Is CrowdStrike (CRWD) Pricing Reflect Recent Cybersecurity Focus Or Point To Valuation Gap

CrowdStrike CRWD | 411.16 411.50 | +3.18% +0.08% Post |

- If you are wondering whether CrowdStrike Holdings is still worth its current price, this article will help you connect the recent share performance with what the underlying valuation actually suggests.

- The stock last closed at US$429.64, with returns of 3.9% over the past week, a 5.3% decline over the past month, a 5.3% decline year to date, and a 5.6% decline over the past year, compared with a very large 3 year return of 282.1% and a 5 year return of 96.7%.

- Recent news around CrowdStrike has focused on its role within cybersecurity and its positioning among high growth software names. This often attracts attention when market sentiment shifts. Coverage has also highlighted how security spending trends and enterprise demand can influence investor expectations for companies like CrowdStrike, even when the broader software sector is mixed.

- On Simply Wall St's valuation checks, CrowdStrike scores 3 out of 6 for being assessed as undervalued, giving it a valuation score of 3. Next we will look at how different valuation methods line up on this stock before finishing with a framework that can help you think about value in an even more complete way.

Approach 1: CrowdStrike Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth today by projecting its future cash flows and discounting them back to the present.

For CrowdStrike Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $. The latest twelve month free cash flow is about $1.1b. Analyst estimates are available for several years, and Simply Wall St then extends these further, with projected free cash flow of about $6.5b in 2031 under this scenario.

