Is Clover Health (CLOV) Quietly Redefining Its Medicare Advantage Strategy With This Leadership Shift?

Clover Health CLOV | 0.00 |

- Clover Health Investments reported that Brady Priest stepped down earlier this month as CEO of Clover Care Services, its home-care arm, with his responsibilities folded into the existing executive leadership to more tightly link home-care with the broader business.

- The decision not to appoint a new Clover Care Services CEO underscores management’s push to more closely integrate its home-care operations with the company’s core Medicare Advantage-focused model.

- Now we’ll examine how this leadership change, alongside the Medicare star rating upgrade, could influence Clover Health’s broader investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Clover Health Investments Investment Narrative Recap

To own Clover Health today, you need to believe its technology-centric Medicare Advantage model can translate improving operations into durable profitability, while managing regulatory and cost pressures. In that context, consolidating Clover Care Services leadership into the core team looks incremental rather than transformational, and does not materially change the near term catalyst of the 4 star Medicare payment year or the key risk that higher medical and pharmacy utilization could squeeze margins again.

The most relevant recent development is the Medicare star rating upgrade to 4.5 Stars for Clover’s PPO plans following a favorable court ruling. That upgrade supports higher CMS reimbursements in the 2026 payment year, directly tied to the same integrated care model that includes Clover Care Services. Together, the rating improvement and tighter home care integration strengthen the link between care coordination, potential margin benefits, and the company’s central investment thesis.

Yet, against this improving operational story, investors should be aware of how sensitive Clover’s margins remain to shifts in medical and pharmacy costs...

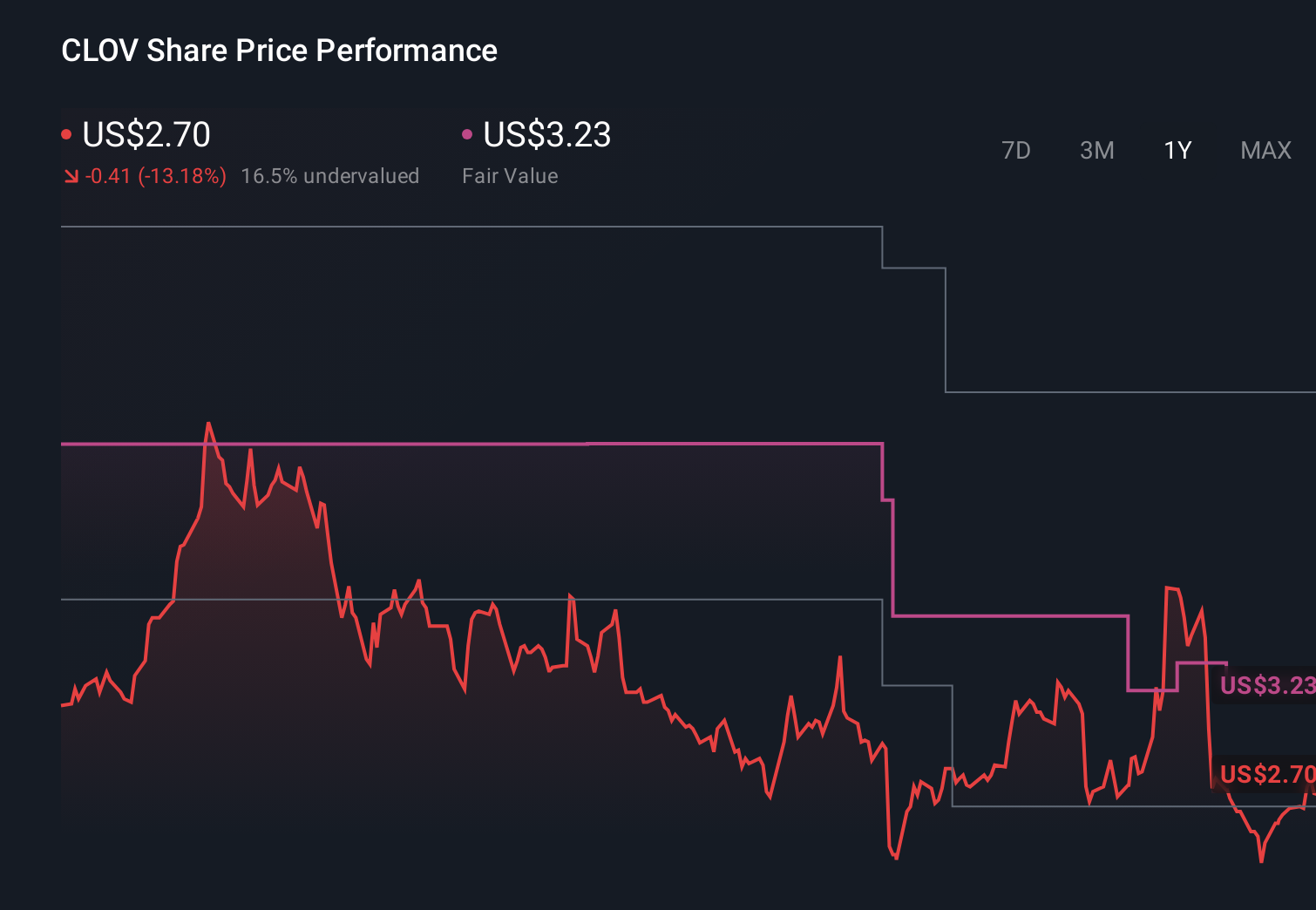

Clover Health Investments' narrative projects $4.0 billion revenue and $30.9 million earnings by 2029. This requires 21.8% yearly revenue growth and a $87.8 million earnings increase from -$56.9 million today.

Uncover how Clover Health Investments' forecasts yield a $3.15 fair value, a 39% downside to its current price.

Exploring Other Perspectives

While consensus focuses on star rating upside and integration benefits, the most cautious analysts stress that even with US$3.8 billion revenue and US$26.3 million earnings by 2029, rich valuation expectations and rising cost pressures could still limit returns, which shows just how differently you and other investors might view the same set of headlines.

Explore 5 other fair value estimates on Clover Health Investments - why the stock might be worth 39% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Clover Health Investments research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Clover Health Investments research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Clover Health Investments' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.