Is Elevance Health a Hidden Opportunity After 24.5% Share Price Drop in 2025?

Elevance Health ELV | 300.96 | +0.82% |

- Thinking about whether Elevance Health is a bargain right now? Let’s break down what’s really driving the conversation around its value and what investors should be on the lookout for.

- The stock has seen some notable moves lately, dipping 5.4% over the last week and dropping 9.1% in the past month, with a year-to-date slide of 13.1%. Even over the past year, shares are down 24.5%, hinting at shifting sentiment or new risks on investors’ radars.

- Much of this volatility has come after news about broader healthcare sector changes, including concerns over rising costs and policy shifts that have put pressure on managed care stocks like Elevance. Industry conversations about evolving government healthcare programs have fueled uncertainty, but may also be setting up opportunities for those looking past the headlines.

- When it comes to valuation, Elevance Health stands out with a strong score of 6 out of 6 according to our key valuation checks. We’ll explore what goes into this score and how standard models stack up, but stick around as there is an even smarter way to understand value that we’ll cover by the end.

Approach 1: Elevance Health Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its expected future cash flows and then “discounting” those amounts back to today using a required rate of return. This approach attempts to determine what all those future dollars are worth in the present, providing a clear picture of a company’s intrinsic value.

For Elevance Health, the DCF model starts with the latest reported Free Cash Flow of $3.6 billion. Analysts estimate this will grow over time, reaching $6.4 billion by 2026 and $8.7 billion by 2029. Simply Wall St extrapolates those forecasts, projecting Free Cash Flow could rise as high as $12.3 billion by 2035, though estimates beyond five years should always be treated with caution. All figures are in US dollars.

