Is DICK'S Sporting Goods (DKS) Pricing Look Reasonable After Mixed Long Term Returns

Dick's Sporting Goods, Inc. DKS | 191.75 | -0.20% |

- If you are wondering whether DICK'S Sporting Goods is fairly priced at around US$204.22 a share, this article walks through what that number might and might not be telling you.

- The stock has had mixed returns, with a 1% decline over the last 7 days, a 0.7% decline over 30 days, a 2% gain year to date and a 7.1% decline over 1 year. The 3 year return sits at 66.4% and the 5 year return is very large at about 3x.

- Recent attention on DICK'S Sporting Goods has focused on how a well known US sports retailer is positioned as consumer spending patterns change and athletic and outdoor categories continue to attract interest. News coverage has also highlighted how traditional brick and mortar retailers are responding to competition from online only players and evolving customer expectations.

- Right now, DICK'S Sporting Goods has a valuation score of 3 out of 6 checks. Next we will look at what that score means across different valuation methods and then finish with a way to think about value that goes beyond any single model.

Approach 1: DICK'S Sporting Goods Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts those projections back to today’s value to estimate what the business might be worth per share.

For DICK'S Sporting Goods, the model starts with last twelve months free cash flow of about $293.0 million. Analysts provide explicit forecasts for the next few years, and Simply Wall St extends those into a 10 year path, with projected free cash flow of $472.5 million in 2035. Each of these future cash flows is discounted back to today using a required return, which is how you arrive at an estimated value per share.

