Is Goodyear Tire & Rubber (GT) Now Attractive After A 14% One Year Share Price Decline

Goodyear Tire & Rubber Company GT | 6.59 6.60 | -2.08% +0.22% Post |

- Wondering whether Goodyear Tire & Rubber at around US$8.86 is a bargain or a value trap? This article walks through what the numbers are actually saying about the stock.

- The share price has been under pressure, with returns of a 2.6% decline over the past week, a 2.5% decline over the past month, and a 14.3% decline over the last year, which may have changed how investors view both its potential and its risks.

- Recent coverage around Goodyear has focused on its position in the tire industry and how the company is responding to changing demand patterns, regulatory pressures, and competition from global manufacturers. These themes help frame why the market might be reassessing the stock and set the context for thinking about what a fair price could look like.

- On our 6 point valuation checklist, Goodyear currently scores 3 out of 6, which raises some interesting questions about where it might be cheap and where it might still be demanding. Next we will walk through the usual valuation tools such as P/E, P/B and cash flow models, then finish with a broader way to think about value that goes beyond any single metric.

Approach 1: Goodyear Tire & Rubber Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts those back to today’s dollars to estimate what the business might be worth per share.

For Goodyear Tire & Rubber, the model used is a 2 Stage Free Cash Flow to Equity approach based on projected Free Cash Flow in US$. The latest twelve month Free Cash Flow is a loss of about $182.8 million. Analyst inputs and extrapolated estimates point to Free Cash Flow of $200.4 million in 2028, with intermediate projections such as $92.1 million in 2026 and $181.1 million in 2027, and further extrapolated figures out to 2035.

