Is Costco Wholesale (COST) Priced Too High After Strong Multi Year Share Price Gains

Costco Wholesale COST | 0.00 |

- Investors may be asking whether Costco Wholesale at US$1,048.95 is offering good value today, or if the price already reflects everything currently expected by the market.

- The stock has returned 4.0% over the past week, 6.5% over the past month, 22.8% year to date and 2.8% over the last year. The 3 year and 5 year returns are 119.9% and 190.8% respectively.

- Recent attention on Costco Wholesale has focused on its role as a large US consumer retail stock. Investors have been weighing its scale, membership model and position in the sector. This backdrop helps explain why the share price has been active over multiple time frames as the market reassesses what that combination of factors might be worth.

- Simply Wall St currently assigns Costco Wholesale a valuation score of 0 out of 6. Next is a closer look at how different valuation approaches line up on the stock and why an additional, broader way of thinking about value at the end of this article could be especially useful.

Costco Wholesale scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

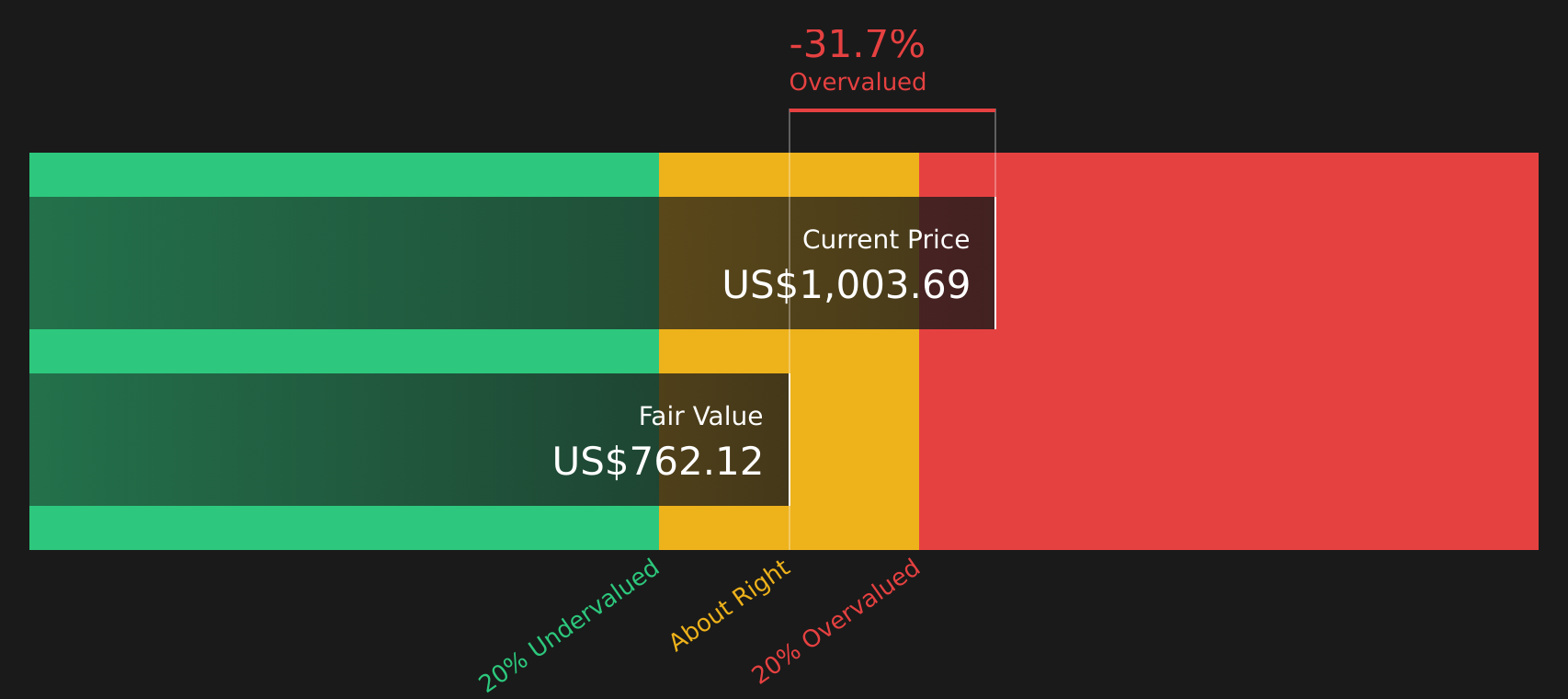

Approach 1: Costco Wholesale Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting its future cash flows and then discounting those back to today using a required return. It is essentially asking what future dollars are worth in present day terms.

