Is Frontline’s Surging Q1 Dividend And EPS Altering The Investment Case For Frontline (FRO)?

Frontline Plc FRO | 0.00 |

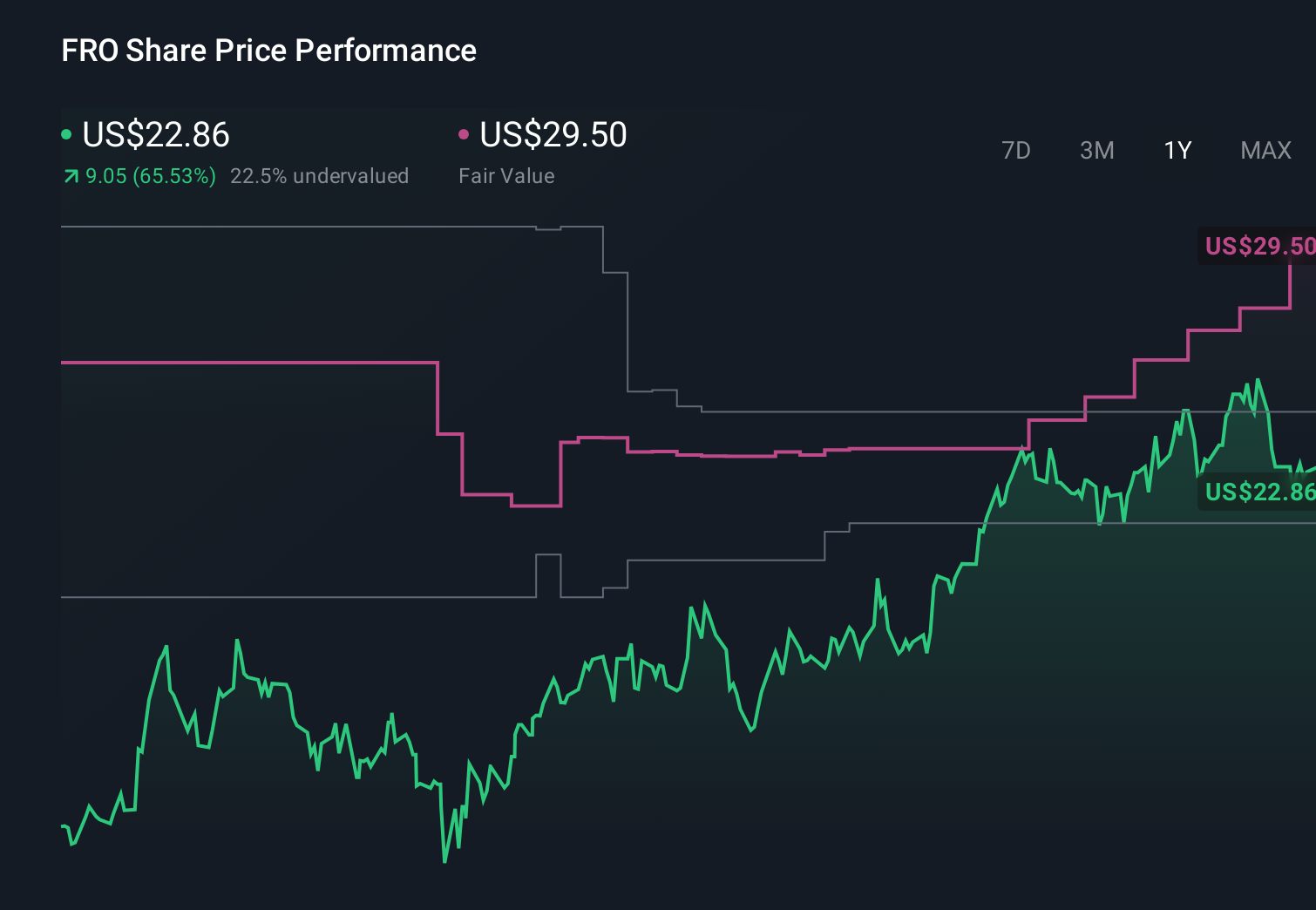

- Frontline plc has already reported first-quarter 2026 results, with revenue rising to US$929.33 million and net income to US$559.12 million, and the board declaring a US$1.55 per share dividend for shareholders of record on June 12, 2026.

- The sharp jump in quarterly earnings per share from continuing operations to US$2.51 compared with a year earlier highlights how strongly recent trading has supported the company’s capacity to distribute cash to investors.

- We’ll now examine how this higher US$1.55 per-share dividend shapes Frontline’s existing investment narrative built around fleet renewal and earnings potential.

Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

Frontline Investment Narrative Recap

To own Frontline, you need to believe that today’s tanker earnings power can support both fleet renewal and meaningful cash returns, while accepting exposure to cyclical spot rates and shifting oil trade flows. The strong Q1 2026 results and higher US$1.55 dividend reinforce the near term cash generation story, but do not remove the key risk that weaker charter markets or policy changes could quickly pressure day rates and, in turn, the company’s ability to sustain these payouts.

The Q1 2026 earnings release is the most relevant backdrop to this dividend news. Revenue of US$929.33 million and net income of US$559.12 million underline how much current conditions have lifted margins versus a year ago, supporting the step up from the prior US$1.03 per share dividend. Against this, Frontline’s sizable ECO newbuilding program still ties the investment case to successful execution and the tanker cycle as those vessels are delivered from late 2026 onward.

Yet against this strong quarter, the risk that prolonged softer spot rates and changing trade patterns could quickly pressure Frontline’s earnings is something investors should be aware of...

Frontline’s narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline but an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 20% upside to its current price.

Exploring Other Perspectives

By contrast, the most pessimistic analysts were penciling in roughly US$1.3 billion of revenue and about US$492.6 million of earnings by 2029, reminding you that views on Frontline’s exposure to geopolitics and tanker demand can differ widely and may shift again as this latest earnings and dividend surprise is fully reflected.

Explore 6 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Frontline research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.