Is Copa Holdings (CPA) Still Attractive After Recent Volatility And DCF Valuation Check

Copa Holdings, S.A. Class A CPA | 0.00 |

- If you are wondering whether Copa Holdings at around US$135.84 still offers value, the key question is how its current price stacks up against a range of valuation measures.

- The stock has been volatile recently, with a decline of 5.0% over the past week, a 22.4% gain over the last 30 days, and returns of 11.5% year to date and 34.0% over the past year.

- That mix of short term weakness and stronger longer term returns has put Copa Holdings back on many investors' radars, especially as the broader airlines space keeps reacting to shifting expectations around travel demand and costs. Recent coverage has focused on how airline stocks are pricing in these themes, which directly influences how investors judge whether Copa's move is overdone or justified.

- Copa Holdings currently scores 5 out of 6 on Simply Wall St's valuation checks, giving it a valuation score of 5. The sections that follow will compare what different valuation methods say about that price, then finish with a more complete way to think about what the stock might be worth.

Approach 1: Copa Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a stock could be worth by projecting future cash flows and discounting them back to today, using the idea that cash received in the future is worth less than cash in hand now.

For Copa Holdings, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $356.95 million. Analysts supply nearer term estimates, such as $347 million for 2026 and $423 million for 2027. Simply Wall St then extrapolates further, with projected Free Cash Flow reaching about $755.44 million in 2035 based on the provided 10 year path.