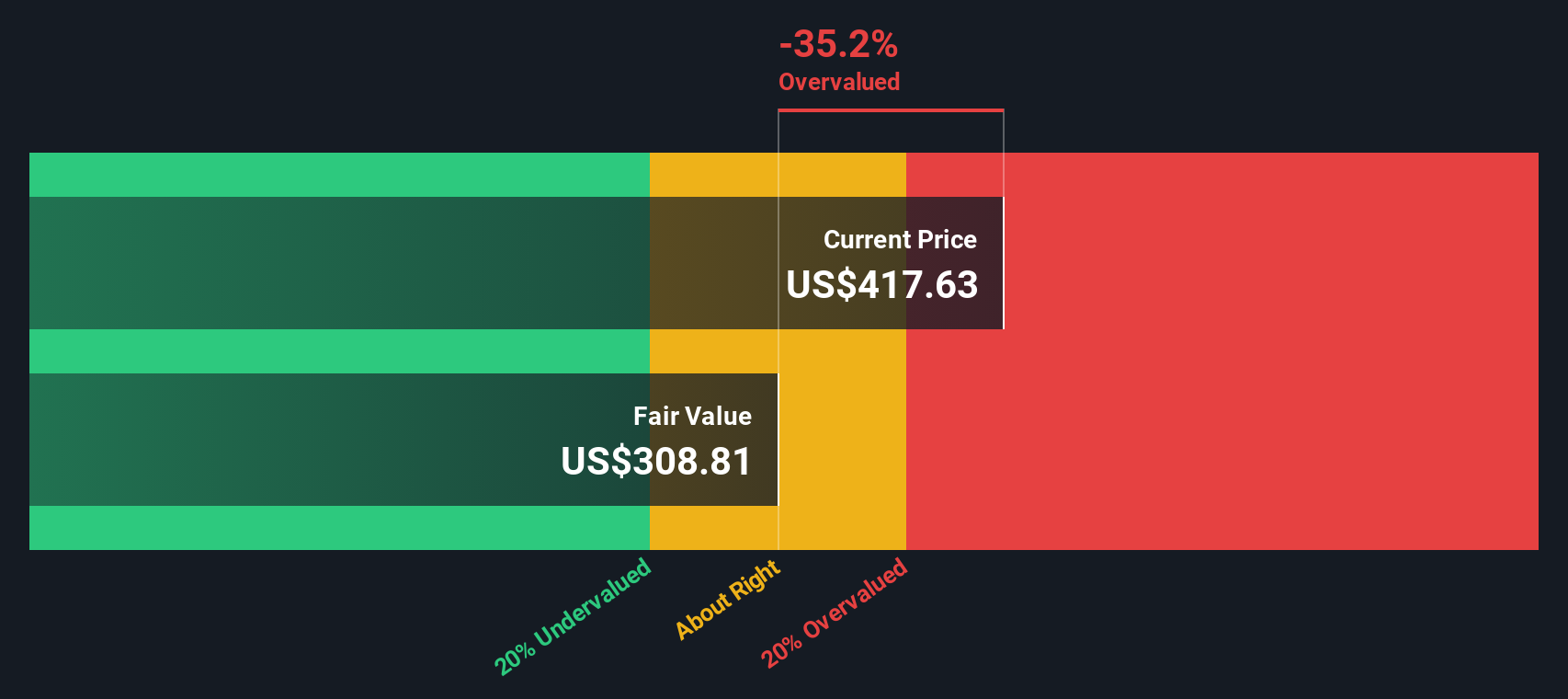

Bringing all those projected cash flows back to today gives an estimated intrinsic value of about US$540.22 per share. Compared with the recent share price of US$429.64, this implies the stock is 20.5% undervalued according to this model.

This DCF output suggests the current price leaves a valuation gap, but it is still only one lens on CrowdStrike’s potential worth.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CrowdStrike Holdings is undervalued by 20.5%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

