Is Duolingo (DUOL) Fully Priced Following Earnings Jitters?

Duolingo, Inc. DUOL | 0.00 |

Duolingo (DUOL) slipped 3.01% in its latest session even as broader markets advanced, as investors focused on the upcoming August 5 earnings report, which is expected to pair revenue growth with a sharp EPS decline.

At a share price of $131.22, Duolingo has seen short term momentum build, with a 90 day share price return of 26.84%. However, this contrasts with a year to date share price decline of 25.65% and a 1 year total shareholder return decline of 63.69%, suggesting sentiment remains cautious ahead of earnings despite routine director RSU grants.

If Duolingo’s setup has you reassessing where growth and risk feel acceptable, it could be a useful moment to scan 63 profitable AI stocks that aren't just burning cash for other AI focused stocks with established profitability.

Duolingo’s business still looks strong on user engagement and revenue, yet the stock’s sharp swing over the past year raises a different issue: is that quality already more than reflected in today’s $131.22 price or not?

Most Popular Narrative: 14.6% Overvalued

Against Duolingo’s last close at $131.22, the most followed narrative anchors on a fair value of $114.49, framing the stock as modestly ahead of that mark while still highlighting a strong business story.

Duolingo just crossed $1 billion in revenue and delivered a 367% surge in net earnings, yet the stock trades at a trailing P/E of just 11x. For a market-leading EdTech platform with 50 million daily active users, that is a number you would normally associate with a slow-moving industrial company, not one of the most recognisable consumer brands on the planet.

Curious how a high margin, cash rich platform ends up with this fair value gap? According to REmmy, the narrative leans heavily on earnings quality, future profitability and where growth settles after the current investment phase.

Result: Fair Value of $114.49 (OVERVALUED)

However, Duolingo’s Vision 2026 spend and rising AI competition could still pressure margins or user growth expectations. This could quickly challenge this overvaluation story.

Another View: Duolingo Through Our DCF Model

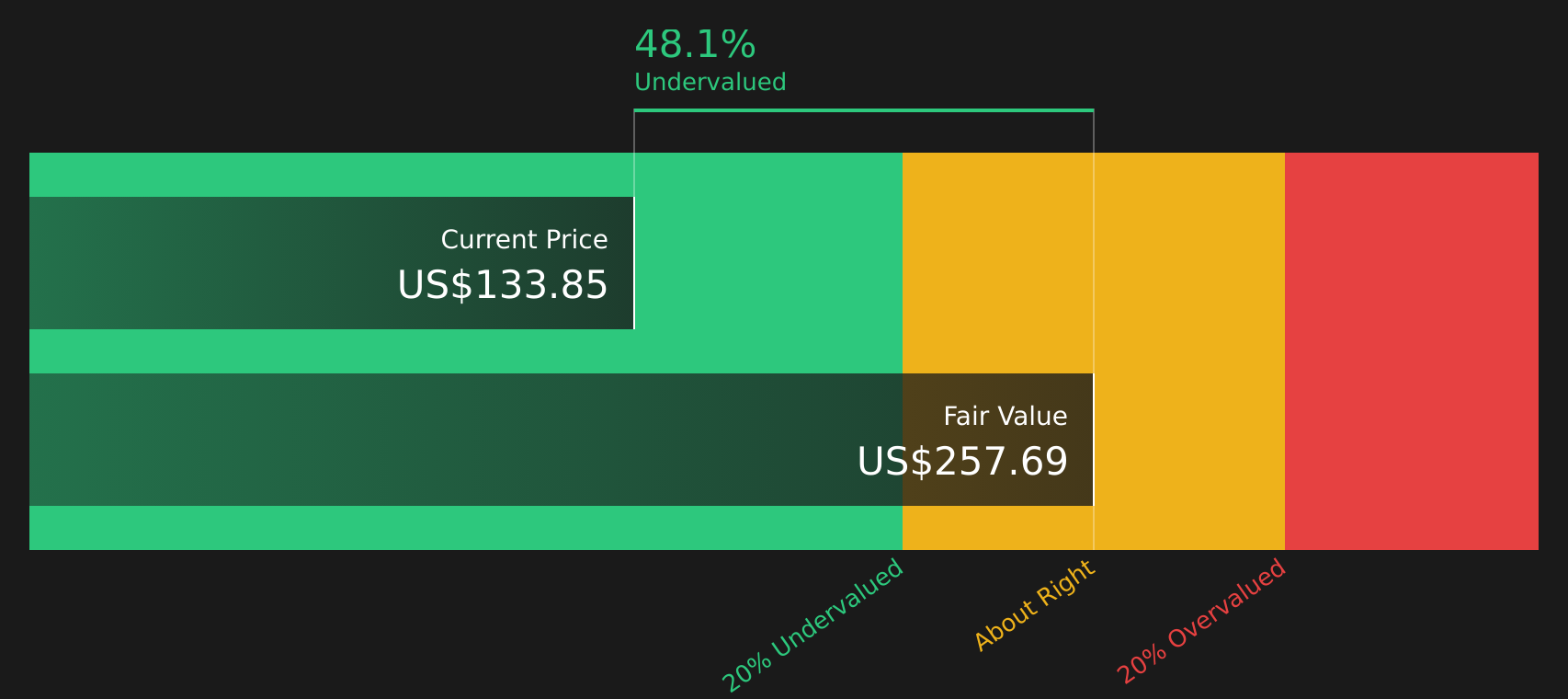

While the popular Duolingo narrative frames the stock as about 14.6% overvalued versus a fair value of $114.49, the Simply Wall St DCF model points in the opposite direction. At $131.22, Duolingo is trading about 56.2% below an estimated future cash flow value of $299.44, which raises a different question about how much pessimism is already priced in.

For readers who want to see how this cash flow view is built line by line, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Duolingo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed messages around Duolingo leave you unsure, consider acting while the data is fresh and weigh both sides carefully by reviewing 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Duolingo?

Duolingo’s mixed signals can be a useful reminder not to anchor on a single stock. Broaden your watchlist so you are not missing other potential opportunities.

- Target potential mispriced opportunities early by scanning the screener containing 20 high quality undiscovered gems before they attract wider attention.

- Strengthen your core holdings by reviewing companies in the solid balance sheet and fundamentals stocks screener (48 results) that pair financial resilience with clear fundamentals.

- Reduce portfolio stress by looking at the 78 resilient stocks with low risk scores for stocks that score well on stability and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.