Is e.l.f. Beauty a Bargain After This Year’s 40% Price Drop?

e.l.f. Beauty, Inc. ELF | 60.87 | -2.30% |

- Thinking about buying or holding e.l.f. Beauty stock? If you are wondering whether its price tag still matches its long-term promise, you are in the right place.

- The stock has pulled back sharply, dropping 40% so far this year and over 43% in just the last month. Its 5-year return still sits at an impressive 245.4%.

- Key news stories have fueled this recent volatility, with headlines focusing on increased competition in the cosmetics space and broader uncertainty around consumer spending for beauty products. While these developments have led to a cool-off after years of huge gains, they have also put a spotlight on what the company is really worth.

- Right now, e.l.f. Beauty scores a 3 out of 6 on our valuation checks. This suggests the market may be rethinking the company’s future growth. Next, we will break down the most common valuation approaches, and there is an even smarter way to connect these dots, which we will get to at the end.

Approach 1: e.l.f. Beauty Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a company is worth by projecting its future cash flows and then discounting them back to today’s dollars. This approach seeks to answer one essential question: what is the present value of all the future cash that e.l.f. Beauty will generate?

For e.l.f. Beauty, the latest reported Free Cash Flow stands at $154.7 million. Looking ahead, analyst projections and model estimates see this figure climbing to $1.01 billion by 2035. The company’s annual free cash flow forecasts show steady growth, fueled by both analyst input for the next few years and longer-range extrapolations. For example, FCF is expected to reach $425 million by 2028, with each year building on the next.

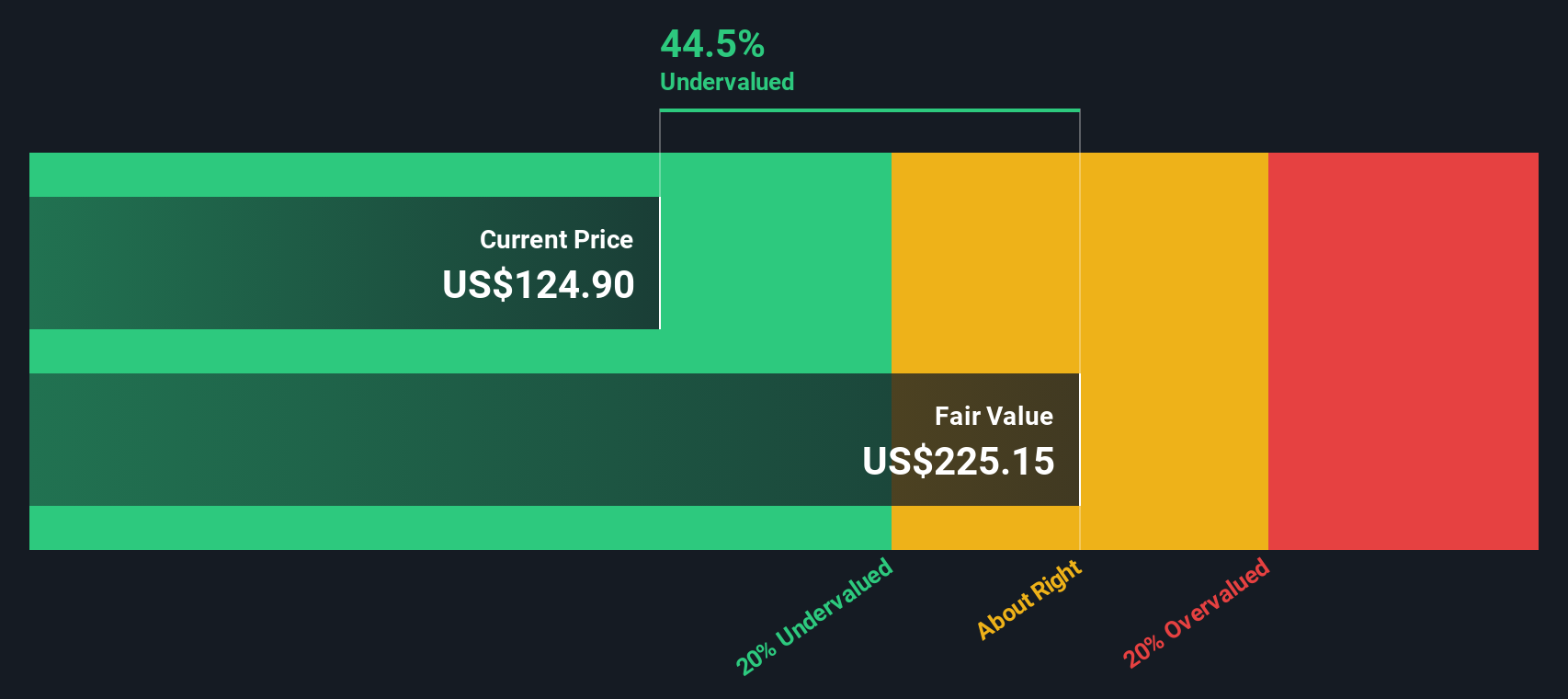

This DCF model uses a 2 Stage Free Cash Flow to Equity method, capturing both near-term analyst forecasts and estimated longer-term performance. Based on these inputs, the intrinsic value for e.l.f. Beauty comes out to $246.46 per share. This suggests the stock could be 70.1% undervalued relative to its current price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests e.l.f. Beauty is undervalued by 70.1%. Track this in your watchlist or portfolio, or discover 872 more undervalued stocks based on cash flows.

