Is Freshworks a Bargain After Its 28% Slide and New AI Integration News?

Freshworks, Inc. Class A FRSH | 8.32 | +3.10% |

Thinking about what to do with Freshworks stock? You are definitely not alone. The last year has been a bit of a rollercoaster, and investors are deciding whether this growth story is just getting started or if there is more risk than reward. After closing recently at $11.40, Freshworks is down about 1.0% over the last week, off 14.2% in the past month, and has slipped 28.3% so far this year. That is a big drop, especially compared to a small 2.2% gain over the last twelve months. Digging back over the past three years, shares have actually lost 12.2% of their value.

So what is going on here? Part of the movement is tied to shifts in how the broader market views high-growth tech companies. Ongoing developments in the software sector and cautious investor sentiment have contributed to some of these swings in Freshworks’ stock price. It is not just about the company itself, but also about how risk and reward are being valued in this environment. Despite the recent turbulence, something interesting is happening under the hood: when you assess Freshworks’ current valuation, it actually scores a 5 out of 6 on our typical undervalued company checklist. That is a strong signal that it might be cheaper than the headlines suggest.

Curious which valuation methods make Freshworks look attractive, and which area leaves room for improvement? Let us break down each valuation lens in detail, then talk about an even smarter way to judge if this stock is a buy or a pass.

Approach 1: Freshworks Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a company is worth by forecasting its future cash flows and then discounting them back to today’s value. This method aims to capture the present value of all money Freshworks is expected to generate in the coming years.

For Freshworks, the current Free Cash Flow stands at $185 million. Analyst projections extend up to five years, and Simply Wall St extrapolates these trends forward for a further five years, resulting in an estimated Free Cash Flow of $594 million by 2035. These figures indicate consistent growth in the company’s ability to generate cash, which can be a positive signal for long-term investors.