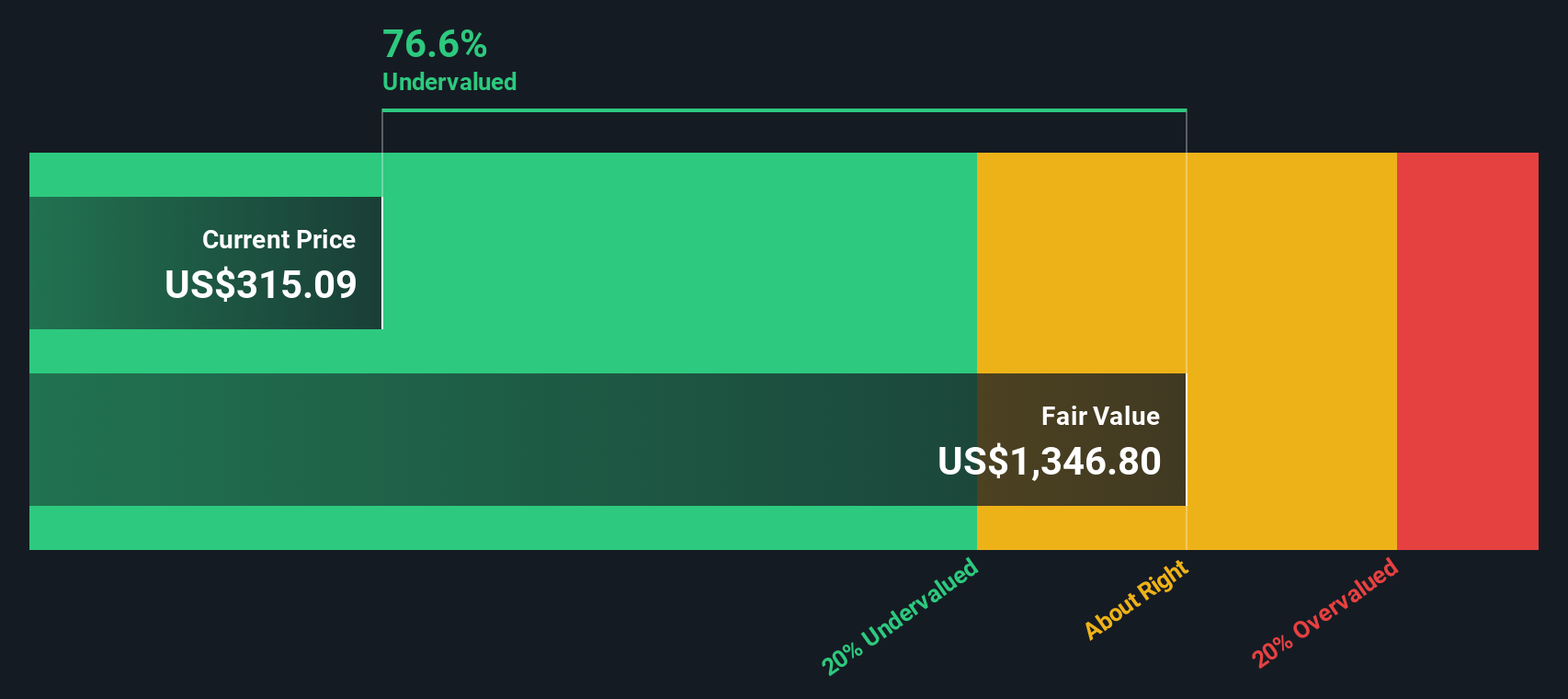

After discounting each year’s projected cash flow back to today, the DCF model arrives at an intrinsic value of $1,090.84 per share for Elevance Health. This is about 71% higher than current share prices, which signals a substantial undervaluation based on current projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Elevance Health is undervalued by 70.8%. Track this in your watchlist or portfolio, or discover 850 more undervalued stocks based on cash flows.

Approach 2: Elevance Health Price vs Earnings

For established, profitable companies like Elevance Health, the Price-to-Earnings (PE) ratio is a widely-used measure for valuing a stock. It tells investors how much the market is willing to pay today for a dollar of current earnings, making it particularly relevant when earnings are stable and predictable.

Not all PE ratios are created equal. Growth expectations and risk profiles play a big part in what is considered a “normal” PE for a company or industry. High-growth companies often trade at higher PEs, reflecting optimism about future earnings, while more uncertainty or slower growth can pull a PE ratio lower.

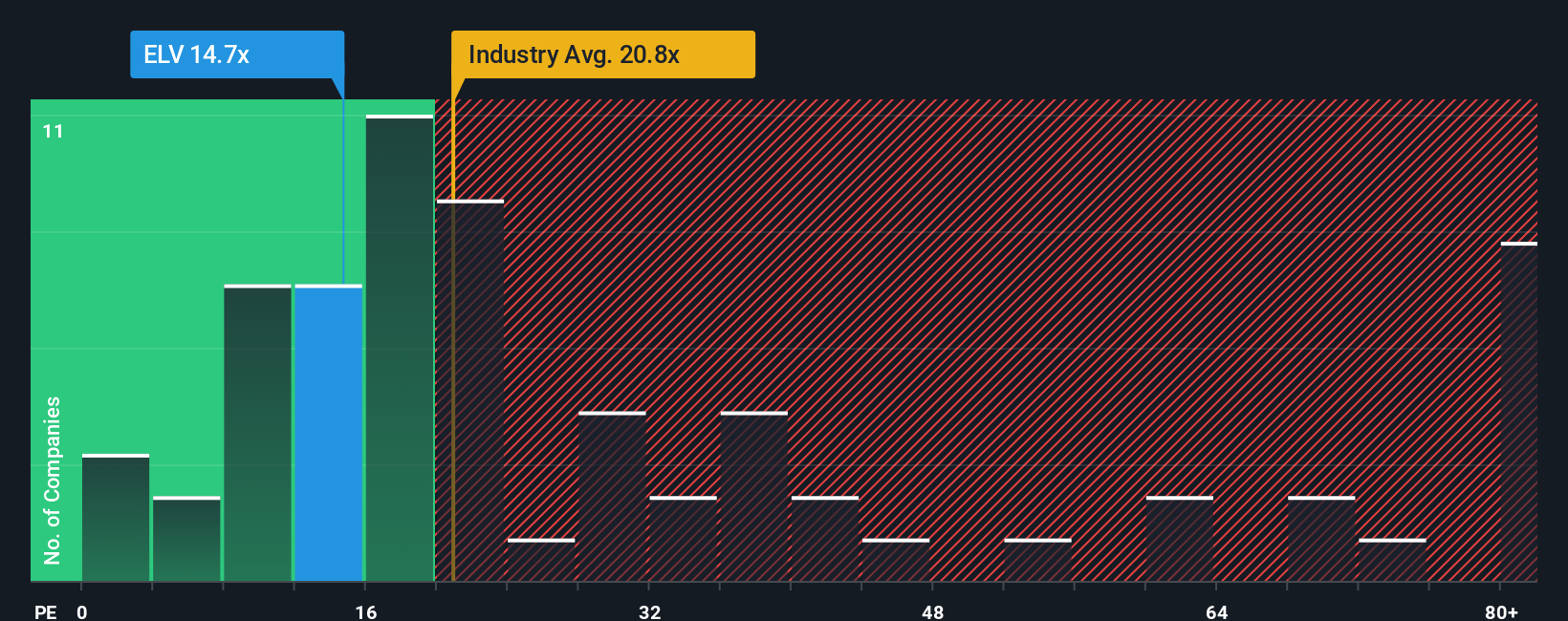

At the moment, Elevance Health is trading at a PE ratio of 12.8x. For context, the average PE across the healthcare industry is 21.5x, and Elevance’s peer group averages an even higher 25.4x. This suggests that, at first glance, Elevance may be undervalued compared to its sector and competitors.