Approach 2: e.l.f. Beauty Price vs Earnings (PE Ratio)

The Price-to-Earnings (PE) ratio is a commonly used valuation metric for profitable companies because it tells investors how much they are paying for each dollar of current earnings. Since e.l.f. Beauty is generating consistent profits, using the PE ratio makes sense as it allows for direct comparison of the company to its rivals and the wider industry.

What is considered a “normal” or fair PE ratio is influenced by factors such as expected earnings growth and the level of risk. High-growth, lower-risk companies often justify higher PE multiples, while less dynamic or riskier businesses usually trade at lower multiples. This provides context for how much investors might be willing to pay for future profits.

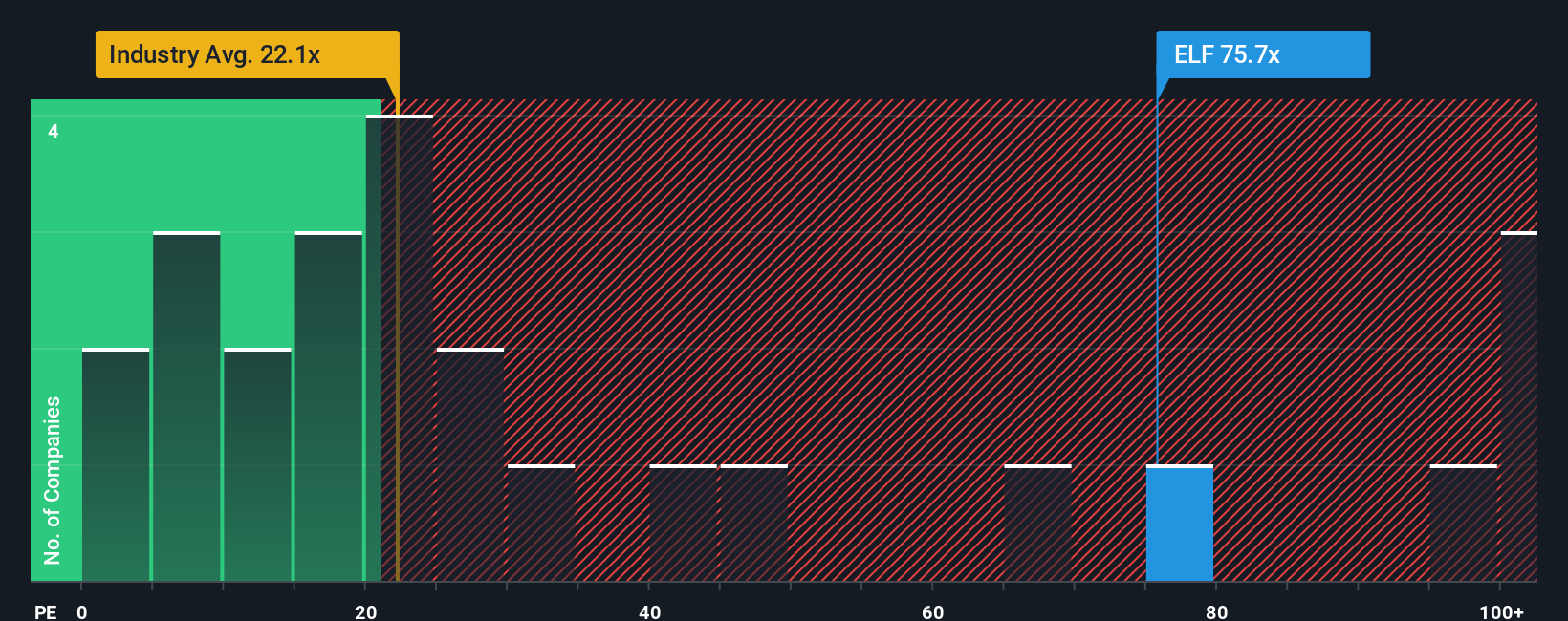

Right now, e.l.f. Beauty trades on a PE ratio of 53.6x. That is significantly higher than the Personal Products industry average of 21.5x and well above the peer group average of 14.1x. However, Simply Wall St calculates a “Fair Ratio” for e.l.f. Beauty at 34.8x. The “Fair Ratio” is a proprietary measure that considers multiple factors unique to e.l.f. Beauty, including its earnings growth outlook, profit margins, market cap, and the risks specific to the business and industry.

Rather than relying solely on broad peer values or industry averages, the “Fair Ratio” offers a more targeted benchmark. It reflects what an investor could reasonably expect to pay for e.l.f. Beauty given its growth story and risk profile, making it a more comprehensive reference point.

With a current PE ratio of 53.6x compared to a fair value of 34.8x, the stock appears overvalued on this metric, as investors are paying a premium even after factoring in attractive growth prospects.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1403 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your e.l.f. Beauty Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply your perspective on a company, where you connect the story you believe about its future with your own forecasts for key financials, such as revenue, earnings, and profit margins, to arrive at a fair value tailored to your view.

Narratives bridge the gap between a company's qualitative story and quantitative forecasts. This allows you to clearly map how your expectations about the business drive your fair value. On Simply Wall St’s Community page, Narratives are available as an accessible, easy-to-use tool embraced by millions of investors. It is simple for you to express your thesis and compare it against the crowd or consensus.

This approach empowers better decisions, as you can see whether your fair value indicates a buy or sell by comparing it to the current share price. Narratives update automatically when new information, such as earnings or breaking news, hits the market. For example, with e.l.f. Beauty, some investors create optimistic Narratives, predicting robust global expansion, higher margins, and a fair value as high as $165. Others highlight risks such as supply chain concentration and increased competition, resulting in a more conservative fair value closer to $112. This range of Narratives reflects diverse viewpoints and makes it much easier to see where and why opinions differ.

Do you think there's more to the story for e.l.f. Beauty? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.