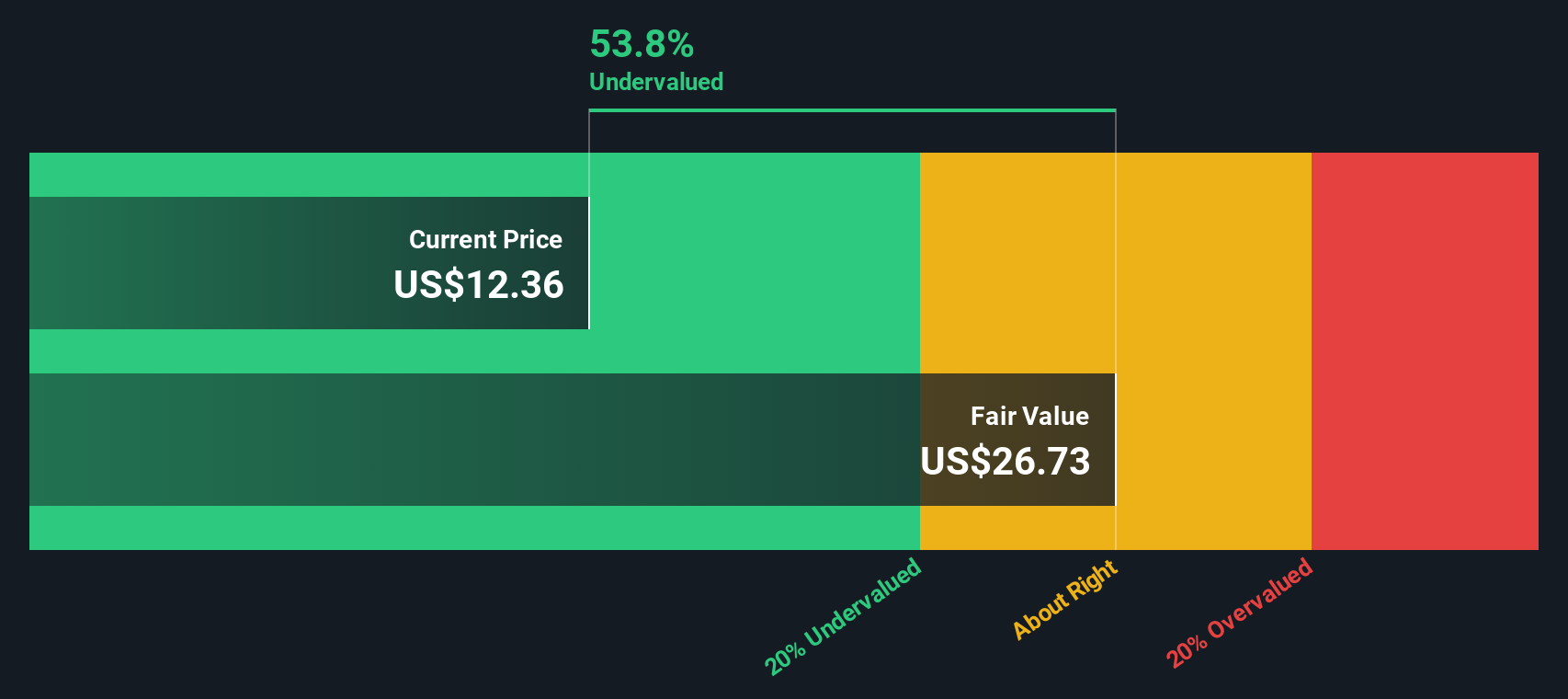

Bringing all those future cash flows back to today, the DCF model estimates Freshworks' intrinsic value at $26.81 per share. With the stock currently trading at $11.40, this suggests the market price is about 57.5% below what the company is worth based on these projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Freshworks is undervalued by 57.5%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Freshworks Price vs Sales

The Price-to-Sales (P/S) ratio is a commonly used metric for valuing companies that may not yet be consistently profitable. This makes it a great fit for Freshworks. This ratio focuses on revenues rather than profits, and is especially relevant for growth-stage software businesses, where high reinvestment rates can keep net earnings low but revenue growth remains robust.

In the current environment, a "normal" or fair P/S ratio depends on how quickly a company is growing and the risks involved in sustaining that momentum. High-growth companies often carry higher P/S multiples, as investors anticipate strong future expansion. Companies with more risk or slower expected growth typically see lower multiples.

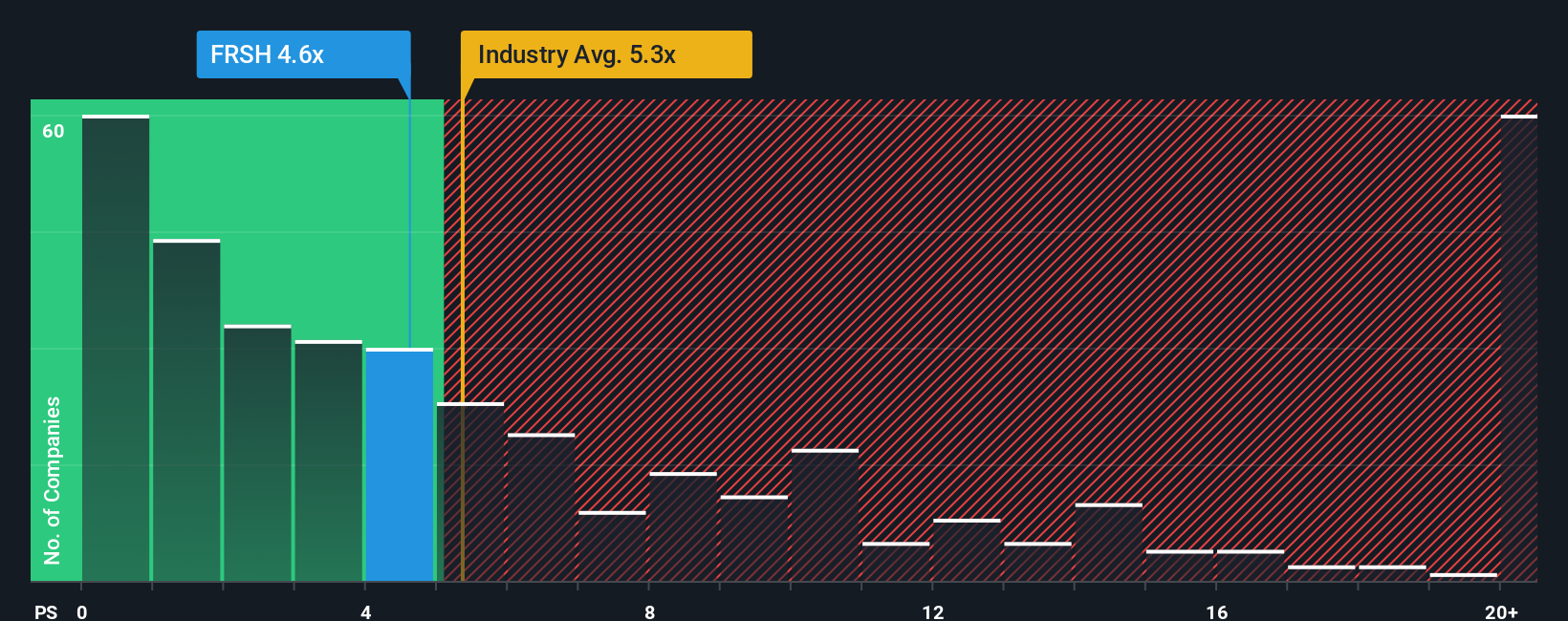

Right now, Freshworks trades at a P/S ratio of 4.25x. For perspective, the industry average is 5.18x and its closest peers average 6.21x. However, Simply Wall St’s proprietary “Fair Ratio,” which takes into account Freshworks’ growth prospects, margins, risks, industry conditions, and market cap, calculates a fair P/S multiple of 6.35x. This provides a tailored benchmark specifically for Freshworks and goes beyond broad peer or industry comparisons.

