Is Del Monte (DMC) Undervalued Following Its New Treatt Extracts Launch?

Del Monte Corporation DMC | 0.00 |

Product launch puts Del Monte’s ingredient business in focus

Del Monte (DMC) has drawn fresh attention after partnering with Treatt on a new line of fruit-derived beverage extracts that use upcycled pineapple, watermelon, mango and cantaloupe materials from its existing processing operations.

Despite the new ingredient launch and an upcoming second quarter 2026 earnings release, Del Monte’s recent momentum has been soft. The share price is down 31.6% over 90 days and the 1 year total shareholder return has declined 12.84%, although the 3 year total shareholder return is 19.68%.

If this kind of product story has you thinking more broadly about where growth could come from next, it may be worth checking a curated list of 18 top founder-led companies

Given Del Monte’s share price slide alongside double digit recent revenue and net income growth, is the stock now reflecting concerns about the core business, or simply a sharp swing in sentiment that leaves the current valuation looking stretched?

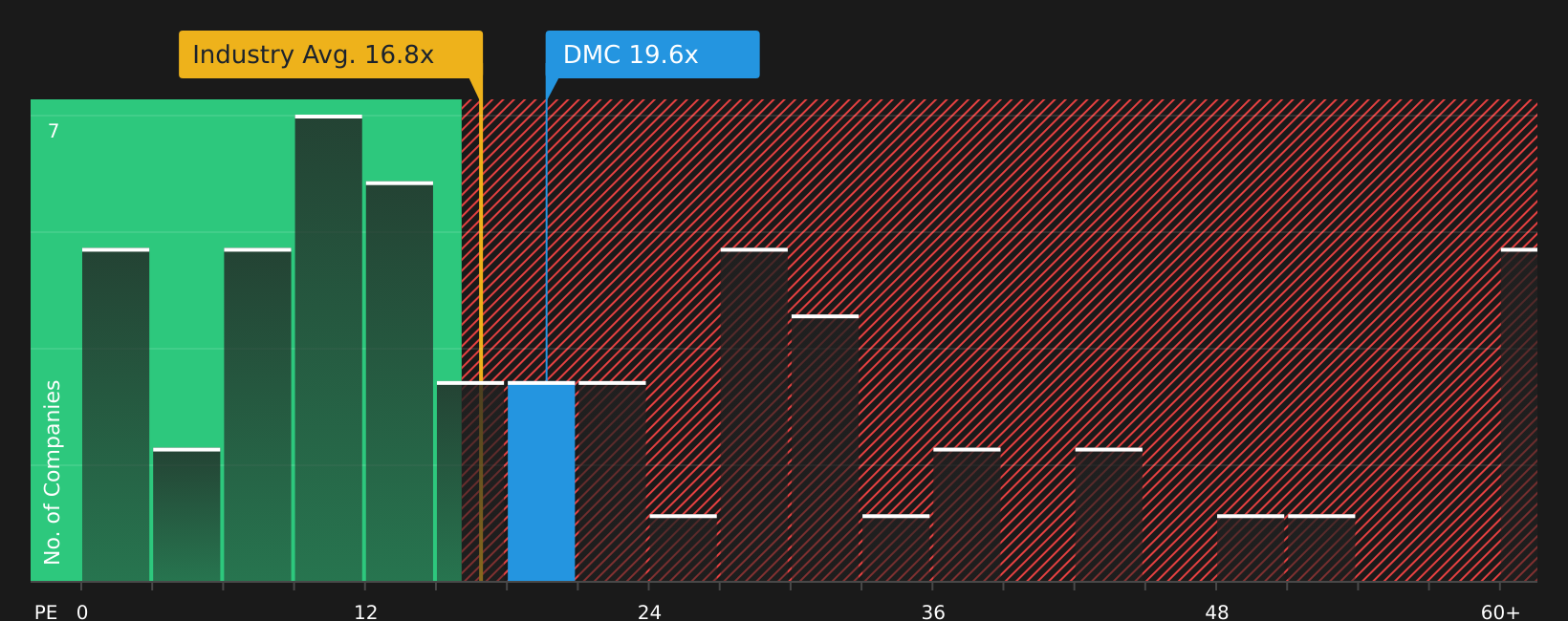

Most Popular Narrative: 46.2% Undervalued

The most widely followed narrative currently places Del Monte’s fair value at $52 per share, well above the last close of $27.99. This puts the recent share price weakness into a very different context.

Strong recent pricing and ongoing global consumer demand for pineapples (especially premium and proprietary varieties) have supported robust sales and margin expansion. However, the current industry-wide supply shortage, driven by weather disruptions and crop disease, could be interpreted by investors as a sustainable tailwind. This may lead to overestimation of future revenue growth and net margin resilience once supply gradually normalizes.

Want to see what is behind that $52 figure for Del Monte? The narrative rests on a specific path for sales growth, margin rebuild and future earnings multiples that might surprise you.

Result: Fair Value of $52 (UNDERVALUED)

However, there are still meaningful risks around Del Monte, including climate and supply chain disruption as well as sustained cost inflation, that could challenge the current undervalued narrative.

Another view on Del Monte’s valuation

The analyst narrative frames Del Monte as undervalued at $27.99 versus a $52 fair value, but a simple P/E check paints a cooler picture. DMC trades on 19.1x earnings compared with 16.9x for the US Food industry, though below its estimated fair ratio of 38.4x. Is the market being cautious or just early?

To see how this pricing gap looks when you line Del Monte up against peers and the fair ratio the market could move toward, take a closer look at the valuation breakdown, including the latest multiple workup, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of opportunity and concern around Del Monte leaves you uncertain, review the numbers yourself, pressure test the assumptions and weigh the 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond Del Monte?

If Del Monte has prompted you to think more broadly about your portfolio, now is a good time to scan for other stocks that could suit your goals.

- Spot potential bargains early by reviewing companies that stand out in our value filters using the 44 high quality undervalued stocks.

- Strengthen the defensive side of your portfolio by focusing on companies highlighted in the 79 resilient stocks with low risk scores.

- Get ahead of the crowd by checking companies surfaced in the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.