Is Constellation Brands (STZ) Pricing Offer An Opportunity After Mixed Multi Year Returns

Constellation Brands, Inc. Class A STZ | 151.20 | +0.07% |

- If you are wondering whether Constellation Brands is fairly priced or offering value right now, you are not alone.

- The share price closed at US$165.63, with returns of 3.1% over 7 days, 12.7% over 30 days, 17.3% year to date, but only 3.2% over 1 year and a 22.2% decline over both 3 and 5 years.

- These mixed returns put the spotlight on what might be driving sentiment shifts around Constellation Brands. Recent coverage has focused on how investors are weighing the company against other large beverage names and debating whether current pricing properly reflects its long term prospects.

- On Simply Wall St's 6 point valuation checklist, Constellation Brands scores 2 out of 6. Next we will look at what that score means across different valuation methods, and why there may be an even better way to think about value that we will come back to at the end.

Constellation Brands scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Constellation Brands Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting future cash flows and then discounting those back to a present value.

For Constellation Brands, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $1.59b. Analyst and extrapolated estimates suggest Free Cash Flow rising to around $2.35b by 2030, with a series of annual projections between 2026 and 2035 that are discounted back to today using Simply Wall St’s assumptions.

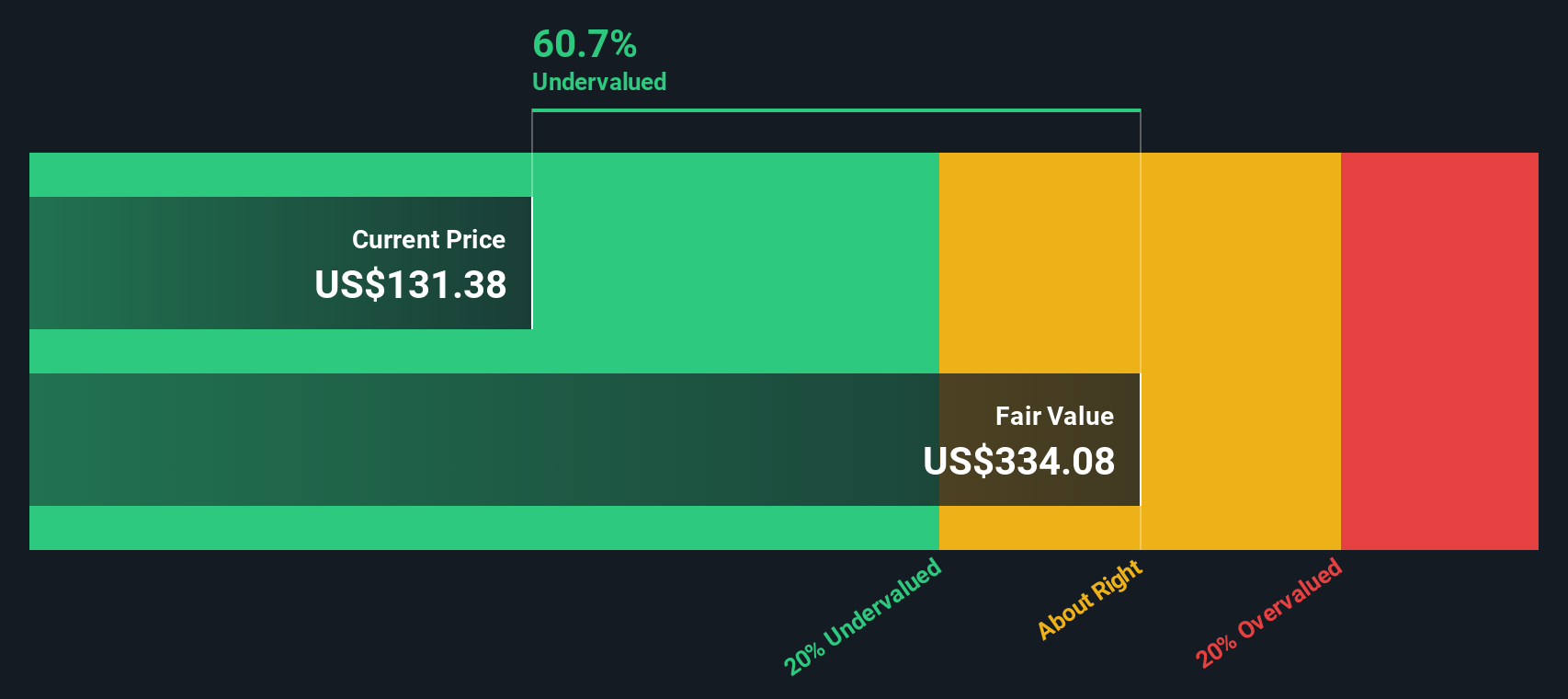

When all those discounted cash flows are added up, the model arrives at an estimated intrinsic value of about $321.34 per share. Against the recent share price of $165.63, this implies the stock is 48.5% undervalued according to this specific DCF framework.

This is a sizeable gap, so if you place weight on long term cash generation, the DCF view suggests Constellation Brands may currently be pricing in a lot of caution.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Constellation Brands is undervalued by 48.5%. Track this in your watchlist or portfolio, or discover 52 more high quality undervalued stocks.

