Is Camtek (CAMT) Fairly Valued On Its Recent Pullback?

Camtek Ltd CAMT | 0.00 |

Camtek (NasdaqGM:CAMT) drew attention after its shares fell 5.9% on July 7, 2026, following concerns that the stock trades above one intrinsic value estimate, raising fresh questions about valuation risk.

That 5.9% drop sits within a wider cooling in Camtek’s momentum, with the share price down 18.3% over the past week and 21.7% over 90 days. At the same time, the year to date share price return is 15.4% and the 1 year total shareholder return is 50.9%. This points to strong longer term gains alongside a recent reassessment of valuation risk.

If Camtek’s recent volatility has you rethinking where to focus next, this could be a good moment to see which other chip related opportunities stand out in our 52 AI infrastructure stocks

Camtek now trades below the average analyst price target yet above one intrinsic value estimate, putting the recent pullback in a grey zone. Is this a reasonable discount or a warning that caution is still warranted?

Most Popular Narrative: 28.8% Undervalued

Compared with Camtek’s last close at $133.26, the most followed narrative points to a fair value of $187.25. This frames the recent pullback as a valuation gap rather than a completed reset.

Accelerating demand for high-performance computing (HPC) and AI-driven applications is expanding the need for advanced packaging, micro-bump, and hybrid bonding inspection, directly growing Camtek's total addressable market and supporting multi-year revenue growth.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that higher fair value for Camtek? The narrative leans on compounding revenue, sharply higher margins and a future earnings multiple that still assumes discipline. If you are curious which exact earnings and revenue paths underpin that $187.25 figure and how a higher discount rate still supports it, the full narrative lays those assumptions out in black and white.

Result: Fair Value of $187.25 (UNDERVALUED)

However, that bullish Camtek narrative still faces real pressure points, including heavy reliance on Asian demand and concentrated high bandwidth memory customers, whose spending plans could change quickly.

Another View On Camtek’s Valuation

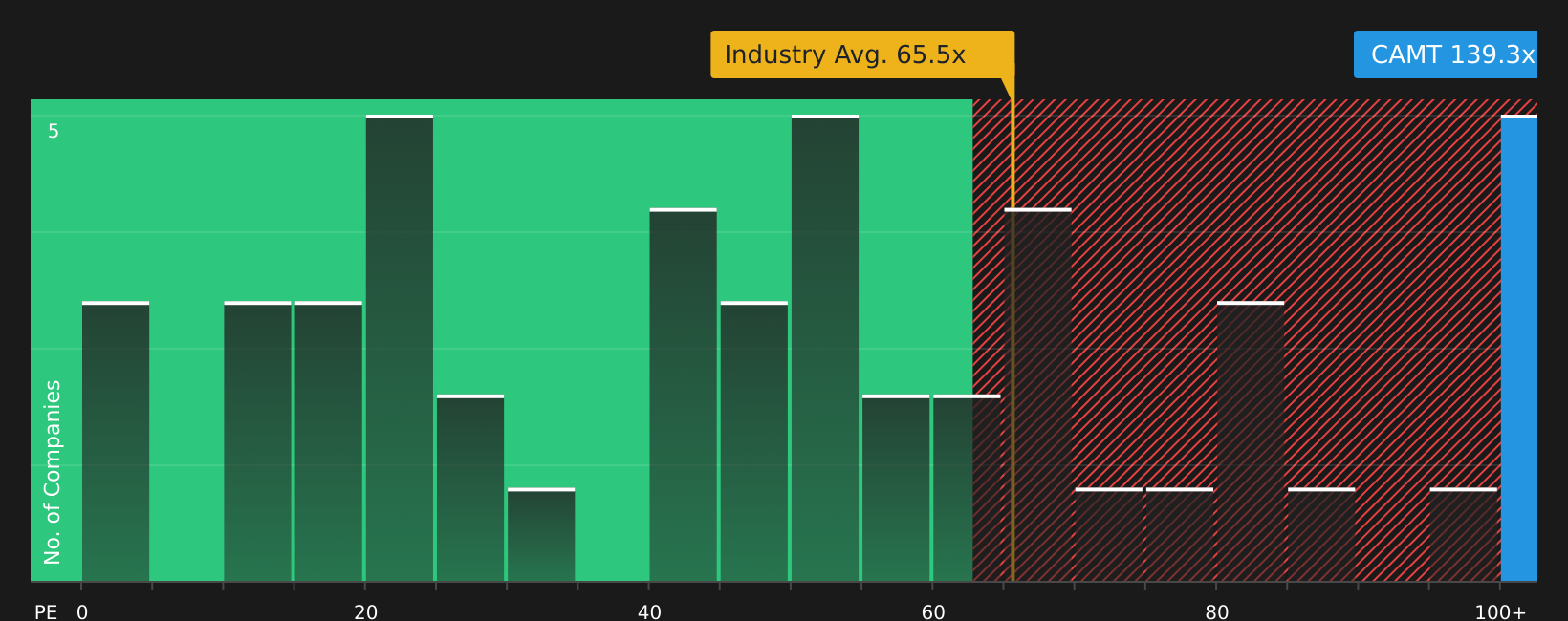

While the narrative fair value suggests Camtek is 28.8% undervalued, the market’s current P/E of 127.7x tells a different story. That multiple is roughly double the US Semiconductor industry average of 65.3x and also far above a fair ratio of 62.7x, which implies richer pricing and higher valuation risk if earnings stumble. Which signal do you give more weight to?

For a closer look at how this valuation gap could close over time, check the detailed comparison in our See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and concern around Camtek leaves you undecided, take a moment to review the numbers yourself and move quickly to form your own stance. You can start with the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Camtek?

If Camtek has sharpened your focus on valuation and risk, do not stop here. Fresh opportunities elsewhere could end up shaping your next big investing decision.

Use the Simply Wall Street Screener to quickly surface stocks that fit your style and avoid getting stuck on a single story.

- Target potential mispricings by scanning for companies trading at attractive valuations using the 44 high quality undervalued stocks.

- Prioritize resilience by filtering for businesses with strong finances in the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for under followed opportunities that the market may be overlooking through the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.