There is more to the story than simple averages. Simply Wall St’s “Fair Ratio” combines a range of company-specific factors, such as Elevance’s earnings growth, risk profile, industry landscape, profit margins, and size, to arrive at a more tailored benchmark for value. This proprietary metric gives a clearer indication of what the market should pay, instead of relying solely on comparisons that might not account for important nuances.

For Elevance Health, the Fair Ratio stands at 32.1x. Comparing this to the current PE of 12.8x, the shares appear significantly undervalued based on these tailored expectations.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1407 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Elevance Health Narrative

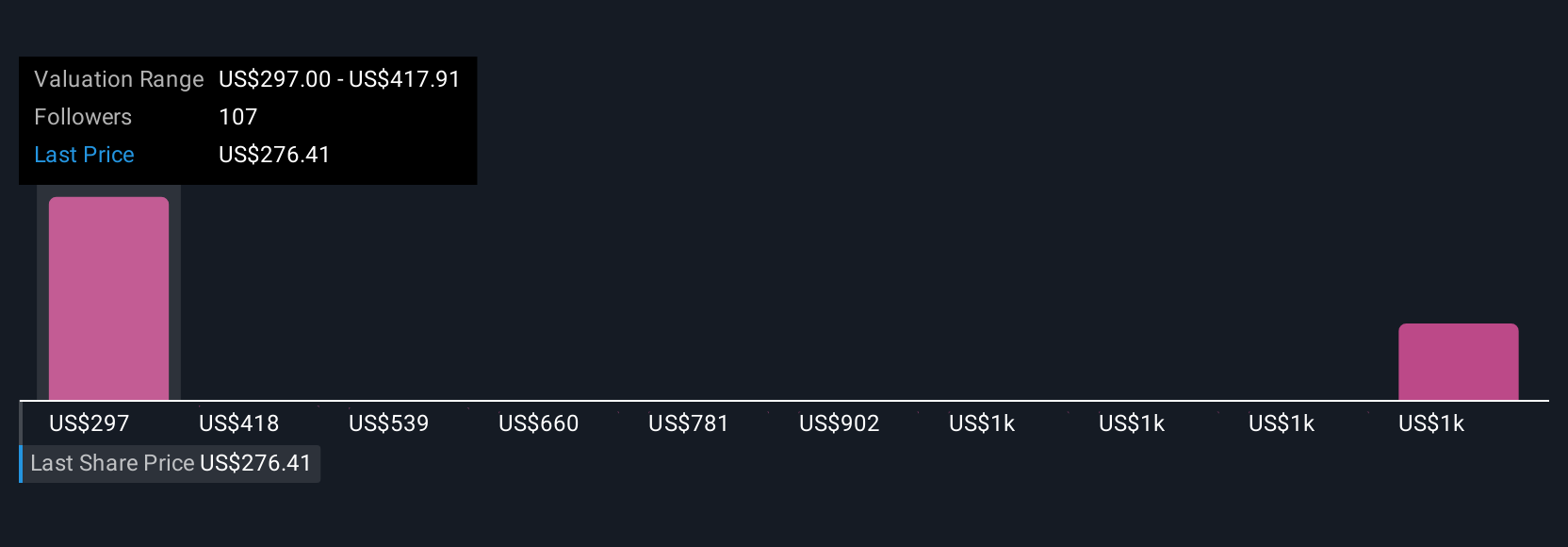

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a personal, story-driven perspective on a company, which connects your beliefs about Elevance Health’s future (such as projected revenue and earnings) to a set of financial forecasts and a fair value. Essentially, this links the company’s story to the numbers. Narratives are easy to create and share within Simply Wall St’s Community, used by millions of investors, making it simple to capture your viewpoint in one place.

With Narratives, you can compare your Fair Value with the market Price to decide whether it is time to buy or sell. Because Narratives update automatically when new data, news, or earnings come in, your view of Elevance Health can evolve as the facts change. For example, some investors might see Elevance as a value play with a fair value near $507 based on robust Medicare Advantage growth, while others see more risk and forecast a fair value closer to $297 due to persistent cost pressures and Medicaid headwinds. This shows that different stories lead to very different investment conclusions.

Do you think there's more to the story for Elevance Health? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.