Approach 2: Constellation Brands Price vs Earnings

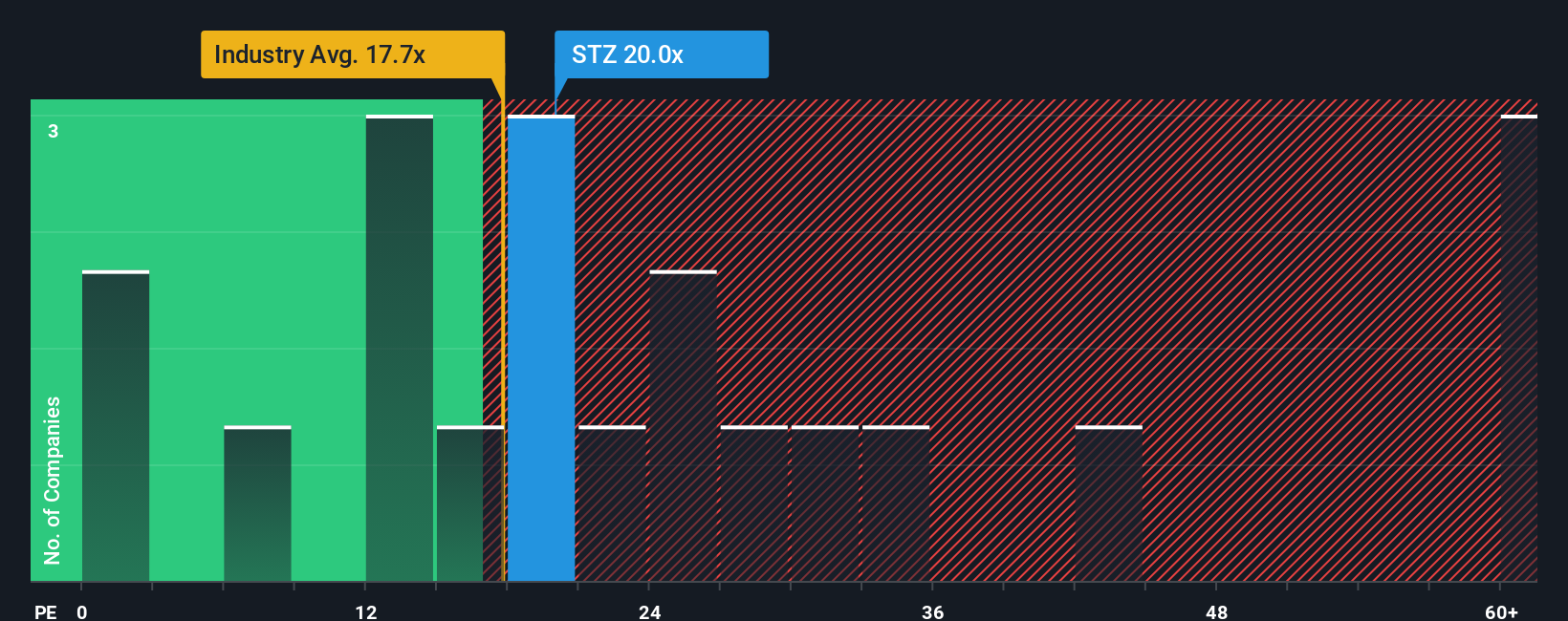

For a profitable company like Constellation Brands, the P/E ratio is a useful way to relate what you pay per share to the earnings the business is already generating. It helps you see how many dollars of price the market is attaching to each dollar of current earnings.

What counts as a “normal” P/E often reflects how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth or higher risk tends to align with a lower multiple.

Constellation Brands currently trades on a P/E of 25.88x. That sits above the Beverage industry average of 17.51x and also above the peer group average of 20.20x. Simply Wall St’s Fair Ratio for Constellation Brands is 23.64x, which is the P/E level its model suggests based on factors like earnings growth, industry, profit margins, market cap and company specific risks.

The Fair Ratio can be more tailored than a simple comparison with peers or the broad industry because it adjusts for those company specific characteristics, rather than assuming all beverage stocks deserve the same multiple. With the current P/E of 25.88x sitting above the Fair Ratio of 23.64x, the shares screen as somewhat expensive on this measure.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Constellation Brands Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives, where you set out your story for Constellation Brands, link it to explicit forecasts for revenue, earnings and margins, and the platform turns that into a Fair Value you can compare with the current price. You can keep this updated as news or earnings arrive, and see it alongside other investors on the Community page. Examples range from a more optimistic view that supports a Fair Value around US$220 with assumptions for revenue growth and higher margins, through to a cautious view closer to US$118 that reflects softer revenue assumptions and a lower future P/E, so you can decide which story feels closest to your own expectations.

For Constellation Brands however we will make it really easy for you with previews of two leading Constellation Brands Narratives:

Fair value in this bullish narrative: about US$170.73 per share

Implied pricing gap to that fair value: roughly 3.0% undervalued versus the last close of US$165.63

Revenue growth assumption used in the model: very large, close to 1x current revenue

- Analysts in this camp see Wine & Spirits restructuring and divestitures supporting higher margins and enterprise wide cost savings by fiscal 2028.

- They anchor on strong cash generation and investment in the beer business, alongside share repurchases and a set dividend payout ratio, to support earnings over time.

- This view assumes margins improve, earnings reach about US$2.2b by 2028 and the shares trade on a mid teens P/E that sits below the current industry level used in the narrative.

Fair value in this bearish narrative: US$118.00 per share

Implied pricing gap to that fair value: about 40.4% overvalued versus the last close of US$165.63

Revenue growth assumption used in the model: 3.41% annual decline

- This narrative leans on softer long term revenue expectations, with alcohol moderation trends and alternatives seen as a drag on volumes and pricing power.

- It highlights reliance on Mexican import beers, regulatory and tax risks, and higher input costs as key pressures on margins and earnings stability.

- The fair value ties to a future P/E in the low teens, alongside assumptions of declining revenue to around US$8.7b and earnings of about US$2.1b by 2028.

If you want to go beyond these previews and see how other investors are framing the upside and downside, it is worth reading the full bull and bear narratives, then weighing them against your own expectations for the business.

Do you think there's more to the story for Constellation Brands? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.