Is FactSet Research Systems (FDS) Looking Attractive Again After Recent Share Price Rebound?

FactSet Research Systems Inc. FDS | 0.00 |

- Wondering if FactSet Research Systems at around US$253 per share is starting to look attractive again, or if the stock still carries too much downside risk for your portfolio?

- The share price has risen about 7.5% over the last week and 12.9% over the last month, even though the stock remains down about 11.0% year to date and has fallen about 40.6% over the past year.

- Recent headlines have focused on FactSet Research Systems as a key data provider within capital markets, with investors reacting to how its services are being used by asset managers and other financial institutions. This context helps explain why sentiment around the stock has shifted at points, even while the longer term share price performance has been weak.

- On Simply Wall St's 6-point valuation checklist, FactSet Research Systems currently scores 4 out of 6. The rest of this article will walk through what that means across different valuation methods, then finish with a way to think about value that goes beyond the usual ratios.

Approach 1: FactSet Research Systems Excess Returns Analysis

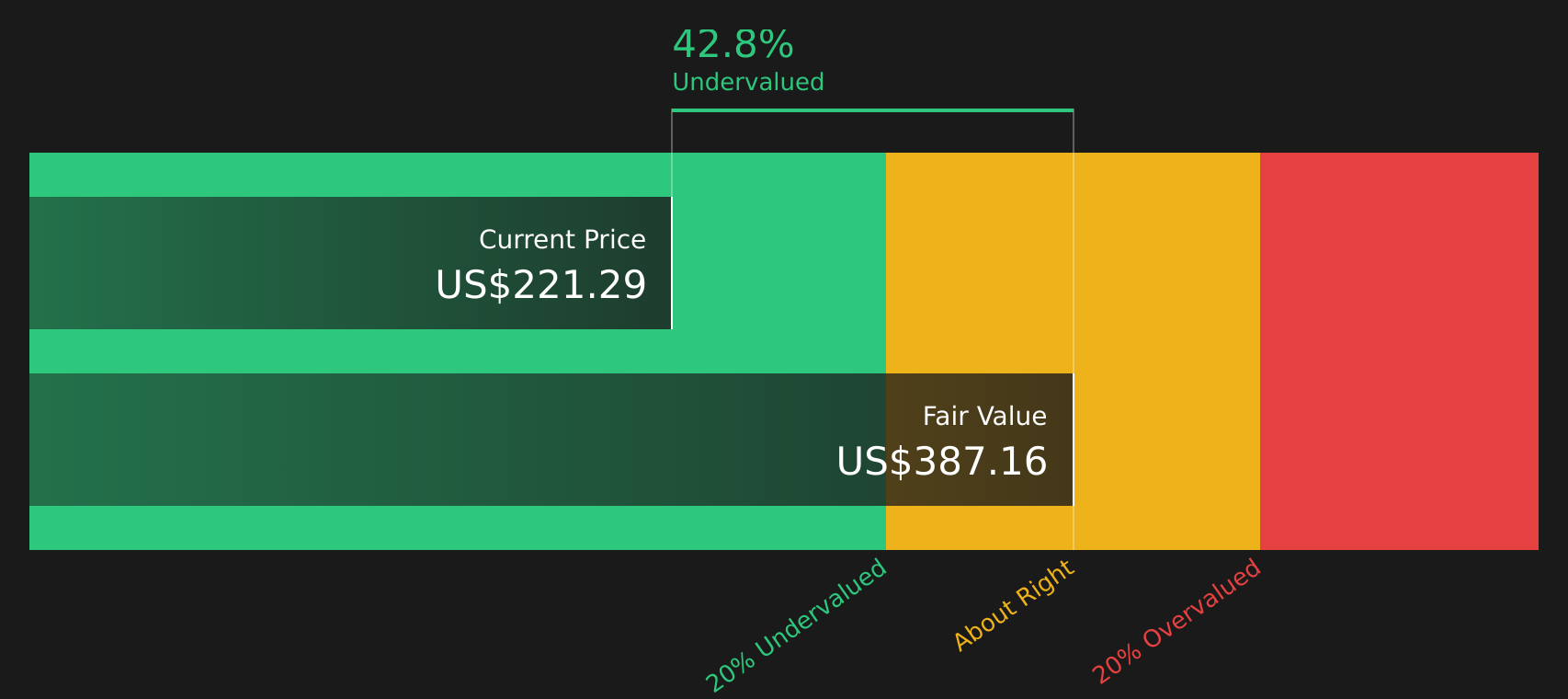

The Excess Returns model looks at how much value a company creates above the return that shareholders require. Instead of focusing on cash flows, it compares the earnings generated on the equity base to the cost of that equity and projects this relationship forward.

