Is DoorDash (DASH) Using Auto Parts Delivery to Quietly Redefine Its Logistics Moat?

DoorDash DASH | 0.00 |

- Recently, AutoParts.com Inc. announced that its catalog of hundreds of thousands of auto parts went live on the DoorDash Marketplace, using geo-located inventory and a nationwide retailer network to support rapid, last‑mile delivery, alongside a limited‑time 20% discount for new DoorDash AutoParts.com customers on qualifying orders.

- This move extends DoorDash’s platform beyond food and everyday essentials into time‑sensitive auto parts delivery, highlighting how its logistics infrastructure can be applied to more complex, higher‑value categories.

- Next, we’ll examine how adding rapid, last‑mile auto parts delivery through AutoParts.com may influence DoorDash’s broader investment narrative.

Find 44 companies with promising cash flow potential yet trading below their fair value.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe its logistics platform can keep widening beyond restaurants into categories like groceries, retail, and now auto parts, while still protecting margins despite rising labor and regulatory pressures. The AutoParts.com launch reinforces the “many verticals, one logistics network” thesis but does not alter the near term focus on cost discipline and order frequency, nor does it materially change the key risk of execution strain as DoorDash layers on more complex categories.

Among recent announcements, the expanded DoorDash Ads suite is particularly relevant, because AutoParts.com and other non food partners can plug into higher margin advertising tools that aim to lift order volume and monetization per partner. Bulls watching catalysts around ad revenue, subscription depth, and automation may see this pairing of new verticals with richer ad products as an example of how DoorDash is trying to increase platform economics without relying solely on order growth.

But beneath the surface, investors should be aware that growing into more complex verticals also heightens exposure to…

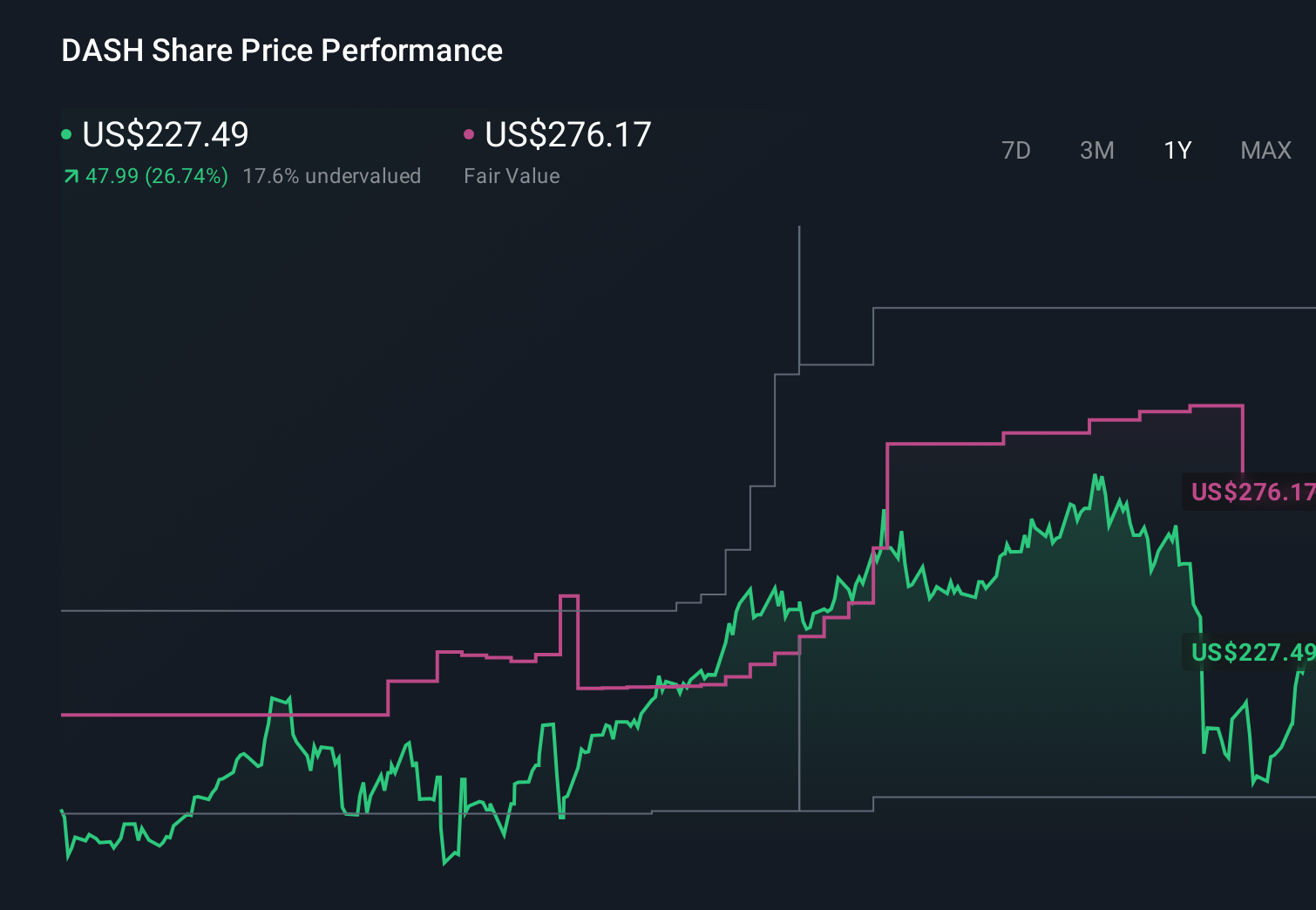

DoorDash's narrative projects $26.2 billion revenue and $3.3 billion earnings by 2029. This requires 21.2% yearly revenue growth and about a $2.4 billion earnings increase from $926.0 million today.

Uncover how DoorDash's forecasts yield a $245.99 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some analysts were far more optimistic before this news, assuming revenue could reach about US$21.9 billion and earnings US$4.8 billion by 2028, which contrasts sharply with concerns that international and category expansion might strain cash flow rather than boost it, reminding you that even a single new partnership like AutoParts.com can eventually tilt these competing narratives in very different directions.

Explore 10 other fair value estimates on DoorDash - why the stock might be worth just $175.16!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.