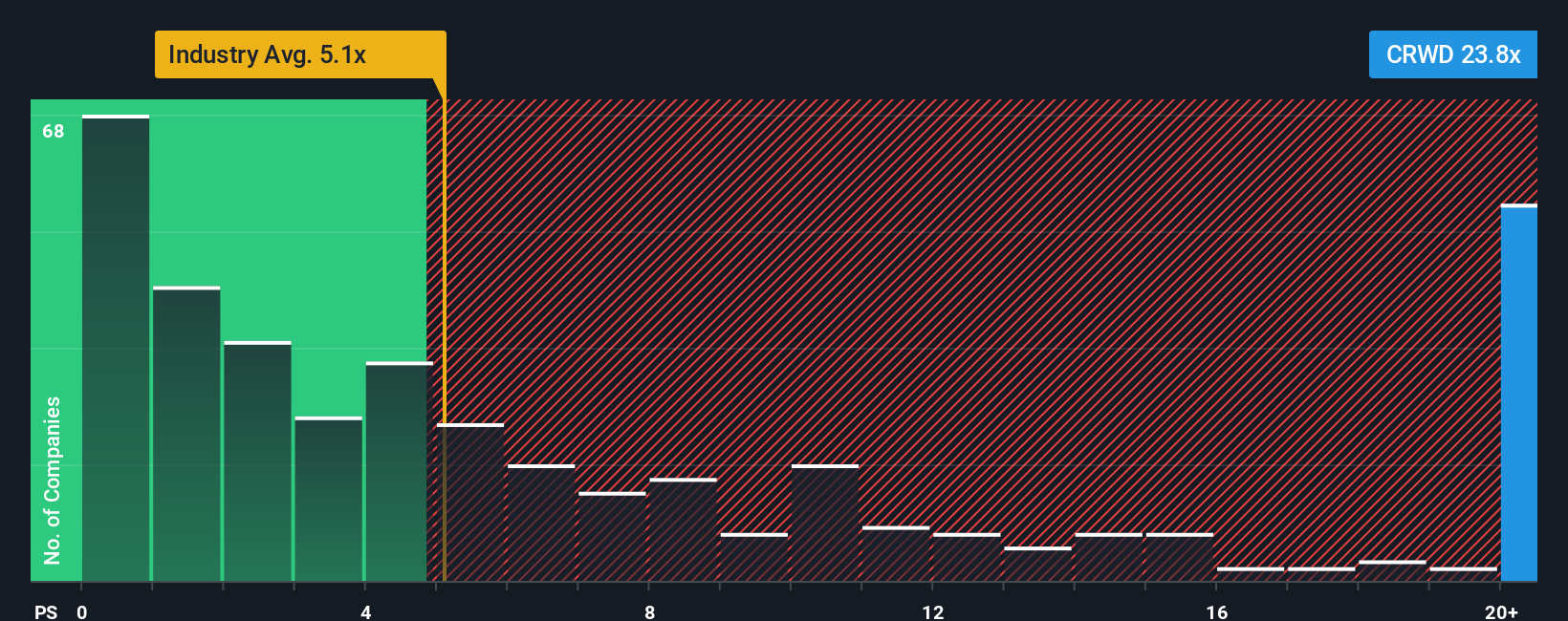

Approach 2: CrowdStrike Holdings Price vs Sales

For companies where earnings are limited or volatile but revenue is meaningful, the P/S ratio is often a useful way to think about valuation, because it compares what investors pay for each dollar of sales rather than each dollar of profit.

What counts as a “normal” or “fair” trading multiple tends to reflect what investors expect for future growth and how much risk they see. Higher expected growth or lower perceived risk can support a higher ratio, while slower growth or higher uncertainty usually points to a lower one.

CrowdStrike currently trades on a P/S of 23.73x. That is above the Software industry average P/S of 3.64x and also above the peer group average of 9.99x. Simply Wall St’s Fair Ratio for CrowdStrike is 13.71x, which is its proprietary estimate of what a reasonable P/S might be after considering factors such as the company’s growth profile, profit margins, industry, market value and key risks.

Compared with simple peer or industry comparisons, the Fair Ratio aims to be more tailored to the company itself, rather than relying on broad group averages that may mix very different business models.

On this basis, CrowdStrike’s current P/S of 23.73x sits above the Fair Ratio of 13.71x.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your CrowdStrike Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives on the Community page, where you tell your story about CrowdStrike by linking your assumptions for future revenue, earnings and margins to a forecast and fair value. You can then compare that fair value with the current price to help you decide if and when to act. The platform automatically refreshes your Narrative as new news or earnings arrive, and you can see how different investors reach very different views on the same stock. For example, one Narrative values CrowdStrike at about US$324.30 based on a certain growth, margin and future P/E profile, while another values it at about US$692.37 using stronger growth and profitability assumptions.

For CrowdStrike Holdings, however, we will make it really easy for you with previews of two leading CrowdStrike Holdings Narratives:

Fair value in this bull case: US$533.26 per share

Implied valuation gap vs last close: about 19.4% undervalued, based on that fair value and the recent price of US$429.64

Forecast annual revenue growth used in this Narrative: 21.55%

- Focuses on Falcon Flex, AI tools like Charlotte and a broader product suite that aim to deepen customer relationships and support higher margins over time.

- Leans on analysts' assumptions for strong revenue growth, a shift from losses to profits and a high future P/E multiple to support the fair value estimate.

- Flags risks around execution, reliance on newer products and acquisitions, and the impact of competition and non GAAP adjustments on how profitability is viewed.

Fair value in this bear case: US$324.30 per share

Implied valuation gap vs last close: about 32.5% overvalued, based on that fair value and the recent price of US$429.64

Forecast annual revenue growth used in this Narrative: 25.01%

- Assumes strong revenue growth and healthy margins for CrowdStrike, but concludes that the valuation multiples already price in a lot of that optimism.

- Highlights business, regulatory and competitive risks, including possible market saturation, larger technology players and emerging startups.

- Points out that the current and future P/E multiples used in the Narrative are very high, which can leave less room for disappointment if growth or profitability fall short.

Seen together, these Narratives show how two investors can work from different assumptions about fair value, risk and required P/E multiples, even while looking at the same company and many of the same facts. Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for CrowdStrike Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.