Is EPAM Stock Attractively Priced After a 29.8% Drop in 2025?

EPAM Systems, Inc. EPAM | 135.12 135.12 | -0.21% 0.00% Post |

- Wondering if EPAM Systems is a bargain or overpriced? You are not alone. Let's dive into what really matters for investors curious about the company's true value.

- EPAM's share price recently closed at $160.91, with a minor dip of 1.2% over the past week but a rebound of 5.5% across the last 30 days. Even so, the stock is down 29.8% year-to-date and has declined by more than 20% in the last 12 months.

- Recent headlines have focused on the technology sector's volatility and global talent challenges, both of which have impacted EPAM’s perception among investors. Broader concerns about tech outsourcing trends and project delays have added to uncertainty, influencing recent price shifts.

- According to our valuation checks, EPAM Systems scores an impressive 5 out of 6 for undervaluation, putting it ahead of many software industry peers. Next, we will break down what this actually means for investors using a variety of valuation models, plus share an approach at the end that could help you make the most informed decision.

Approach 1: EPAM Systems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's fair value by projecting its future cash flows and discounting them back to today's value. This helps investors assess what the business might truly be worth, based on its current and expected financial performance.

For EPAM Systems, the latest trailing twelve months’ Free Cash Flow stands at $407.7 million. Analyst estimates cover the next five years, forecasting cash flow rising to $742 million by the end of 2029. Beyond this point, projections are extended to reflect longer-term trends, all denominated in US dollars. This trajectory suggests robust expected growth in the company’s ability to generate cash over time.

