current P/E of 147.3x tells a very different story. That is more than double the semiconductor industry at 70x, above peers at 133.7x, and almost twice the Simply Wall St fair ratio of 74.7x. This implies far less room for error if growth or margins fall short. Is this rich multiple a sign of over enthusiasm, or is the market correctly pricing hard to repeat growth?

Next Steps

With Camtek's mixed signals on valuation and sentiment, now is the time to review the underlying data yourself and weigh both sides of the story with 2 key rewards and 3 important warning signs

Looking For More Investment Ideas Beyond Camtek?

If Camtek has your attention, do not stop there. A few minutes with targeted stock lists could surface opportunities you regret skipping later.

- Target consistent value by scanning companies that screen as 44 high quality undervalued stocks and compare how their fundamentals stack up against your current watchlist.

- Prioritise resilience by focusing on businesses that appear in the 71 resilient stocks with low risk scores and check which ones line up with your risk tolerance.

- Spot potential early movers by reviewing the screener containing 19 high quality undiscovered gems and see which stories the broader market may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.