For Costco Wholesale, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $9.50b. Analyst estimates and extrapolations suggest projected free cash flow of $11.66b by 2029, with a series of annual projections out to 2035 that are discounted back to reflect the time value of money and risk.

Aggregating these discounted cash flows, Simply Wall St arrives at an estimated intrinsic value of $751.43 per share for Costco Wholesale. Compared with the current share price of $1,048.95, this DCF output indicates the stock is about 39.6% above the model’s estimate of fair value. This points to the shares looking expensive on this specific cash flow framework.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Costco Wholesale may be overvalued by 39.6%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Costco Wholesale Price vs Earnings

For a profitable company like Costco Wholesale, the P/E ratio is a useful way to relate what you are paying for the stock to the earnings it is currently generating. A higher or lower P/E often reflects what the market is willing to pay today for each dollar of earnings, given its expectations and perceived risk.

In general, higher growth expectations and lower perceived risk can support a higher P/E, while slower growth and higher risk tend to be associated with a lower, more cautious multiple. Costco Wholesale currently trades on a P/E of 54.44x. That compares with an industry average P/E of 17.93x for Consumer Retailing and a peer average of 22.98x, so the stock is currently priced at a premium to both groups.

Simply Wall St also provides a proprietary “Fair Ratio” of 41.03x for Costco Wholesale. This aims to show what a reasonable P/E might look like after considering factors such as earnings growth, profit margins, size, risk profile and its specific industry. Because it folds these elements into one figure, it can be more informative than a simple peer or industry comparison. Here, the current P/E of 54.44x is above the Fair Ratio of 41.03x, which indicates that the shares appear expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Costco Wholesale Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in, giving you a simple story driven way to link your view of Costco Wholesale’s business to a forecast and then to a fair value that you can compare directly with today’s share price.

A Narrative on Simply Wall St is your structured story about a stock. You set assumptions for future revenue, earnings and margins, and the platform converts that story into a financial forecast and a fair value estimate.

Narratives live inside the Community page and are used by millions of investors on the platform. It is easy to browse different viewpoints and see how each story translates into a fair value versus the current price, which can help you decide whether the stock looks attractive, fully priced or expensive against your own assumptions.

For Costco Wholesale, one investor Narrative currently anchors on a fair value around US$489.26 per share while another is closer to US$1,528.77. Both are updated when fresh information such as earnings or news flows in, so you can see in real time how different stories about membership strength, margins or future P/E multiples lead to very different conclusions about value.

For Costco Wholesale, however, we’ll make it really easy for you with previews of two leading Costco Wholesale Narratives:

Fair value in this narrative: US$1,528.77 per share

Market price vs this fair value: about 31.4% below the narrative fair value

Revenue growth assumption: 7%

- Emphasises ultra-sticky memberships around 90% renewal, membership fees that underpin a 2% to 3% profit margin, and a low price model that is designed to appeal in inflationary periods.

- Highlights Kirkland Signature as a major profit contributor with about US$86b in sales and points to international expansion, including China, as a key growth driver.

- Flags risks around high valuation multiples, dependence on membership income for profitability and ongoing competition from e commerce, while viewing the current price in this model as roughly in line with fair value if current assumptions hold.

Fair value in this narrative: US$726.29 per share

Market price vs this fair value: about 44.4% above the narrative fair value

Revenue growth assumption: 7%

- Describes Costco as a wide moat business with strong leadership and recurring membership revenue, but argues the stock is priced for perfection at current P/E levels.

- Sees future returns as heavily influenced by potential P/E multiple compression, even with revenue growth and modest margin expansion, with scenario analysis that ranges from very low single digit to low teens annualised outcomes.

- Calls out valuation risk, possible tariff impacts on hardline categories and pressure from competitors such as Sam's Club as the key factors that could limit shareholder returns at the current price.

These two narratives sit on opposite sides of the value debate. This gives you a practical range to compare against your own assumptions on Costco Wholesale’s membership strength, margin path and future P/E.

Do you think there's more to the story for Costco Wholesale? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.