Is DoorDash (DASH) Quietly Redefining Its Profit Engine With Ads Despite Recent App Outages?

DoorDash DASH | 0.00 |

- In recent weeks, DoorDash has expanded its DoorDash Ads platform with new formats, offsite reach, automation tools, and data partnerships, while also facing temporary app outages that disrupted access for many users.

- The advertising upgrades, including immersive Spotlight placements and Symbiosys-powered offsite campaigns, highlight DoorDash’s push to monetize its first-party data and merchant relationships beyond core delivery.

- We’ll now examine how DoorDash’s expanded advertising toolkit and data partnerships may reshape its investment narrative and long-term profit mix.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

DoorDash Investment Narrative Recap

To own DoorDash today, you need to believe it can evolve from food delivery into a broader local commerce and advertising platform while managing rising complexity and costs. The near term catalyst is execution on higher margin ads and subscriptions, and the recent Ads expansion supports that story. By contrast, the biggest risk remains operational and regulatory pressure on fulfillment costs, which the temporary outages highlight but do not appear to materially change on their own.

The June launch of DoorDash’s expanded Ads suite, including Spotlight formats and Symbiosys powered offsite campaigns, is most relevant here because it directly targets higher margin, data driven revenue. Early tests citing stronger click through rates and “new to brand” reach speak to the potential for advertising to grow as a share of profits, which could help offset future pressure from labor, incentives, and expansion spending if DoorDash executes consistently.

Yet behind the headlines, investors should also be aware that growing reliance on gig labor and regulatory scrutiny could...

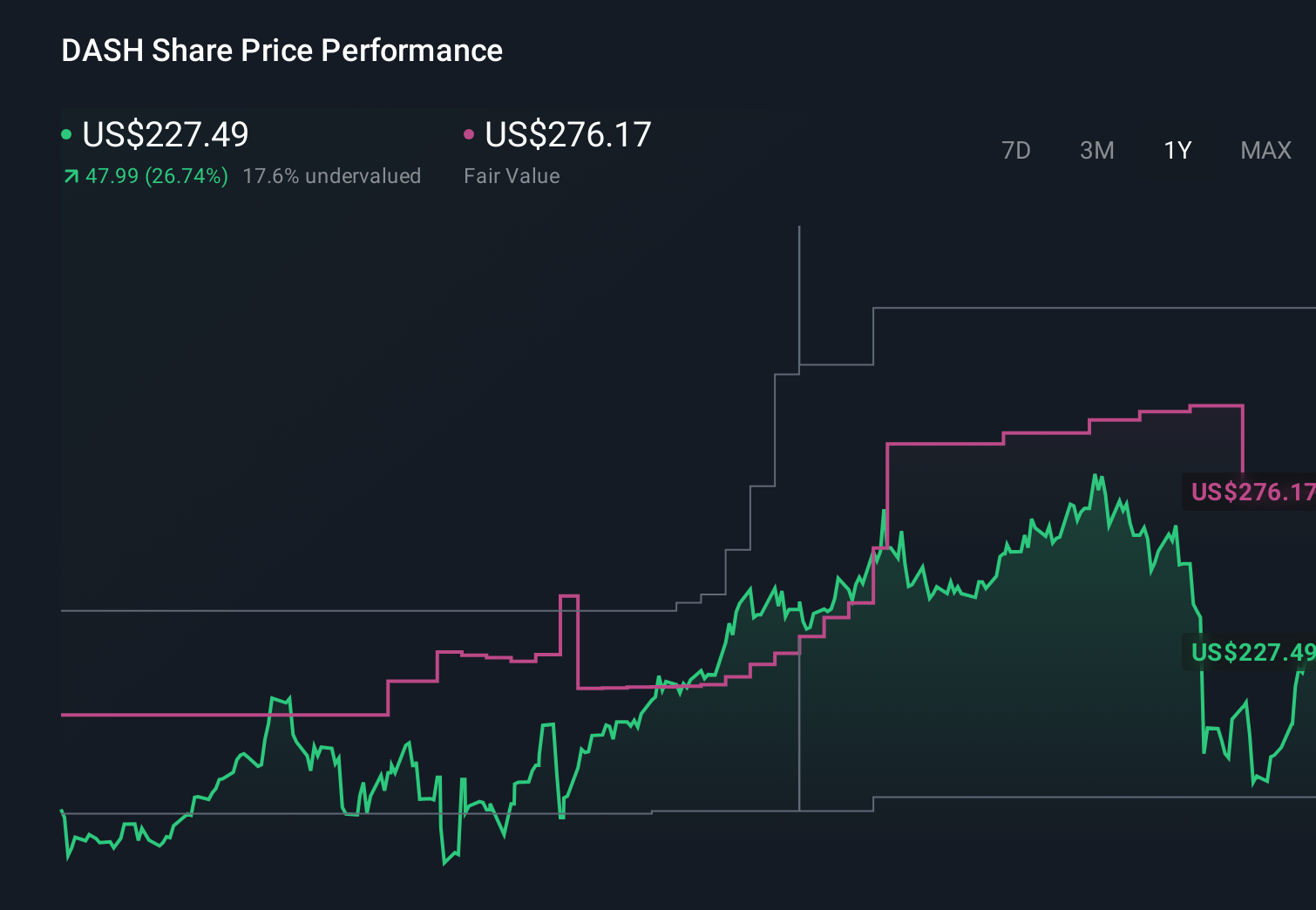

DoorDash's narrative projects $26.2 billion revenue and $3.3 billion earnings by 2029. This requires 21.2% yearly revenue growth and approximately a $2.4 billion earnings increase from $926.0 million today.

Uncover how DoorDash's forecasts yield a $245.99 fair value, a 45% upside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the most cautious analysts saw a tougher path, even before this Ads update, despite still projecting revenue of about US$23.7 billion and earnings of roughly US$2.3 billion by 2029; their concerns about higher labor costs and tighter margins may look different in light of DoorDash’s push into higher margin advertising, and it is worth weighing that more pessimistic story alongside more optimistic takes.

Explore 9 other fair value estimates on DoorDash - why the stock might be worth just $226.02!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 32 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.