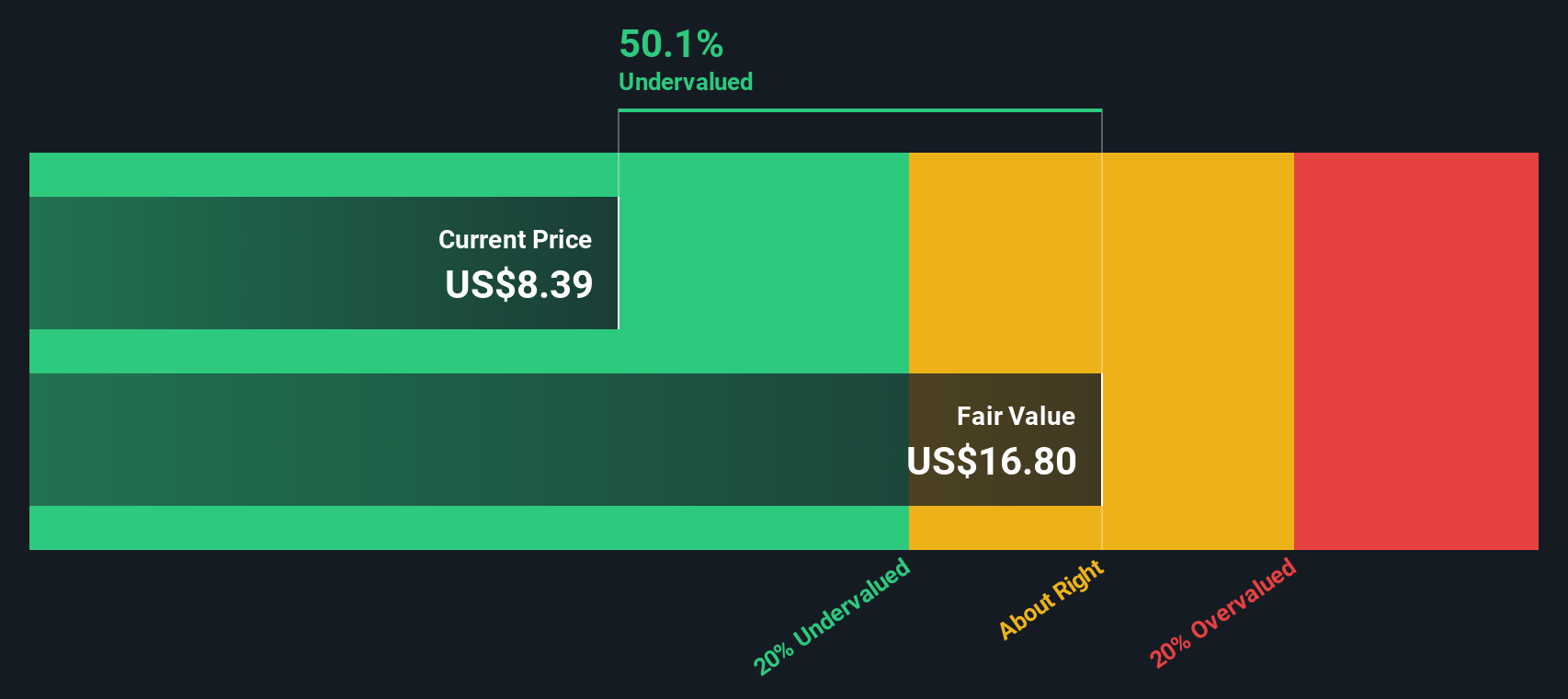

When all those projected cash flows are discounted back and combined with a terminal value, the model arrives at an estimated intrinsic value of about $7.65 per share. Against a current share price around $8.86, this implies the stock is about 15.9% overvalued under this set of assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Goodyear Tire & Rubber may be overvalued by 15.9%. Discover 56 high quality undervalued stocks or create your own screener to find better value opportunities.