The Fair Ratio is a more nuanced guide because it blends several company-specific factors, not just raw financial results. This makes it a better reference point for judging proper valuation in today's dynamic software sector.

Comparing Freshworks’ current P/S multiple of 4.25x with its Fair Ratio of 6.35x, the stock appears attractively priced against what it may be worth in context.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Freshworks Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives are a simple but powerful concept: instead of just relying on numbers, they allow you to connect your own story about a company with your perspective on its market position, growth drivers, risks, and future, along with your assumptions about future revenues, margins, and a fair value. This means your investment decision is driven by both the big picture and the bottom line.

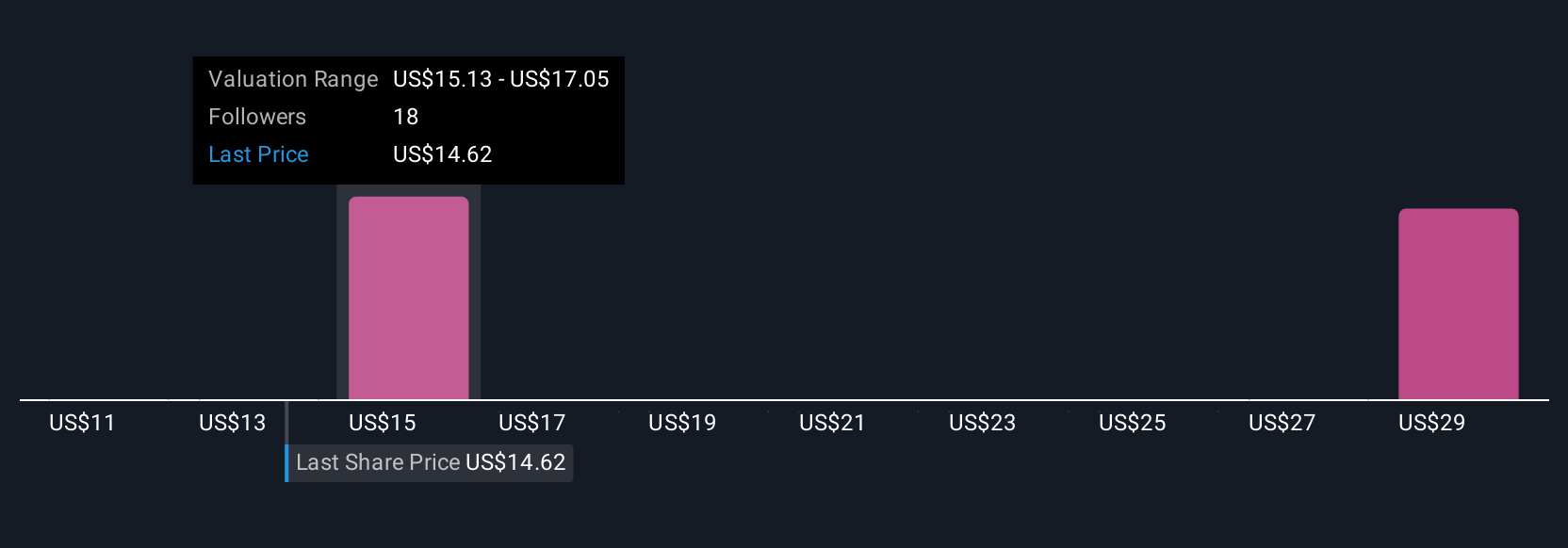

A Narrative essentially links what you believe about Freshworks with a financial forecast and, ultimately, a fair price per share. Narratives are easy to use on Simply Wall St’s Community page, where millions of investors compare and refine their own views. They help you decide when to buy or sell by comparing your Narrative's fair value against the market price, making the process both clear and dynamic.

What makes Narratives truly smart is that they update automatically as new information such as news or earnings reports becomes available, ensuring your investment thesis stays relevant. For Freshworks, one investor’s Narrative might forecast rapid revenue growth fueled by strong AI adoption and global partnerships and set a fair value near $27.00 per share, while another could be more cautious, factoring in competitive and profit margin risks, and estimate a fair value closer to $18.00 per share. That is the power of Narratives: your view, quantified and ready to take action when it matters most.

Do you think there's more to the story for Freshworks? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.