Is Carvana (CVNA) Undervalued After Its Milwaukee Same Day Delivery Expansion?

Carvana CVNA | 0.00 |

Carvana (CVNA) is back in focus after expanding same-day delivery and pickup to the greater Milwaukee area. This move draws attention to how its online used-car model and logistics may influence the stock.

The Milwaukee launch comes as Carvana’s recent momentum is mixed, with the 1 day share price return of 8.29% and 1 month share price return of 9.80% contrasting with a share price decline of 12.08% year to date and a very large 3 year total shareholder return around 8 times the initial value. This suggests that long term holders still sit on sizeable gains even as shorter term sentiment has cooled.

If the same day delivery story has you rethinking what online platforms can do, it may be a good time to broaden your search with the 18 top founder-led companies

Bulls see Carvana’s Milwaukee rollout as proof its logistics scale can support a higher valuation, while bears worry about capital intensity and margin risk. Which case fits the current revenue, profit and market pricing better?

Most Popular Narrative: 24% Undervalued

On the numbers, the most followed Carvana narrative points to a fair value of $92.10 against a last close of $70.38, putting its long term story under the microscope.

The company''s scaled logistics and reconditioning infrastructure, bolstered by the integration of ADESA locations, is driving lower delivery and inbound transport costs. As utilization rises, these investments are expected to further enhance operating leverage, improving gross margins and profitability.

Want to see what kind of revenue growth, margin profile and earnings power this narrative assumes for Carvana? The model leans on compounding volume, rising efficiency and a premium profit multiple. Curious how those ingredients combine to reach that fair value.

Result: Fair Value of $92.10 (UNDERVALUED)

However, Carvana’s story can change quickly if expansion spending at ADESA sites keeps margins under pressure, or if intensifying digital competition caps unit growth and pricing power.

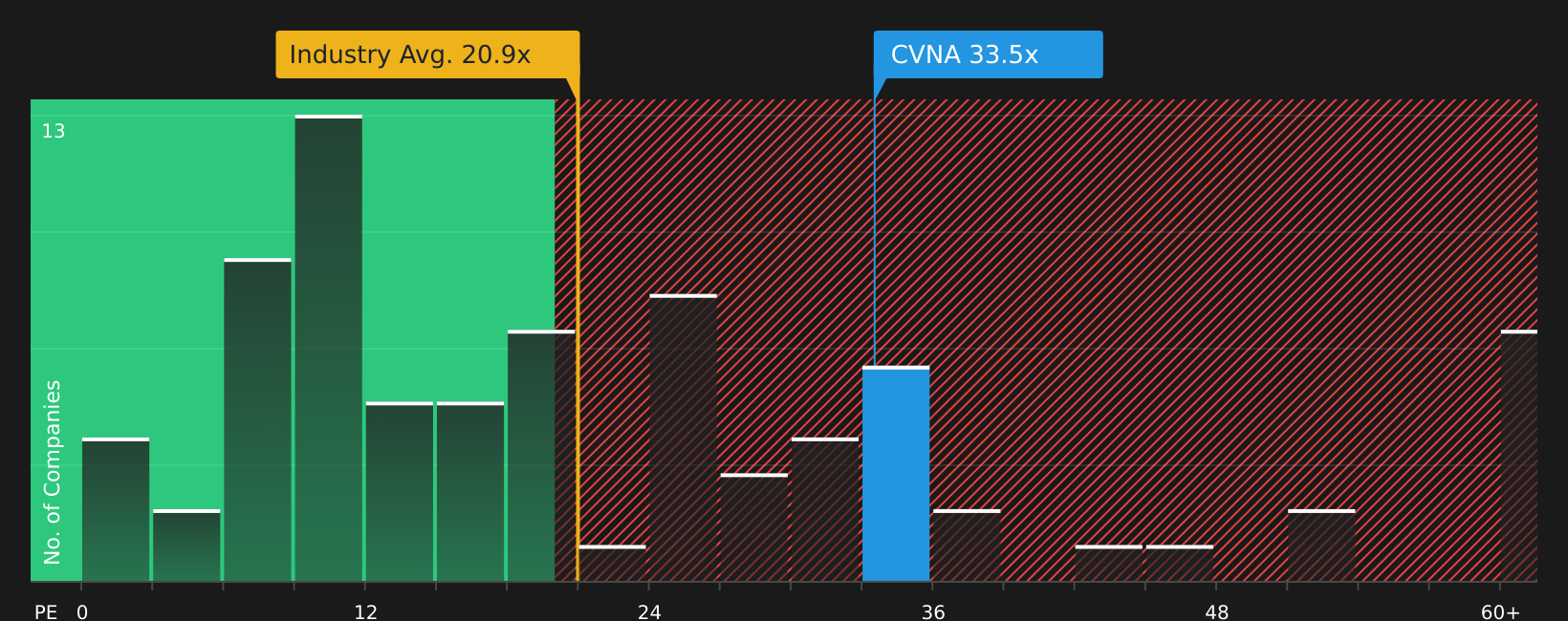

Another View: What Carvana’s P/E Ratio Signals

While the leading Carvana narrative leans on cash flow and long term fair value near $92, the current P/E of 35x paints a different picture. It sits well above both the US Specialty Retail average of 20.4x and a fair ratio of 29.4x, which implies higher valuation risk if expectations slip.

For a closer look at how this pricing stacks up against earnings, margins and peers, take a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Carvana’s mix of concerns and positives in mind, act promptly to review the underlying data and decide where you stand by checking the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Carvana?

If Carvana has sharpened your thinking, do not stop here. Widen your opportunity set with focused stock lists built from the Simply Wall St screener.

- Target potential mispricings by reviewing companies screened as 44 high quality undervalued stocks.

- Strengthen your focus on financial resilience by checking the solid balance sheet and fundamentals stocks screener (48 results).

- Aim for staying power in your portfolio by reviewing income opportunities in the 8 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.