Is Camtek (CAMT) Quietly Redefining Its AI Packaging Edge With New CoWoS-Like Orders?

Camtek Ltd CAMT | 176.51 176.60 | +3.77% +0.05% Pre |

- Camtek Ltd. recently announced it received a multi-system order worth US$31 million from a leading OSAT for CoWoS-like packaging geared toward AI applications, bringing first-quarter 2026 OSAT orders to over US$90 million, with systems scheduled for delivery within this year.

- This surge in advanced packaging demand from outsourced assembly and test providers highlights Camtek’s growing role in inspection and metrology for AI-focused semiconductor manufacturing workflows.

- Next, we’ll assess how this influx of CoWoS-like AI packaging orders might reshape Camtek’s investment narrative around advanced packaging growth.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Camtek Investment Narrative Recap

To own Camtek, you need to believe inspection and metrology will stay central to AI-driven advanced packaging, especially at OSATs, while accepting concentrated exposure to a few HPC and HBM customers and Asia-centric revenues. The new US$31 million CoWoS-like order, lifting Q1 2026 OSAT orders above US$90 million, directly supports the near term catalyst of advanced packaging demand, but also heightens the key risk that any slowdown or supplier shift by these customers could hit orders hard.

The recent US$25 million Hawk systems order from a tier 1 IDM for AI applications is especially relevant here, because it shows Camtek gaining traction for its newer platforms alongside the OSAT momentum. Together with the CoWoS-like OSAT wins, Hawk adoption reinforces the catalyst that higher value, AI focused tools can deepen Camtek’s role in advanced packaging, even as investors weigh execution risks, competition and exposure to semiconductor spending cycles.

Yet beneath the strong AI order headlines, one risk that investors should be aware of is how dependent Camtek still is on a relatively narrow set of...

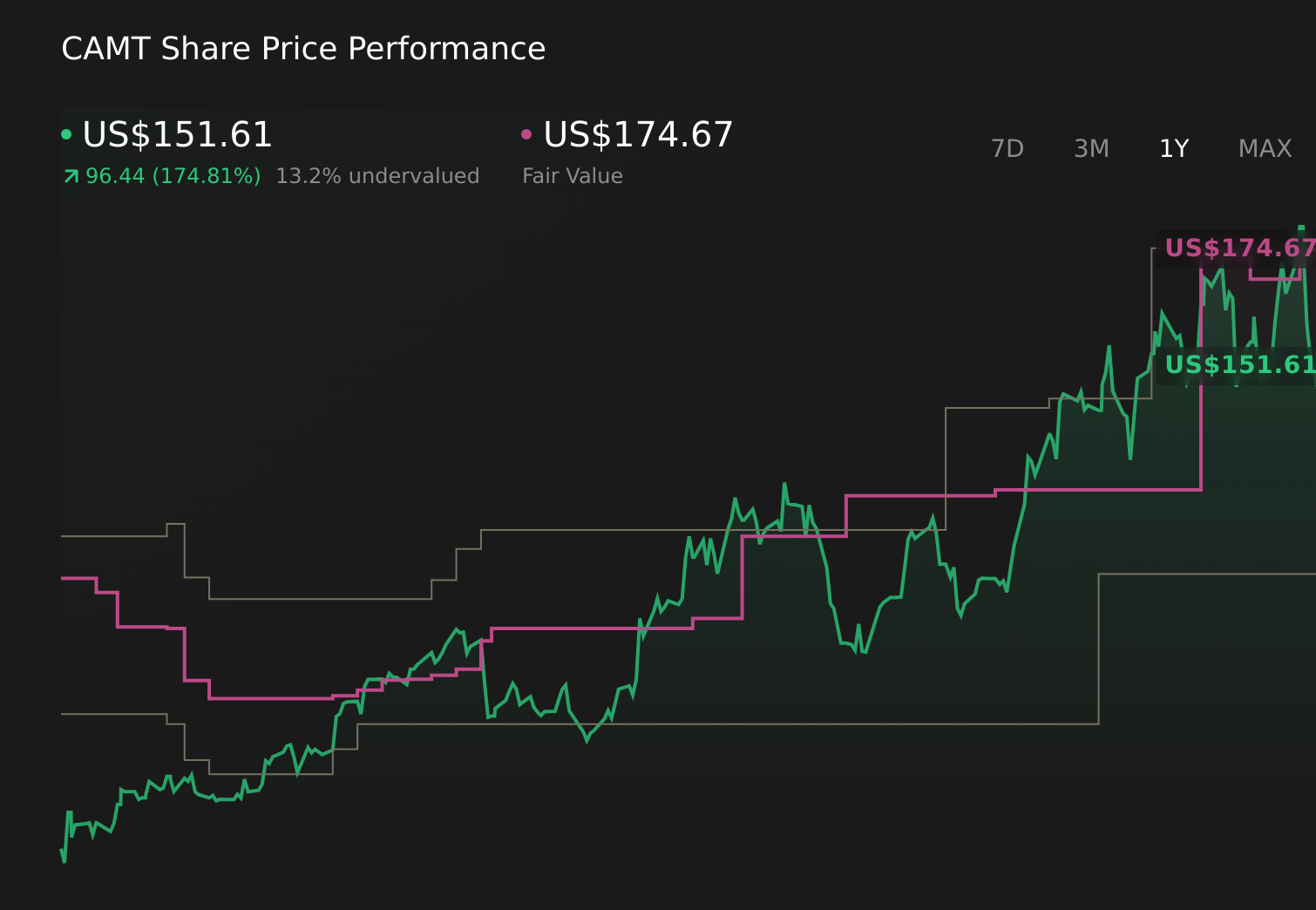

Camtek’s narrative projects $786.7 million revenue and $314.9 million earnings by 2029. This requires 16.6% yearly revenue growth and about a $264 million earnings increase from $50.7 million today.

Uncover how Camtek's forecasts yield a $174.67 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about US$548.8 million of revenue and US$163.9 million of earnings by 2028, so if you are worried about Camtek’s heavy HPC exposure and collection risks, this new AI focused OSAT backlog could either soften those concerns or deepen them, depending on how you see concentration and volatility playing out over time.

Explore 3 other fair value estimates on Camtek - why the stock might be worth as much as 15% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Camtek research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Camtek research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Camtek's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.