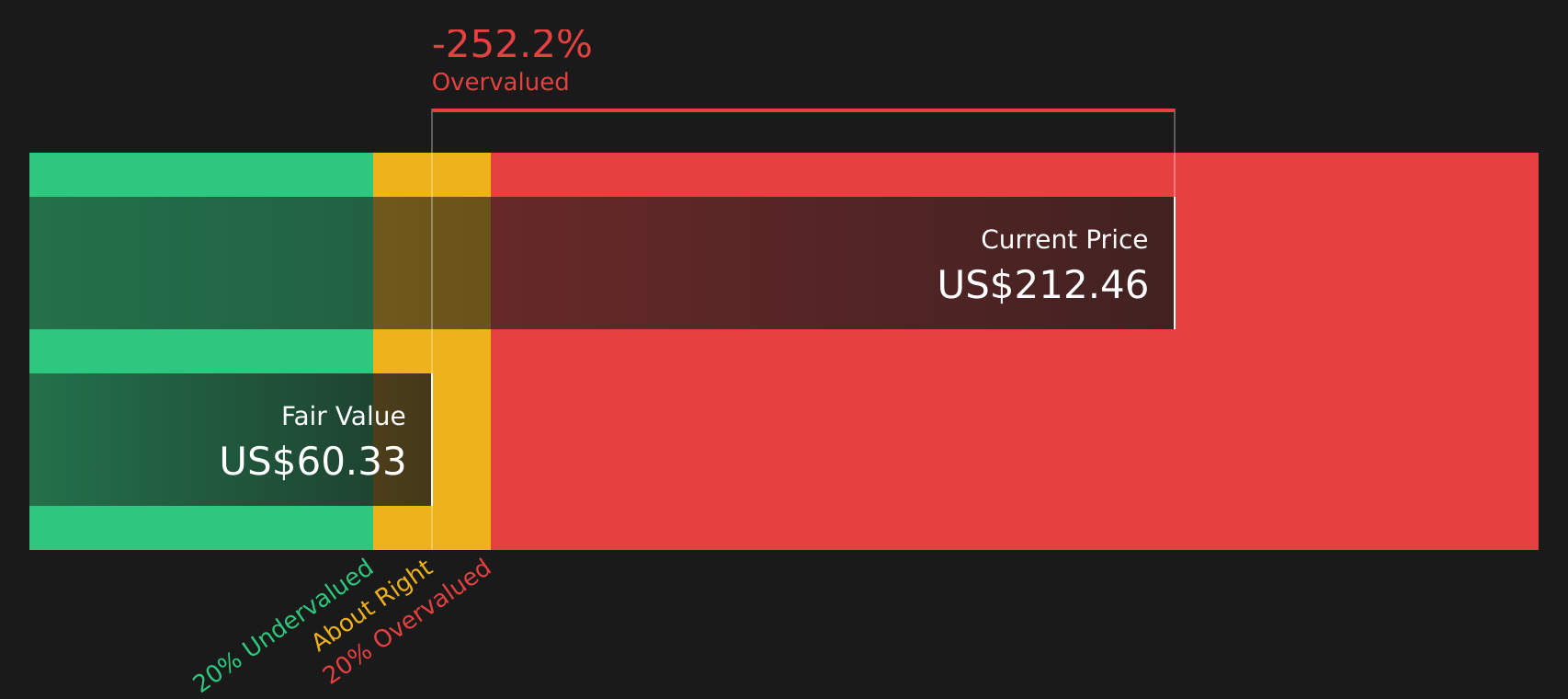

On this 2 Stage Free Cash Flow to Equity model, the intrinsic value comes out at about $73.37 per share. Against a current share price around $204.22, the DCF implies the stock is 178.3% overvalued based on these assumptions and projections.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DICK'S Sporting Goods may be overvalued by 178.3%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: DICK'S Sporting Goods Price vs Earnings

