Is CVR Energy (CVI) Pricing Reflect Its DCF Upside After Recent Share Price Weakness

CVR Energy, Inc. CVI | 32.86 | +3.86% |

- If you are wondering whether CVR Energy's current share price really lines up with its underlying worth, you are in the right place because this article focuses squarely on what the numbers say about value.

- The stock closed at US$23.17, with a 7 day return of 4.3% decline, a 30 day return of 0.6% decline, a year to date return of 8.0% decline, a 1 year return of 25.3%, a 3 year return of 12.8% decline and a 5 year return of 95.6%.

- Recent price moves sit against a backdrop of ongoing interest in the energy sector and periodic shifts in investor sentiment around refiners and related businesses. For CVR Energy, news coverage has tended to focus on how the company fits into broader energy market themes rather than on one single event driving the share price.

- On our checklist of 6 valuation tests, CVR Energy scores 4 out of 6, and you can see the detailed breakdown in our valuation score. Next we will look at how different valuation methods line up on this stock and then finish with a broader way to think about value that goes beyond the usual ratios.

Approach 1: CVR Energy Discounted Cash Flow (DCF) Analysis

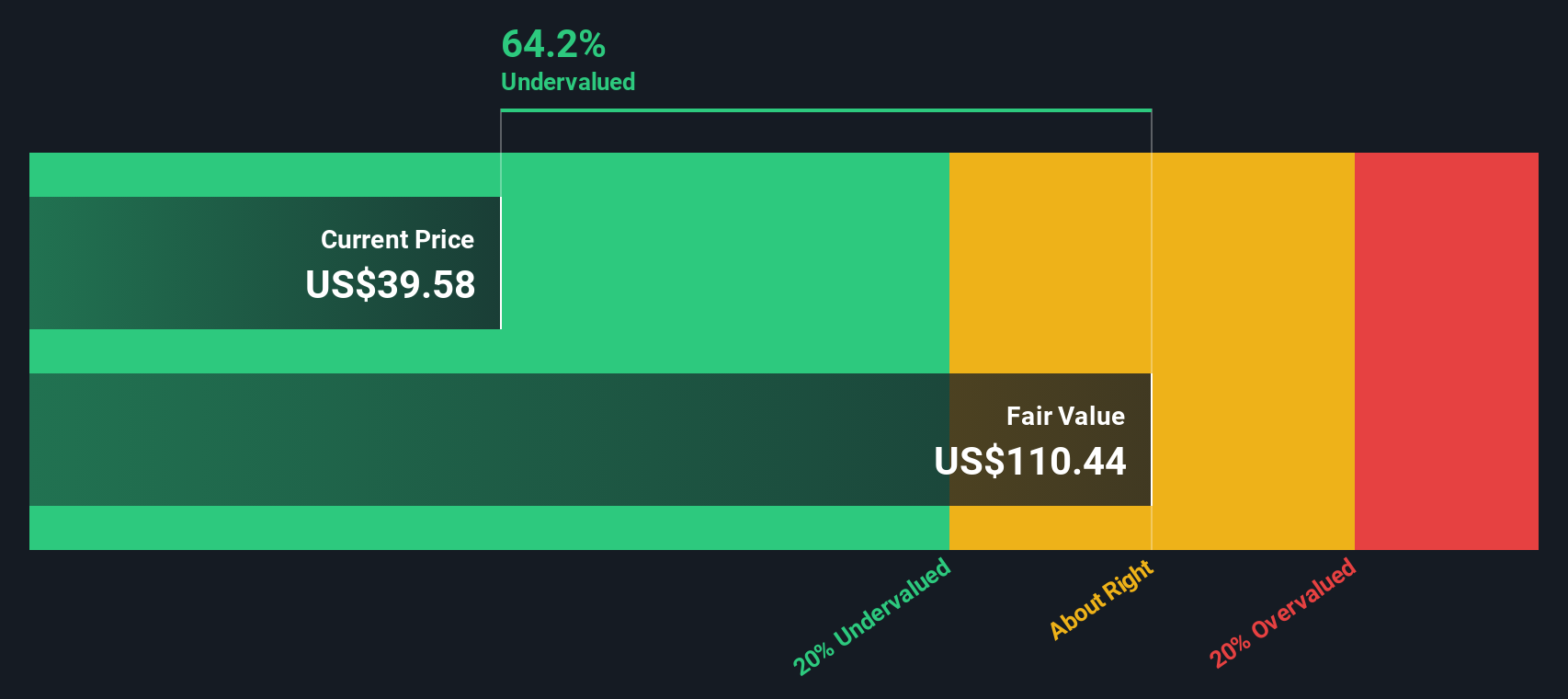

A Discounted Cash Flow, or DCF, model estimates what a company could be worth today by projecting future cash flows and discounting them back to the present using a required return.

For CVR Energy, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of about $14.6 million, so the valuation leans heavily on future estimates. Analyst inputs and extrapolated figures point to free cash flow moving to $322 million in 2026 and $360 million in 2027. Simply Wall St extends that path out to $543.4 million by 2035 using gradually moderating growth assumptions.

When all those projected cash flows are discounted back to today, the DCF model arrives at an estimated intrinsic value of about $95.92 per share, compared with a recent share price of $23.17. That implies the stock is 75.8% undervalued on this set of cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CVR Energy is undervalued by 75.8%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

Approach 2: CVR Energy Price vs Earnings

For a company that is generating profits, the P/E ratio is often a straightforward way to think about what you are paying for each dollar of earnings. Investors usually accept a higher or lower P/E depending on what they expect for future earnings growth and how risky they think those earnings are.

CVR Energy currently trades on a P/E of 14.0x. That sits close to the Oil and Gas industry average P/E of about 14.5x and below the broader peer group average of 21.6x, so on simple comparisons the shares do not look stretched relative to similar businesses.