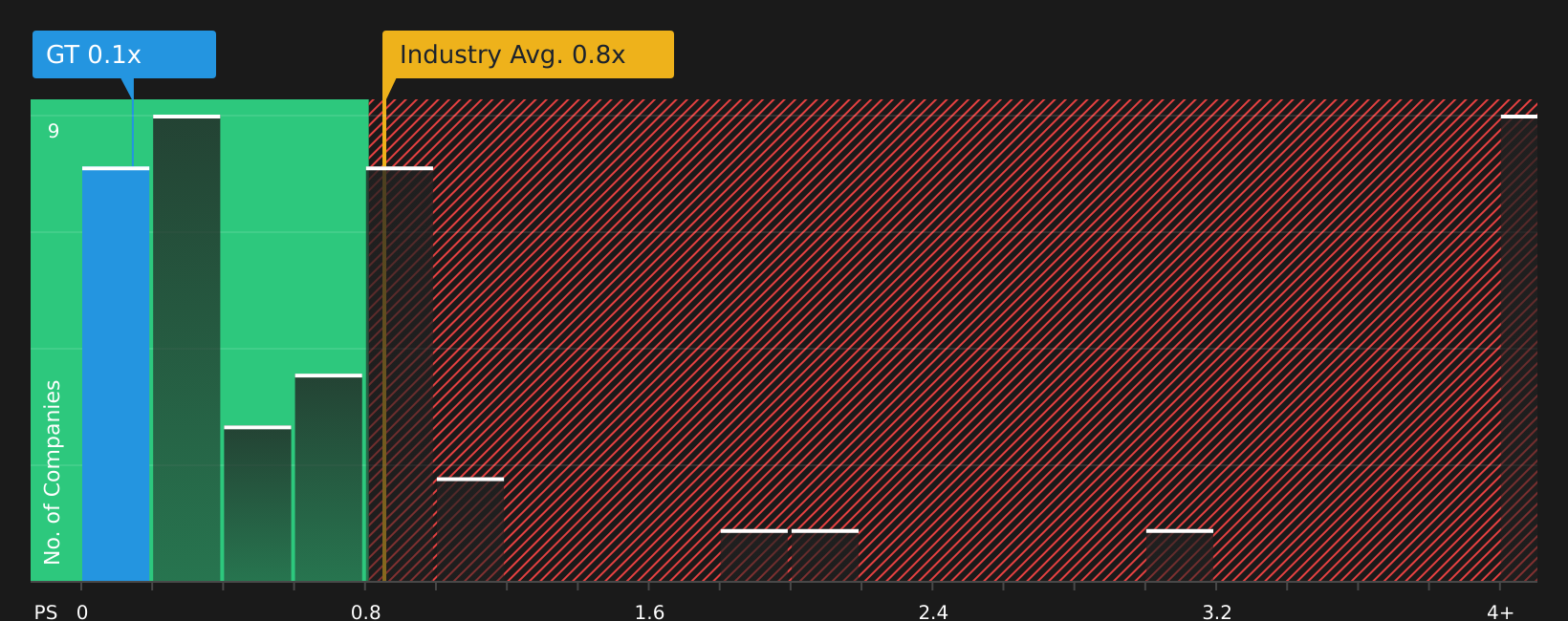

Approach 2: Goodyear Tire & Rubber Price vs Sales

For companies where earnings can be uneven, the P/S ratio is often a useful way to think about value because it compares the market value directly to the revenue the business generates, rather than profits that may be volatile or negative.

Investors usually expect higher growth and lower risk to justify a higher P/S multiple, while slower growth or higher uncertainty tend to line up with a lower, more cautious P/S level. That is why it helps to compare a company’s P/S with a few reference points instead of looking at the number in isolation.

Goodyear Tire & Rubber currently trades on a P/S of 0.14x. This sits below the Auto Components industry average P/S of 0.83x and also below the peer average of 9.30x that Simply Wall St uses for comparison. Simply Wall St then goes a step further with its proprietary Fair Ratio, which considers what P/S multiple might make sense for this specific company, given factors such as earnings growth, profit margin, industry, market cap and key risks. For Goodyear, that Fair Ratio is 0.56x, higher than the current 0.14x. On this metric, the shares appear to be trading below that Fair Ratio.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Goodyear Tire & Rubber Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives let you attach a clear story about Goodyear Tire & Rubber to the numbers you are using for fair value, future revenue, earnings and margins. You can then compare that Fair Value with the current price on Simply Wall St's Community page to see whether your story points you toward buying, holding or selling. The platform keeps that Narrative updated as new news or earnings arrive. For example, one investor might build a more optimistic Goodyear view around a fair value of about US$14.63 and revenue of roughly US$19.4b by 2028, while another might prefer a more cautious view using a fair value closer to US$7.30 and lower assumed revenue growth. Both can then see how their assumptions feed into different potential outcomes.

For Goodyear Tire & Rubber, however, we’ll make it really easy for you with previews of two leading Goodyear Tire & Rubber Narratives:

Fair value: about US$9.89 per share

Implied discount to this fair value: around 10.5% below that estimate

Revenue growth used in this view: about 17%

- Focus on premium and larger rim size tires, cost savings from the Goodyear Forward program, and modernization efforts aim to support margins, while the asset sales program is intended to improve the balance sheet and reduce financing strain.

- Analysts using this narrative work with revenue of about US$18.3b and earnings of roughly US$405.2m by 2028, together with a P/E of 11.2x and a discount rate of 12.3%, which leads them to a consensus price target of US$11.07.

- Key risks include competition from low cost imports, trade disruptions, weak commercial demand, distribution changes, and higher tariff and restructuring costs that could pressure volumes, margins, and free cash flow.

Fair value: about US$7.30 per share

Implied premium to this fair value: around 21.4% above that estimate

Revenue trend used in this view: about 38.4% decline

- This more cautious narrative centers on persistent pricing pressure from low cost imports, high debt, and soft demand, which together are seen as limiting earnings growth and leaving less flexibility to invest in future products.

- Analysts anchoring to the bearish US$9.00 price target assume revenue of about US$18.0b and earnings of roughly US$379.6m by 2028, on a P/E of 9.7x and a discount rate of 12.3%, while also working with a lower updated fair value of about US$7.30.

- Risks flagged include tariff and input cost inflation, trade related volume swings, restructuring drag, and prolonged weakness in commercial truck tires, which together could keep margins and free cash flow under pressure.

If you want to see how these stories are built and how other investors are thinking about the same numbers in more detail, you can use the Community Narratives to stress test your own assumptions against both paths for Goodyear.

Do you think there's more to the story for Goodyear Tire & Rubber? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.