Is Etsy (ETSY) Undervalued Or Already Priced In After Its Recent Rebound?

Etsy, Inc. ETSY | 0.00 |

Recent share performance for Etsy stock

Etsy (ETSY) has drawn fresh attention after a volatile stretch for the stock, with recent trading reflecting a mix of shorter term weakness and longer term recovery that may prompt investors to reassess its current valuation.

Over the past day, Etsy's share price declined 3.3%, and over the past week the stock fell 6.7%. Despite this, it is up about 5.6% over the past month and 41% over the past 3 months.

Year to date, Etsy is up 27.1%, and the total return over the past year is 37.5%. Over longer horizons, total returns over the past 3 years and past 5 years show declines of 14.5% and 62.2% respectively, underlining a mixed track record for longer term holders.

At a share price of $72.83, Etsy has recently combined a 5.6% 1 month share price gain and a 41.0% 3 month share price return with a 37.5% 1 year total shareholder return, but 3 and 5 year total shareholder returns remain negative, suggesting improving momentum after a difficult longer term period.

If you are weighing Etsy's recent rebound against other opportunities in online commerce and digital platforms, it can be useful to broaden your search and review 20 top founder-led companies

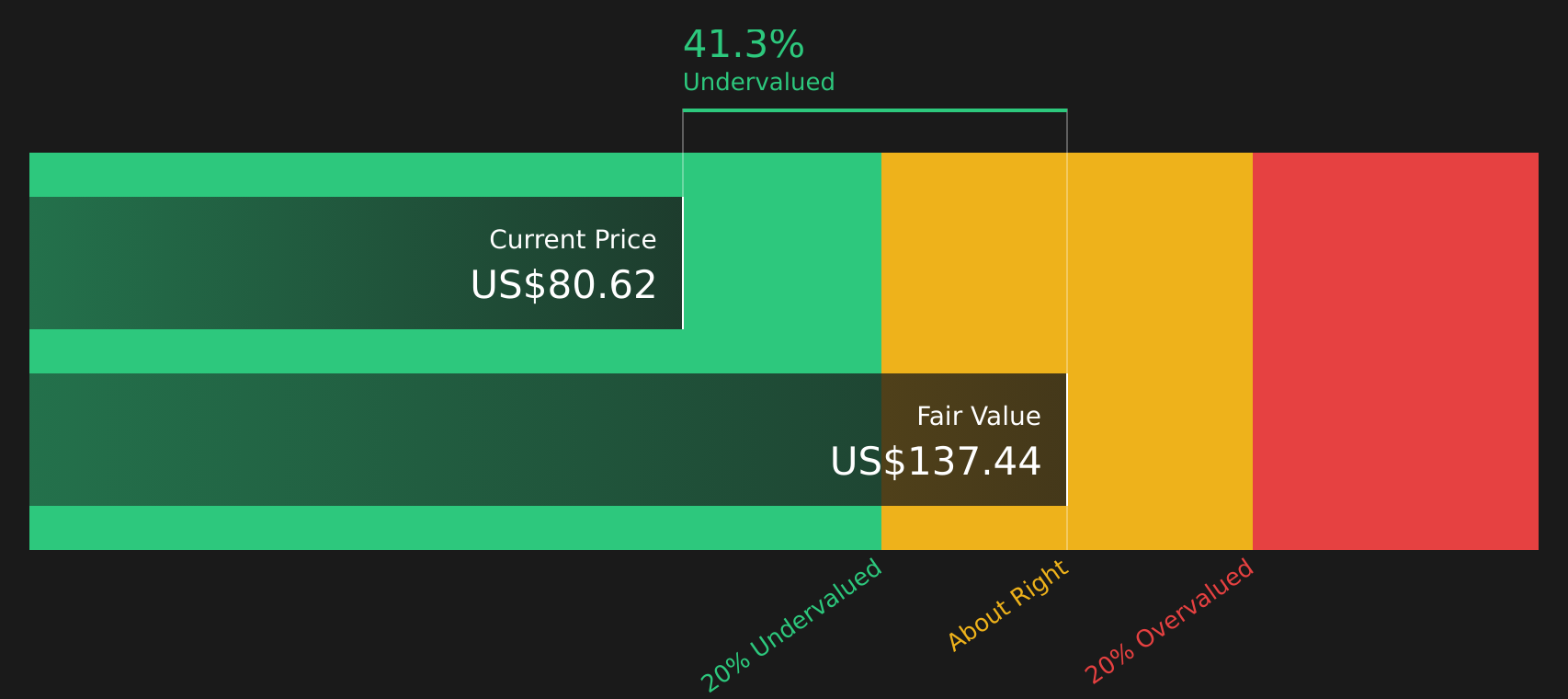

With Etsy trading close to recent analyst targets but sitting on an estimated 46% intrinsic discount, the key question is whether the current price reflects a genuine margin of safety or if the market already assumes stronger growth ahead.

Most Popular Narrative: 13% Overvalued

The most followed narrative on Etsy values the stock at $64.45 per share, which sits below the recent closing price of $72.83. This sets up a valuation debate around maturity versus relevance.

Etsy’s challenge is not relevance, it’s restraint. The platform still owns a unique corner of e-commerce, defined by creativity and connection. For investors, ETSY represents a marketplace built on identity rather than scale. If management protects the ecosystem while monetizing carefully, Etsy can remain differentiated, even as the broader e-commerce world grows louder, faster, and more commoditized.

Want to understand why this narrative pegs Etsy above its fair value line? It leans on measured growth, disciplined profitability, and a valuation multiple that treats the company less like a hyper growth story and more like a seasoned marketplace with steady economics.

Result: Fair Value of $64.45 (OVERVALUED)

However, Etsy’s fee pressure on sellers and rising competition from broader e commerce platforms could weaken seller loyalty and compress the marketplace economics that underpin this narrative.

Another view on Etsy's valuation

While the most popular narrative sees Etsy as 13% overvalued at $72.83, our DCF model points in the opposite direction. On those cash flow assumptions, Etsy screens as undervalued, with a fair value estimate of $135.22 per share, roughly suggesting a wide valuation gap.

This kind of split between a $64.45 narrative fair value and a $135.22 DCF outcome leaves you with a judgment call: are the cash flow assumptions too generous, or are shorter term concerns weighing more heavily on sentiment than the long run math implies?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Etsy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Etsy split between opportunity and caution, take a moment to move quickly, test the assumptions that matter most to you, and weigh 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Etsy?

If Etsy has you rethinking your watchlist, do not stop there. The best opportunities often sit just outside your current radar, so keep widening the lens.

- Scan for potential mispricing by checking companies that score well on quality and valuation using the 41 high quality undervalued stocks.

- Prioritise resilience by reviewing the 73 resilient stocks with low risk scores and see which stocks may better align with your tolerance for setbacks.

- Spot earlier stage opportunities with solid foundations by exploring the screener containing 19 high quality undiscovered gems before they attract broader attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.