Simply Wall St also calculates a Fair Ratio for CVR Energy of 12.9x. This is a proprietary estimate of what the P/E might be, given the company’s earnings growth profile, its industry, profit margins, market value and specific risks. Because it directly reflects these company level drivers, the Fair Ratio can be more tailored than a straight peer or industry comparison, which treats all businesses in the group as if they were the same.

With an actual P/E of 14.0x versus a Fair Ratio of 12.9x, the shares screen as slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your CVR Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply your story about CVR Energy linked directly to a financial forecast and a fair value. On Simply Wall St's Community page you can see how investors plug in their own assumptions for future revenue, earnings and margins, then compare the fair value those inputs produce with the current share price. This can help them decide whether they see CVR Energy as closer to, for example, the higher US$35.00 fair value or the lower US$19.00 fair value. Because these Narratives update automatically when new news, earnings guidance or analyst targets are added, you get an easy, continuously refreshed way to see how your view on the company stacks up against others and whether the price still matches your story.

For CVR Energy however we will make it really easy for you with previews of two leading CVR Energy Narratives:

Fair value in this bullish narrative: US$35.00 per share

Implied pricing gap vs last close: around 34% below this fair value

Revenue growth assumption: 96%

- Expects cost discipline, uninterrupted operations and a better product mix to support margins across refining and fertilizer.

- Sees potential benefits from M&A and asset diversification, with analysts in this camp using higher future P/E multiples in their models.

- Builds in analyst assumptions for revenue, margins and earnings out to 2028, then discounts those cash flows at 7.43% to reach a fair value of US$35.00.

Fair value in this bearish narrative: US$19.00 per share

Implied pricing gap vs last close: around 22% above this fair value

Revenue growth assumption: 207%

- Highlights risks from energy transition policies, older refining assets and regulatory costs that could weigh on long term earnings stability.

- Points to limited diversification and exposure to environmental and policy risks as potential headwinds for access to capital and future profitability.

- Assumes more modest revenue growth and margins, applies an 18.24x future P/E and a 7.77% discount rate, leading to a fair value of US$19.00.

If you want to see how these stories are built in full, including the detailed earnings paths and risk sections, you can step through both narratives side by side and decide which set of assumptions feels closer to your own view.

Do you think there's more to the story for CVR Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.