Is EPD’s 2027 CEO Transition and New Chair Structure Altering The Investment Case For Enterprise Products Partners (EPD)?

Enterprise Products Partners L.P. EPD | 0.00 |

- Enterprise Products Partners has announced that longtime Co-CEO A.J. “Jim” Teague will retire on January 4, 2027, with fellow Co-CEO W. Randall “Randy” Fowler set to assume sole chief executive responsibilities and an expanded Office of the Chairman supporting governance and continuity.

- This planned succession marks a major shift in executive leadership that could influence how Enterprise Products Partners prioritizes future midstream growth projects and capital allocation decisions.

- We’ll now examine how Fowler’s move to sole CEO and the strengthened Office of the Chairman could influence Enterprise Products Partners’ investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to be comfortable with a large, diversified midstream operator whose value hinges on keeping its assets full, reliable and well financed. The planned transition to Randy Fowler as sole CEO in 2027, supported by an expanded Office of the Chairman, does not materially alter the near term focus on bringing new Permian infrastructure online or the key risks around leverage, export exposure and producer activity.

Recent commentary from Fowler underlines Enterprise’s emphasis on growth projects in the Permian Basin, particularly gas gathering and processing that support crude production. That focus ties directly into the main catalysts investors are watching, including the ramp up of new processing plants and export facilities, but it also intersects with one of the core risks: how sensitive producer activity in the basin could be if oil prices soften toward maintenance levels.

However, even with this planned leadership shift, investors should be aware that the company’s sizeable debt load and interest rate exposure could...

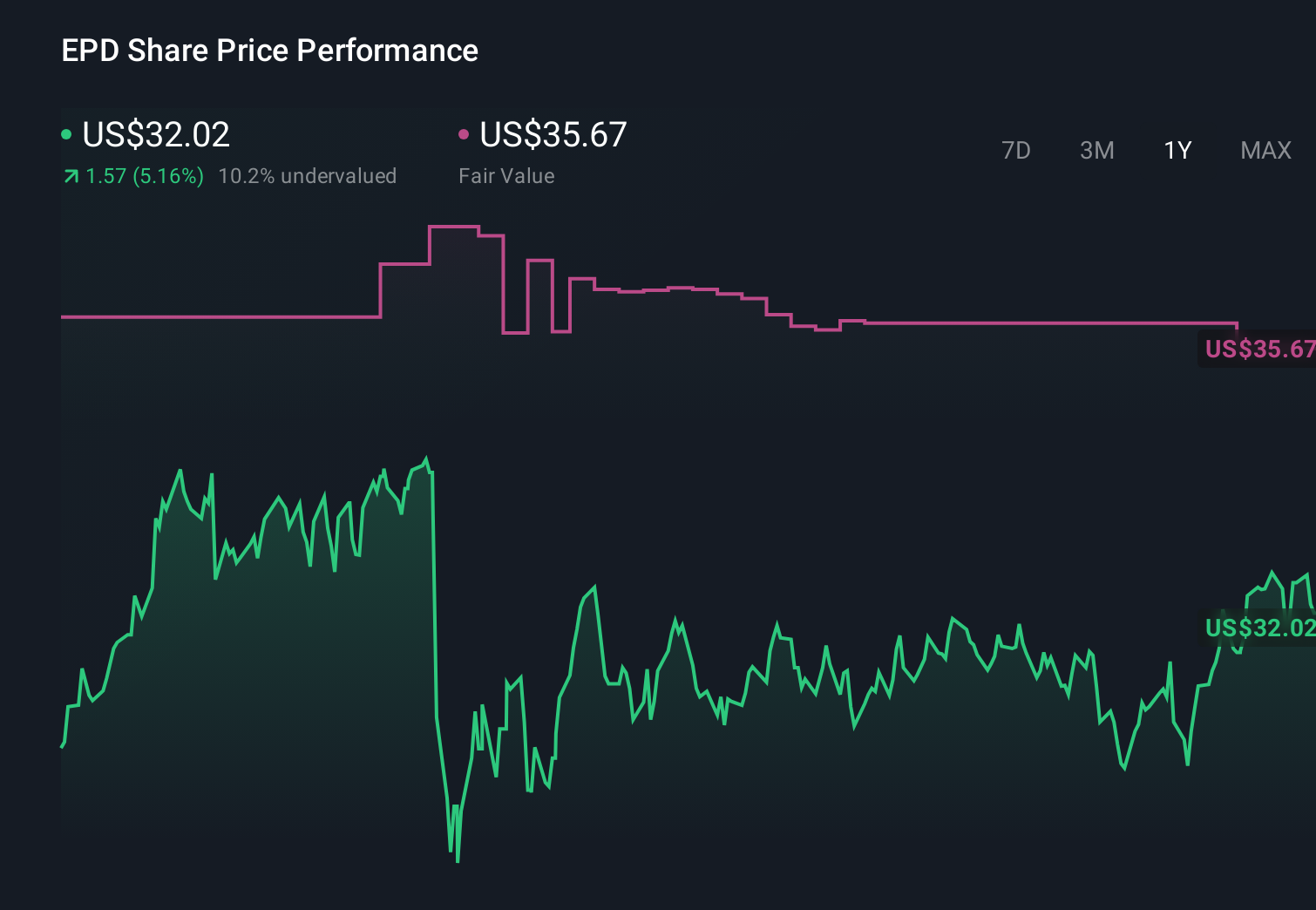

Enterprise Products Partners' narrative projects $61.3 billion revenue and $7.5 billion earnings by 2029. This requires 5.9% yearly revenue growth and a $1.7 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $41.25 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from US$35.25 to US$96.13, reflecting very different expectations. As you weigh those views, remember that Enterprise’s sizeable debt and sensitivity to credit conditions may influence how its future performance aligns with any of these numbers.

Explore 6 other fair value estimates on Enterprise Products Partners - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.