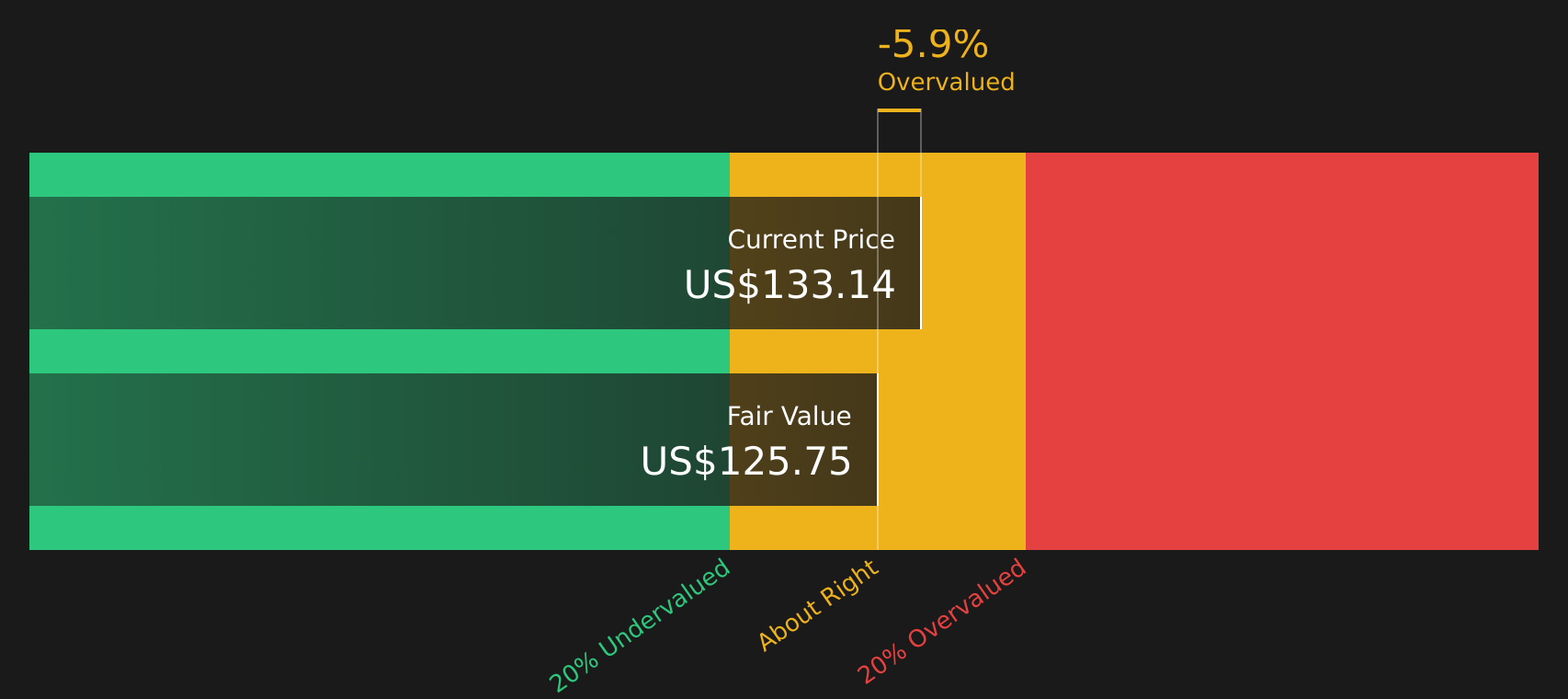

Pulling these cash flows together, the DCF model arrives at an estimated intrinsic value of about $149.67 per share. Compared with a recent share price around $135.84, this calculation suggests the stock is about 9.2% undervalued on these assumptions, which is a relatively small gap.

Result: ABOUT RIGHT

Copa Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Copa Holdings Price vs Earnings

For profitable companies, the P/E ratio is a useful yardstick because it ties what you pay for the stock directly to the earnings the business is already generating. Investors typically accept a higher or lower P/E depending on what they expect for future earnings growth and how risky those earnings appear to be. Higher expected growth or lower perceived risk can support a higher P/E, while slower growth or higher risk usually point to a lower P/E as more reasonable.

Copa Holdings currently trades on a P/E of about 7.86x. This sits below the Airlines industry average P/E of roughly 9.06x, and well below the peer average of around 30.68x. Simply Wall St also calculates a proprietary “Fair Ratio” for Copa Holdings of 16.77x, which is the P/E that would typically be expected given factors such as its earnings growth profile, industry, profit margin, market cap and risk characteristics.

This Fair Ratio can be more useful than a simple comparison with peers or the industry because it adjusts for company specific traits rather than assuming every airline should trade on the same multiple. Since Copa Holdings' current P/E of 7.86x is below the Fair Ratio of 16.77x, the stock screens as undervalued on this measure.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Copa Holdings Narrative

Earlier it was mentioned that there is an even better way to think about valuation. Narratives on Simply Wall St let you turn your view of Copa Holdings into a clear story that connects your assumptions about future revenue, earnings and margins to a forecast and a Fair Value. This then updates automatically as new news or earnings arrive and can be compared to the current share price to help you decide whether the stock looks expensive or cheap based on your own view, whether that is closer to a cautious Fair Value around US$128.87 or a more optimistic Fair Value around US$185.00 shown in the Community page, rather than relying only on a single static P/E or analyst target.

For Copa Holdings however, we will make it really easy for you with previews of two leading Copa Holdings Narratives:

Start with the bullish case if you think the current price does not fully reflect Copa's long term potential, then balance that with the more cautious bear case so you can see what would need to go right or wrong for each view to play out.

Fair Value: US$185.00

Implied discount to this Fair Value at US$135.84: about 26.6% undervalued

Analyst revenue growth assumption: about 12.42% a year

- Analysts taking this view see faster revenue growth supported by aircraft deliveries, capacity expansion and Copa's digital platforms improving efficiency and ancillary sales.

- They expect profit margins to improve, with cost control, premium cabins and a strong hub position helping Copa keep earnings efficiency high.

- This camp ties its Fair Value to earnings potentially reaching about US$1.1b by 2029 and a future P/E of 9.8x, which is close to where the US Airlines industry P/E sits in the data provided.

Fair Value: about US$128.87

Implied premium to this Fair Value at US$135.84: about 5.4% overvalued

Analyst revenue growth assumption: about 8.07% a year

- Analysts in this camp highlight risks from overcapacity, softer yields and tougher competition, which could limit revenue growth and pressure pricing power over time.

- They also focus on exposure to the Panama hub, environmental costs and regional volatility, which could keep margins and earnings under pressure.

- Here the Fair Value is tied to earnings of about US$917.7m by 2029 on a lower future P/E of 7.8x, with buybacks and current load factors seen as helping near term metrics but not removing longer term risk.

Once you have a sense of which Copa Holdings narrative sounds closer to your own view on growth, margins and risk, you can use those Fair Values as a reference point against the current share price rather than relying only on a single model or ratio.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Copa Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Copa Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.