Is ePlus (PLUS) Using NVIDIA-Powered Private AI To Deepen Its Enterprise Moat Or Stretch Thin?

ePlus PLUS | 0.00 |

- Earlier this week, ePlus Inc. announced its Private AI Infrastructure Managed Service, an end-to-end, production-ready AI foundation built on Digital Realty’s PlatformDIGITAL, Lenovo’s Hybrid AI Advantage, and high-performance NVIDIA-accelerated computing clusters in secure colocation facilities.

- By combining full-stack NVIDIA AI platforms with ePlus-designed, owned, and managed infrastructure-as-a-service, enterprises gain tighter control, enhanced security, and long-term value extraction from their AI investments.

- We’ll now examine how ePlus’s new NVIDIA-powered Private AI Infrastructure Managed Service could influence its AI-focused investment narrative and growth mix.

Find 46 companies with promising cash flow potential yet trading below their fair value.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can convert AI, security, and cloud demand into higher margin, recurring services while managing project-driven revenue swings and cost pressures. The new NVIDIA-powered Private AI Infrastructure Managed Service supports that services-led thesis, but does not materially change the near term risk that large, nonrecurring enterprise projects could still drive lumpiness in results and margins.

Among recent updates, the February 2026 guidance raise to 20–22% net sales growth for the year is most relevant, as it reflects management’s confidence in demand for higher value offerings such as AI infrastructure and managed services. Together with the Private AI launch, it frames a near term catalyst around whether services and recurring revenue can scale fast enough to offset exposure to big-ticket, lower margin enterprise deals.

Yet, beneath this promising AI story, investors should be aware that revenue still leans heavily on large, potentially nonrecurring projects that could...

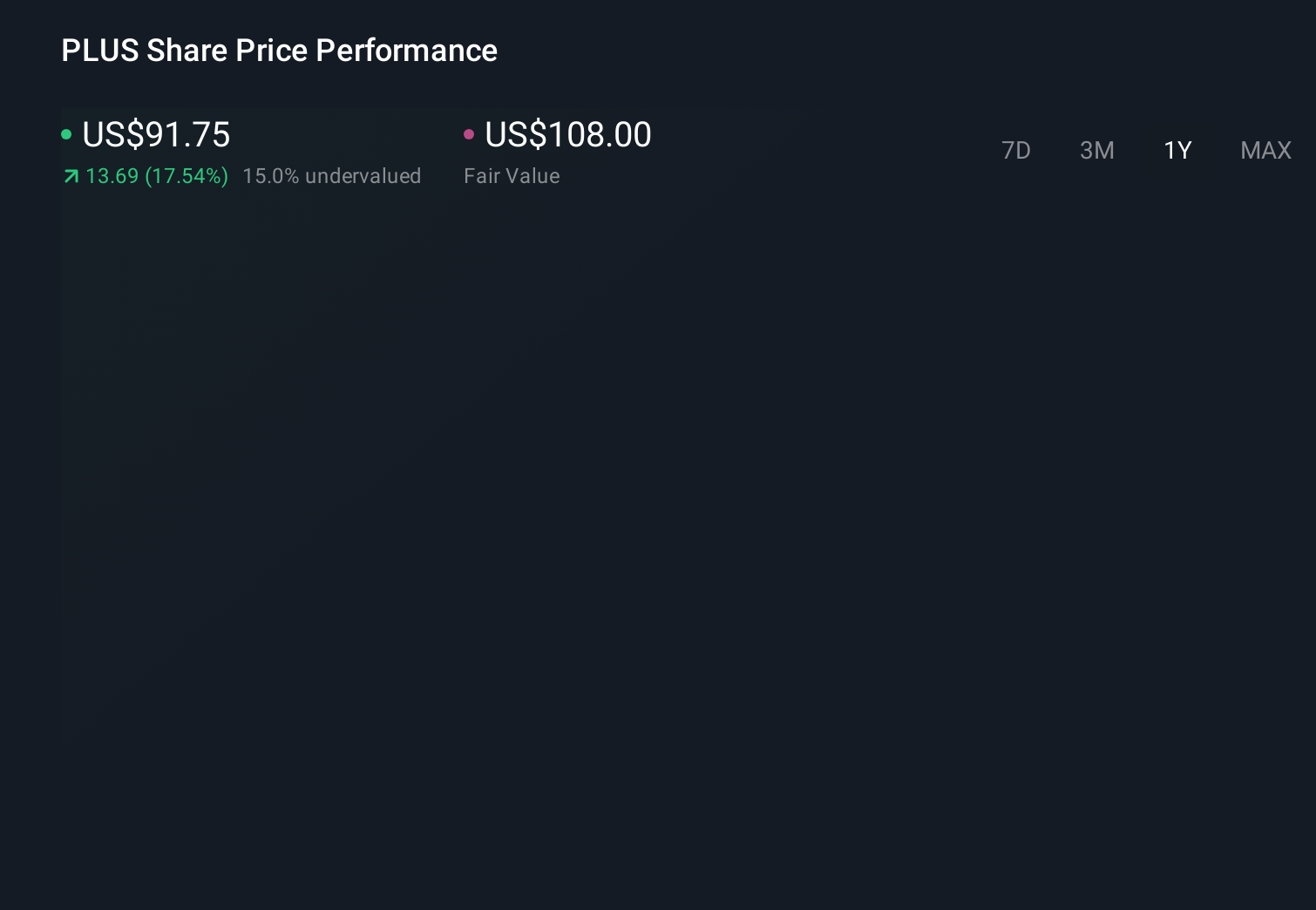

ePlus’ narrative projects $2.8 billion revenue and $142.6 million earnings by 2029. This requires 5.4% yearly revenue growth and a $5.5 million earnings decrease from $148.1 million today.

Uncover how ePlus' forecasts yield a $115.00 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates for ePlus currently sit between US$91.28 and US$115, highlighting how differently individual investors can view the same stock. Against that backdrop, the new NVIDIA-backed Private AI service sharpens the focus on whether ePlus can grow higher margin, recurring services fast enough to reduce its reliance on volatile large projects and support more stable performance over time.

Explore 2 other fair value estimates on ePlus - why the stock might be worth just $91.28!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ePlus research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.