For FactSet Research Systems, the model uses a Book Value of $58.11 per share and a Stable EPS of $20.23 per share, based on weighted future Return on Equity estimates from 4 analysts. With an Average Return on Equity of 29.47% and a Stable Book Value of $68.67 per share, the company is modeled as generating an Excess Return of $14.67 per share over a Cost of Equity of $5.57 per share.

When these excess returns are projected and discounted, the model arrives at an estimated intrinsic value of about $389.68 per share. Compared with the recent share price around $253, this implies the stock is approximately 35.0% undervalued according to this method.

Result: UNDERVALUED

Our Excess Returns analysis suggests FactSet Research Systems is undervalued by 35.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: FactSet Research Systems Price vs Earnings

For a profitable company like FactSet Research Systems, the P/E ratio is a straightforward way to think about what you are paying for each dollar of earnings. It links directly to the business result that ultimately matters for shareholders, earnings per share.

What counts as a “normal” or “fair” P/E depends in part on how quickly earnings are expected to grow and how risky those earnings are. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk can point to a lower one.

FactSet Research Systems currently trades on a P/E of 15.71x. That sits below the Capital Markets industry average of 39.26x and below the peer average of 21.82x. Simply Wall St also provides a proprietary Fair Ratio of 15.31x, which is the P/E level suggested by factors such as earnings growth profile, industry, profit margins, market cap and company specific risks. This Fair Ratio is more tailored than a basic peer or industry comparison because it adjusts for the company’s own characteristics rather than treating all companies as interchangeable. With the actual P/E only slightly above the Fair Ratio, the valuation appears broadly consistent with these fundamentals.

Result: ABOUT RIGHT

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your FactSet Research Systems Narrative

Earlier the article mentioned that there is an even better way to understand valuation, so meet Narratives, a simple tool on Simply Wall St's Community page where you can attach your story about FactSet Research Systems to the numbers by setting your own fair value and assumptions for future revenue, earnings and margins. You can then see how that compares with the current price and with other investors. For example, one Narrative prices FactSet around US$200 based on more cautious AI and margin views, and another sees fair value closer to US$430 based on expectations for stronger AI adoption and higher earnings. Each Narrative updates automatically as fresh news or results arrive, so your buy and sell decisions always start from a clear, numbers backed story you actually agree with.

For FactSet Research Systems, here are previews of two leading FactSet Research Systems Narratives:

Fair value: US$313.99

Implied undervaluation vs last close: about 19.3% below this fair value

Revenue growth assumption: 15%

- Argues the market is treating FactSet Research Systems as if generative AI will permanently damage its business, while underappreciating its shift toward infrastructure style services over the last five years.

- Highlights a multi layer moat built around CUSIP, Vermilion and Portware, which are described as embedded, high margin workflows that would be difficult and costly for clients to replace.

- Frames AI as a tool for efficiency inside products like Cobalt and Vermilion, supporting margins and pricing, rather than a direct threat to the value of FactSet Research Systems offerings.

Fair value: US$252.44

Implied overvaluation vs last close: about 0.4% above this fair value

Revenue growth assumption: 5.52%

- Leans on analyst assumptions that revenue grows in the mid single digits, margins edge up slightly and earnings reach US$712.8m by about May 2029, with a P/E of 14.6x applied to those earnings.

- Points to rising technology spend, pressure on asset management and banking budgets and execution risk in regions like EMEA as factors that could limit growth and weigh on margins.

- Emphasizes that analyst price targets span a wide range from US$200 to US$380, so readers are encouraged to test these inputs against their own expectations before relying on any single fair value.

If you want to go beyond these previews and see the full assumptions behind each story, including how other investors are framing potential risks and rewards, check out the wider range of community Narratives for FactSet Research Systems.Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for FactSet Research Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.