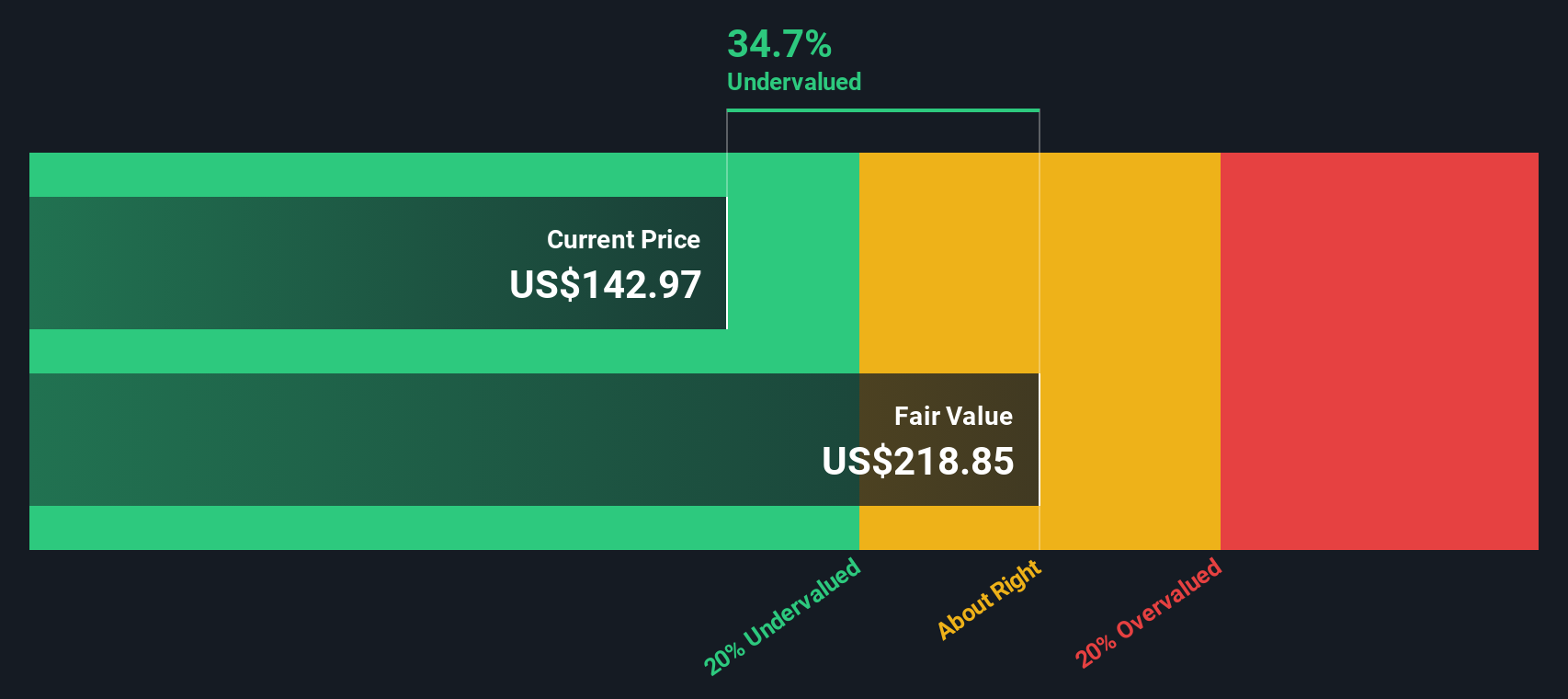

According to the two-stage Free Cash Flow to Equity model, the intrinsic value per EPAM share is estimated at $218.21. With shares currently trading at $160.91, this suggests the stock is trading at a 26.3% discount to its calculated fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests EPAM Systems is undervalued by 26.3%. Track this in your watchlist or portfolio, or discover 844 more undervalued stocks based on cash flows.

Approach 2: EPAM Systems Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most common and insightful ways to assess the valuation of profitable companies like EPAM Systems. Because PE compares a company’s current share price to its earnings per share, it enables investors to quickly gauge how much they are paying for every dollar of profit. This makes it especially relevant for businesses with a consistent history of earnings.

Growth expectations and risks play a major role in determining what constitutes a fair PE ratio. Companies with higher expected earnings growth or lower risk profiles typically command higher PE multiples, while slower-growing or riskier firms see lower ratios.

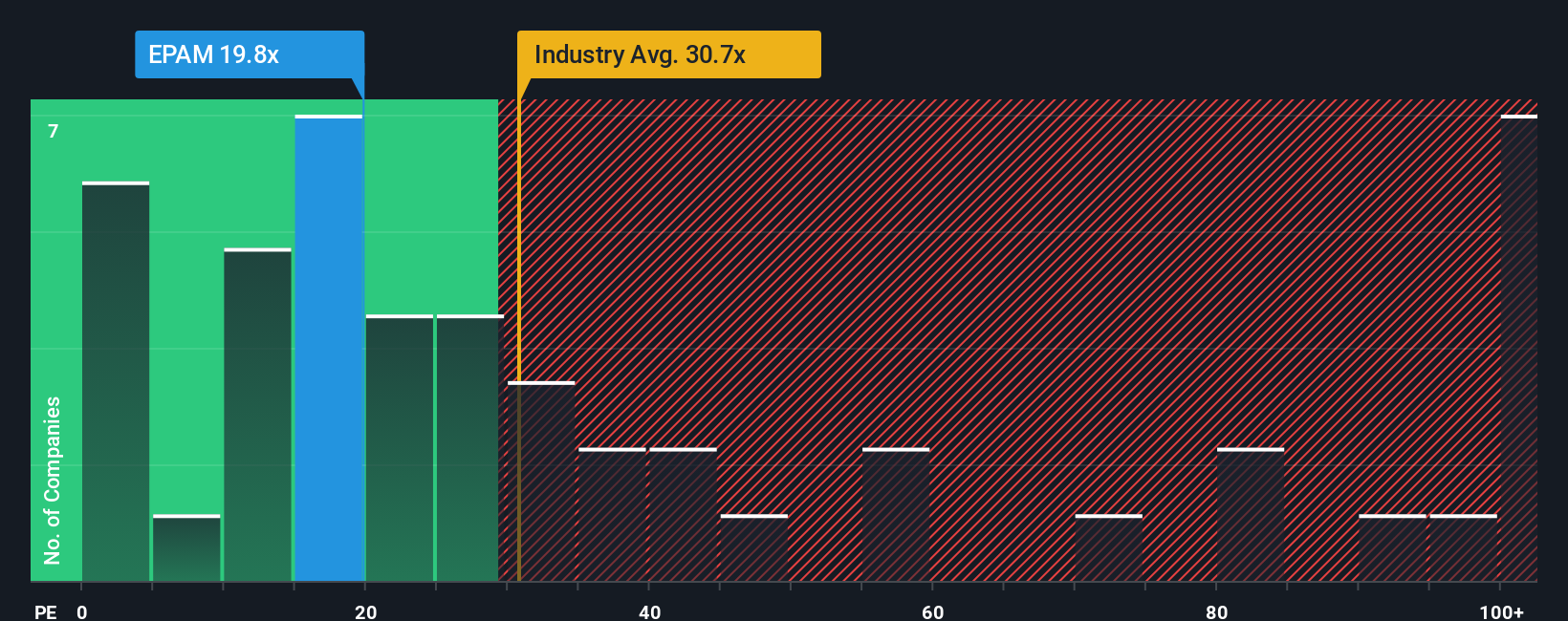

EPAM Systems currently trades at a PE ratio of 22.3x, which is notably below both the industry average of 29.7x and its peer average of 18.3x. However, to truly judge value, it is important to factor in unique elements like EPAM's earnings growth outlook, profit margins, and risk profile, not just broad industry comparisons.