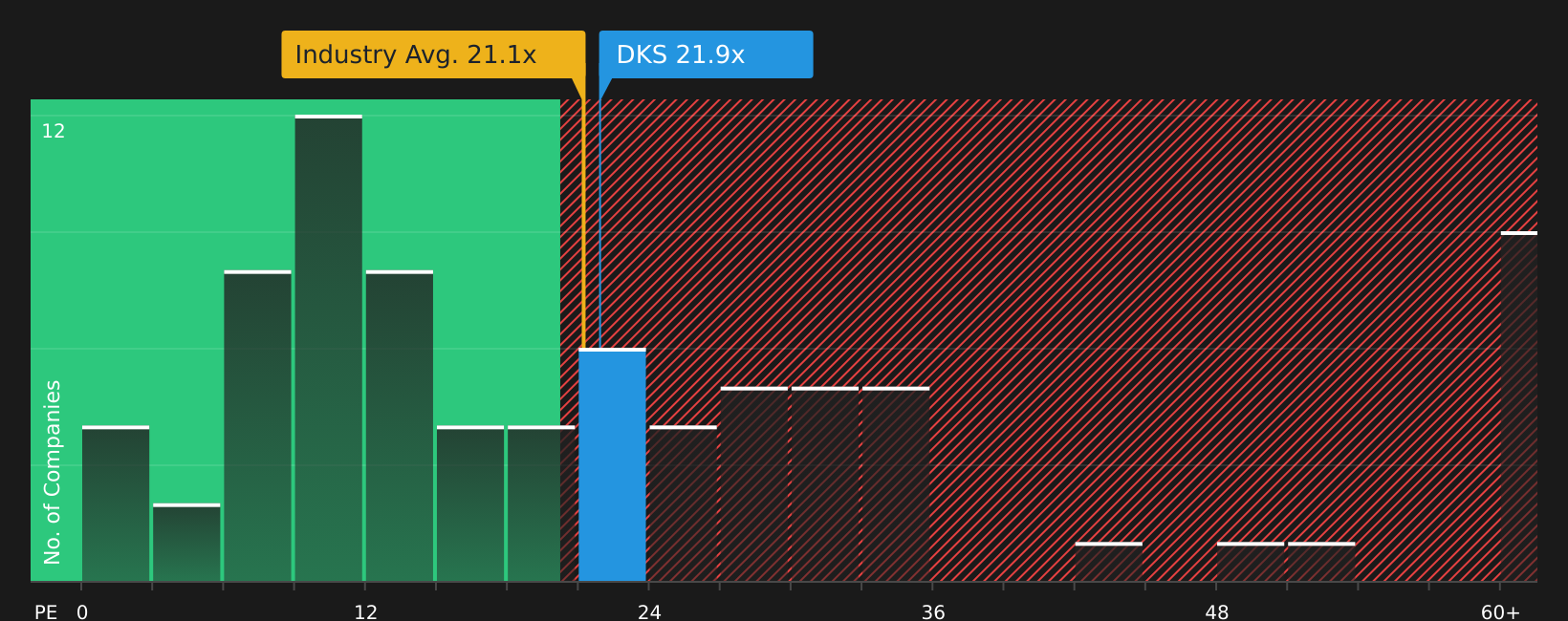

For a profitable company like DICK'S Sporting Goods, the P/E ratio is a straightforward way to link what you pay for each share to the earnings that support it. It helps you see how much the market is willing to pay for every dollar of current earnings.

What counts as a “normal” P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to align with a lower multiple.

DICK'S Sporting Goods currently trades at a P/E of 18.0x. That is below the Specialty Retail industry average of about 20.1x and well below the peer group average of 36.4x. Simply Wall St also calculates a Fair Ratio of 20.8x, which is the P/E it would expect given factors such as earnings growth, margins, industry, market cap and risk profile. This Fair Ratio can be more tailored than a simple peer or industry comparison because it accounts for company specific fundamentals rather than treating all retailers the same.

Comparing the current P/E of 18.0x with the Fair Ratio of 20.8x suggests the shares trade below that model based reference point.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your DICK'S Sporting Goods Narrative

Earlier we mentioned that there is an even better way to understand value, so let us introduce you to Narratives. These let you write a simple story about DICK'S Sporting Goods, connect that story to numbers like your assumed fair value and expectations for future revenue, earnings and margins, and then see how that translates into a fair value that you can compare to today’s price.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors. Each Narrative ties a company’s story to a forecast and then to a fair value, and the platform keeps those Narratives updated as new information such as earnings or news is added.

For DICK'S Sporting Goods, one investor might lean toward the higher fair value cases around US$273 to US$285 if they think omni channel investments, GameChanger and DICK'S Media Network will support stronger earnings over time. Another might sit closer to the lower end around US$155 to US$198.6 if they are more cautious about store expansion, capital spending and footwear growth assumptions.

For DICK'S Sporting Goods, here are previews of two leading DICK'S Sporting Goods Narratives that make the comparison straightforward:

Fair value in this bullish narrative: US$285.00 per share

Implied undervaluation versus the recent price of about US$204.22: roughly 28%

Revenue growth assumption: 16.79% a year

- Expects health and sports trends, plus experiential formats like House of Sport and Field House, to support higher sales and margins.

- Builds in growing contribution from GameChanger and DICK'S Media Network to lift profitability over time.

- Assumes DICK'S uses its scale, vendor relationships, and inventory management to grow earnings enough to justify a higher P/E multiple.

Fair value in this bearish narrative: US$198.60 per share

Implied overvaluation versus the recent price of about US$204.22: roughly 3%

Revenue growth assumption: 3.05% a year

- Focuses on the risk that heavy spend on House of Sport expansion, marketing and inventory does not translate into matching revenue.

- Assumes margins soften slightly while earnings stay around current levels, which limits upside from here.

- Builds in a lower earnings growth path and only a modestly higher future P/E, which pulls the fair value closer to today’s price.

One Narrative sees DICK'S Sporting Goods as having meaningful potential upside if experiential stores, media and digital platforms continue to build earnings power. The other sees only limited upside if spending, margin pressure and more modest growth have a larger impact. If you want to see how other investors are framing the trade-off between these two paths, Curious how numbers become stories that shape markets? Explore Community Narratives and compare their stories with your own expectations about the business.

Do you think there's more to the story for DICK'S Sporting Goods? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.