Is Flowers Foods (FLO) Now A Potential Opportunity After A 49% One-Year Share Price Fall

Flowers Foods FLO | 0.00 |

- Wondering if Flowers Foods at around US$8.09 is a bargain or a value trap? This article walks through what the current price might be implying about the stock.

- The share price is down 6.4% over the past week, roughly flat over the last month, and has fallen 25.0% year to date and 49.3% over the past year, which may have changed how the market views its risk and reward profile.

- Recent coverage has focused on how extended share price weakness is affecting sentiment toward consumer staples stocks like Flowers Foods. Some investors are questioning whether defensive food stocks still justify their past valuations. At the same time, analysts and commentators have been reassessing what a more cautious outlook could mean for long term pricing power and margins in the packaged foods space.

- Simply Wall St currently gives Flowers Foods a valuation score of 2 out of 6. Next up is a look at how different valuation methods stack up for this stock and why a broader framework at the end of this article may help you judge its fair value more clearly.

Flowers Foods scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

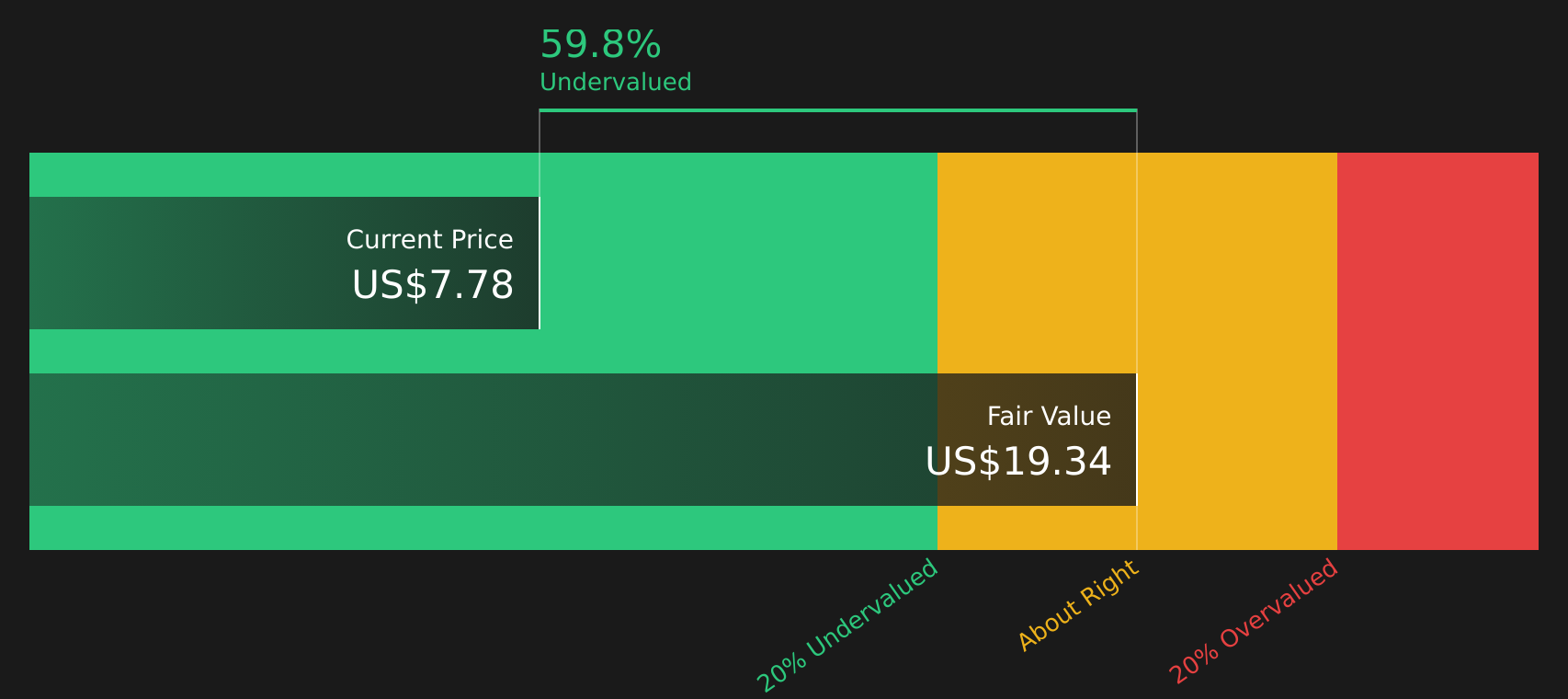

Approach 1: Flowers Foods Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting its future cash flows and discounting them back to today using an appropriate rate. It is essentially asking what all those future dollars are worth in today’s terms.