This is where Simply Wall St’s Fair Ratio comes in. Based on a model that adjusts for earnings growth, risk, industry, margins, and market cap, EPAM’s Fair PE Ratio is calculated at 31.4x. This approach goes beyond broad comparisons with industry peers by reflecting relevant company-specific and sector dynamics.

With the current PE of 22.3x measured against a Fair Ratio of 31.4x, EPAM Systems appears undervalued on this basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your EPAM Systems Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are personal investment stories that let you connect your perspective on a company to the numbers by outlining how you expect EPAM Systems’ revenue, earnings, and margins will evolve. This helps you form your own fair value estimate instead of relying only on the market or analyst averages.

Simply Wall St’s Narratives tool links a company’s story directly to a financial forecast and then calculates a fair value, making this powerful approach available to all investors within the Community page. By creating or reading Narratives, you can see how shifts in the company's fortunes or new industry trends translate into updated price targets that reflect real-time news or earnings releases.

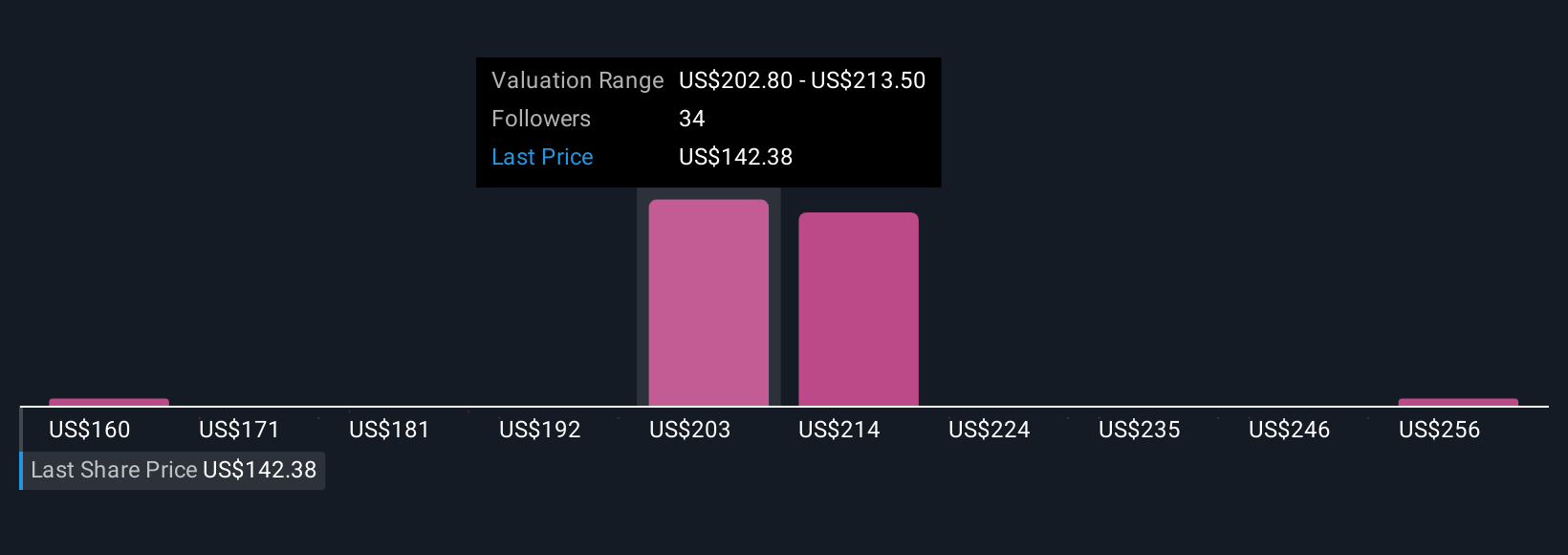

This dynamic method empowers you to understand why others believe EPAM is worth more or less than today’s price. For example, some investors currently have optimistic Narratives, seeing EPAM worth as much as $246.0 due to its AI-driven growth and operational efficiency. Others are more cautious, estimating as low as $171.0 and citing risks like competition and margin pressure. Narratives allow you to compare these sharply different views, decide which makes more sense to you, and act confidently whenever fair value and share price move out of balance.

Do you think there's more to the story for EPAM Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.