Is DoorDash’s (DASH) Exit From Four Markets a Pivot Toward Discipline or Retreat on Global Ambition?

DoorDash DASH | 0.00 |

- In late February 2026, DoorDash announced it is exiting Qatar, Singapore, Japan, and Uzbekistan across its Deliveroo and Wolt brands after a multi‑month review, beginning an orderly wind‑down while stating these moves are not expected to materially affect its previously issued financial outlook.

- This retrenchment underlines DoorDash’s effort to concentrate resources on markets where it believes it can achieve sustainable scale and long‑term leadership, potentially reshaping how investors think about its international expansion plans and cost discipline.

- We’ll now examine how DoorDash’s exit from four countries may reshape its investment narrative around global expansion and operational focus.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

DoorDash Investment Narrative Recap

To own DoorDash, you broadly need to believe its logistics platform, subscriptions, and advertising can support durable earnings growth while it manages regulatory and cost pressures. The exit from Qatar, Singapore, Japan, and Uzbekistan looks immaterial to near term financial guidance, but it slightly reduces the risk of overextension abroad while sharpening focus on execution in core markets. The biggest near term risk still centers on fulfillment costs and gig labor regulation rather than this specific retrenchment.

The most relevant recent update alongside these exits is DoorDash’s full year 2025 earnings, where it reported US$13,717 million in sales and US$935 million in net income. Against that backdrop, pulling back from four smaller markets can be read in the context of protecting profitability and concentrating on areas that already support earnings power and upcoming catalysts such as subscription growth and higher margin services like advertising.

Yet while this renewed focus can look reassuring, investors should also be aware of the ongoing pressure from potential gig labor regulation and its impact on ...

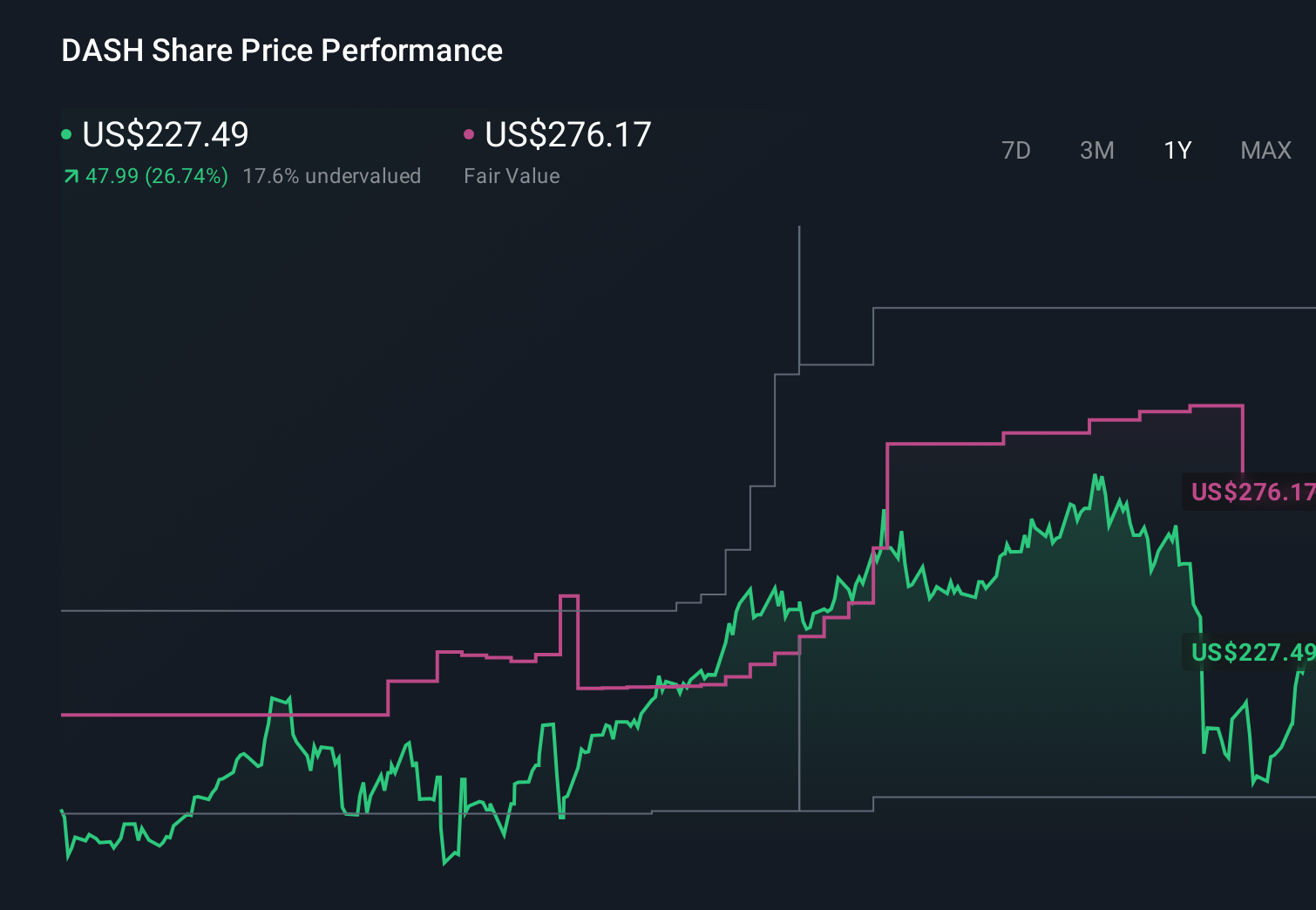

DoorDash's narrative projects $20.4 billion revenue and $3.2 billion earnings by 2028. This requires 19.6% yearly revenue growth and roughly a $2.4 billion earnings increase from $781.0 million today.

Uncover how DoorDash's forecasts yield a $274.69 fair value, a 56% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting revenue of about US$21.9 billion and earnings near US$4.8 billion by 2028, which is far more upbeat than the baseline view and could be challenged or reinforced by DoorDash’s decision to exit four countries and the broader concerns around gig labor costs.

Explore 16 other fair value estimates on DoorDash - why the stock might be worth just $189.85!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

No Opportunity In DoorDash?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.