Is Green Plains (GPRE) Insider Buying Reinforcing Its Clean Fuel Diversification Story?

Green Plains Inc. GPRE | 15.70 | -2.42% |

- On March 6, 2026, Green Plains director Patrick Sweeney bought 6,383 company shares, lifting his overall stake to 42,719, according to an SEC filing.

- This insider purchase, alongside strong AI-driven trading sentiment favoring an overweight bias, is drawing fresh attention to Green Plains’ outlook.

- Next, we’ll examine how Sweeney’s insider buying influences Green Plains’ existing investment narrative built around clean fuel incentives and diversification.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Green Plains Investment Narrative Recap

To own Green Plains today, you need to believe in a long-term shift toward low-carbon fuels and profitable diversification into higher value coproducts, despite recent operating losses and policy uncertainty around clean fuel incentives. Patrick Sweeney’s insider purchase supports confidence in that roadmap, but it does not materially change the key near term catalyst, which remains the effective monetization of 45Z and other carbon credits, or the main risk of continued earnings volatility if execution on the transition slips.

The most relevant recent update alongside Sweeney’s buying is the AI driven trading sentiment that supports an overweight bias and offers momentum and risk hedging strategies keyed to Green Plains’ support and resistance levels. While this is trading focused rather than fundamental, it interacts directly with catalysts by potentially amplifying short term moves around policy developments or earnings surprises, at a time when the company is still unprofitable and reliant on consistent operational progress.

Yet behind the bullish AI signals, investors should still be aware of how dependent Green Plains remains on future clean fuel policy stability and...

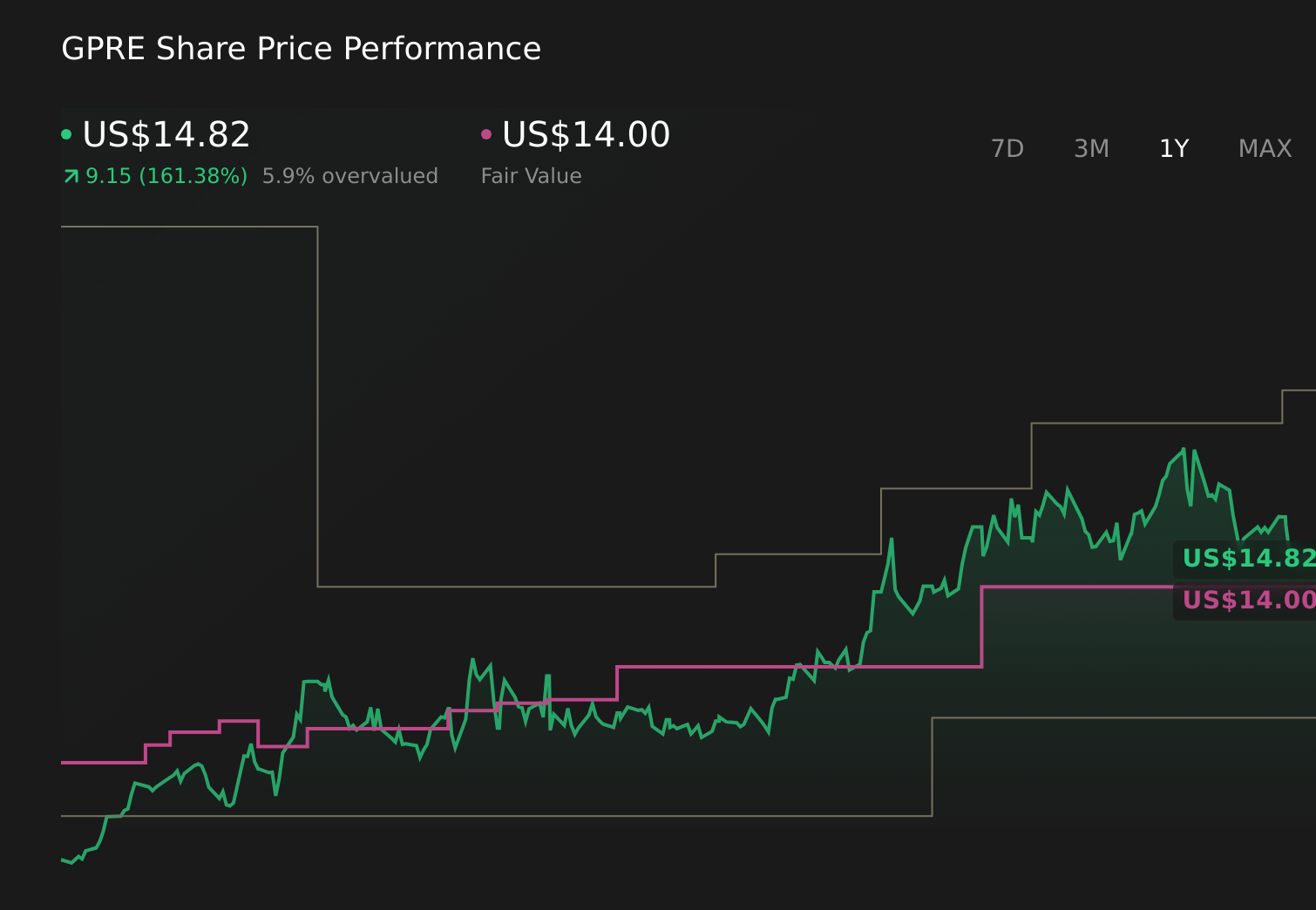

Green Plains' narrative projects $3.4 billion revenue and $116.3 million earnings by 2028. This requires 12.4% yearly revenue growth and a $268.2 million earnings increase from $-151.9 million today.

Uncover how Green Plains' forecasts yield a $14.00 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting Green Plains to reach about US$3.4 billion in revenue and US$116 million in earnings by 2028, so Sweeney’s insider buying and the AI overweight signals could either reinforce that upbeat view or prompt you to question it, especially if you worry about long term ethanol demand or execution on new projects.

Explore 3 other fair value estimates on Green Plains - why the stock might be worth 6% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Green Plains research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Green Plains research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Green Plains' overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.