For Flowers Foods, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The company’s last twelve months Free Cash Flow is about $305.6 million. Analyst inputs and extrapolated estimates from Simply Wall St point to projected Free Cash Flow of $313.3 million in 2026, $301.6 million in 2027 and $174.0 million in 2028, with further extrapolated figures through 2035.

When those projected cash flows are discounted back to today, the DCF model indicates an estimated intrinsic value of about $15.58 per share. Compared with the recent share price of around $8.09, this framework suggests the stock is trading at roughly a 48.1% discount to that intrinsic value. This indicates a material gap between the current market price and this cash flow based estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Flowers Foods is undervalued by 48.1%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Approach 2: Flowers Foods Price vs Earnings

For a profitable company, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of earnings, which makes it a practical way to compare valuation across established businesses like Flowers Foods.

What counts as a "normal" or "fair" P/E usually reflects how the market views a company’s growth potential and risk profile. Higher expected earnings growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk can point to a lower multiple.

Flowers Foods currently trades on a P/E of 20.45x. That is above the Food industry average P/E of 16.21x and slightly above the peer group average of 19.16x. Simply Wall St also calculates a proprietary “Fair Ratio” of 19.68x for Flowers Foods, which is the P/E level suggested by factors such as its earnings characteristics, margins, industry, market cap and risk profile.

The Fair Ratio is designed to be more tailored than a simple comparison with peers or the broad industry, because it brings those business specific factors together rather than relying only on averages.

Comparing the current P/E of 20.45x with the Fair Ratio of 19.68x indicates that the stock screens as slightly overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Flowers Foods Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple way for you to attach a clear story about a company to hard numbers like fair value, future revenue, earnings and margins. You can then see how that story lines up against the current share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. Each Narrative connects a thesis about Flowers Foods to a full forecast and a fair value, then helps you judge whether the stock looks expensive or cheap by comparing that fair value with today’s price.

These Narratives refresh when new earnings, guidance or news arrive, so your fair value view does not stay static. For Flowers Foods you can already see a wide range of stories, from a bullish Narrative with a fair value of US$20.00 at one end through to a more cautious Narrative around US$7.00 at the other. There are alternatives such as US$16.12 and the analyst consensus of US$10.67 in between, giving you clear, quantified perspectives to compare with your own view.

For Flowers Foods however we will make it really easy for you with previews of two leading Flowers Foods Narratives:

Fair value: US$16.12 per share

Implied discount to this fair value at the recent US$8.09 share price: about 49.8% undervalued

Revenue growth assumption: 1.15% a year

- The Simple Mills acquisition and Wonder branded snack expansion point to a broader product mix across health focused and indulgent categories.

- Higher leverage from US$795 million of senior debt puts more focus on cash generation and balance sheet discipline.

- A board refresh, guidance for modest growth and an increased dividend are framed as signs of a company working through a transition period while still prioritizing income for shareholders.

Fair value: US$7.00 per share

Implied premium to this fair value at the recent US$8.09 share price: about 15.6% overvalued

Revenue trend assumption: revenue is expected to decline about 0.53%

- Slower demand for traditional packaged bread, changing consumer preferences and demographic shifts are viewed as structural headwinds for core volumes.

- Competition from private label and smaller bakery rivals, together with possible regulatory costs, is seen as a drag on margins.

- The fair value of US$7.00 is based on flat revenue, modest margin improvement and a future P/E of about 13.8x, below both today's multiple and the wider US Food industry.

These Narratives sit either side of the current share price and use different assumptions about revenue, margins and valuation multiples. They give you a clear range of outcomes to compare with your own expectations for Flowers Foods.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Flowers Foods on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Flowers Foods? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.