Is Hershey’s New Tech-Focused Board Voice Reshaping Its Digital Edge and Risk Profile (HSY)?

Hershey Company HSY | 0.00 |

- Earlier this month, The Hershey Company appointed Joe Park, State Farm’s Executive Vice President and Chief Digital and Information Officer, to its Board effective June 29, 2026, with roles on the Audit and Finance and Risk Management Committees.

- At the same time, Hershey has been drawing investor attention for resilient demand, easing cocoa cost pressures, and earnings diversification through its growing salty snacks portfolio.

- We’ll now explore how Joe Park’s digital expertise and the recent investor spotlight on resilient demand interact with Hershey’s existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Hershey Investment Narrative Recap

To own Hershey, you need to believe its brands can keep demand resilient while the company manages cost pressures and broadens beyond chocolate. The key short term catalyst is whether easing cocoa costs and salty snacks can stabilize margins after recent EPS pressure. The biggest risk remains input cost and tariff volatility, which could further squeeze already lower profit margins. Joe Park’s board appointment does not materially change these near term drivers but may matter more over time.

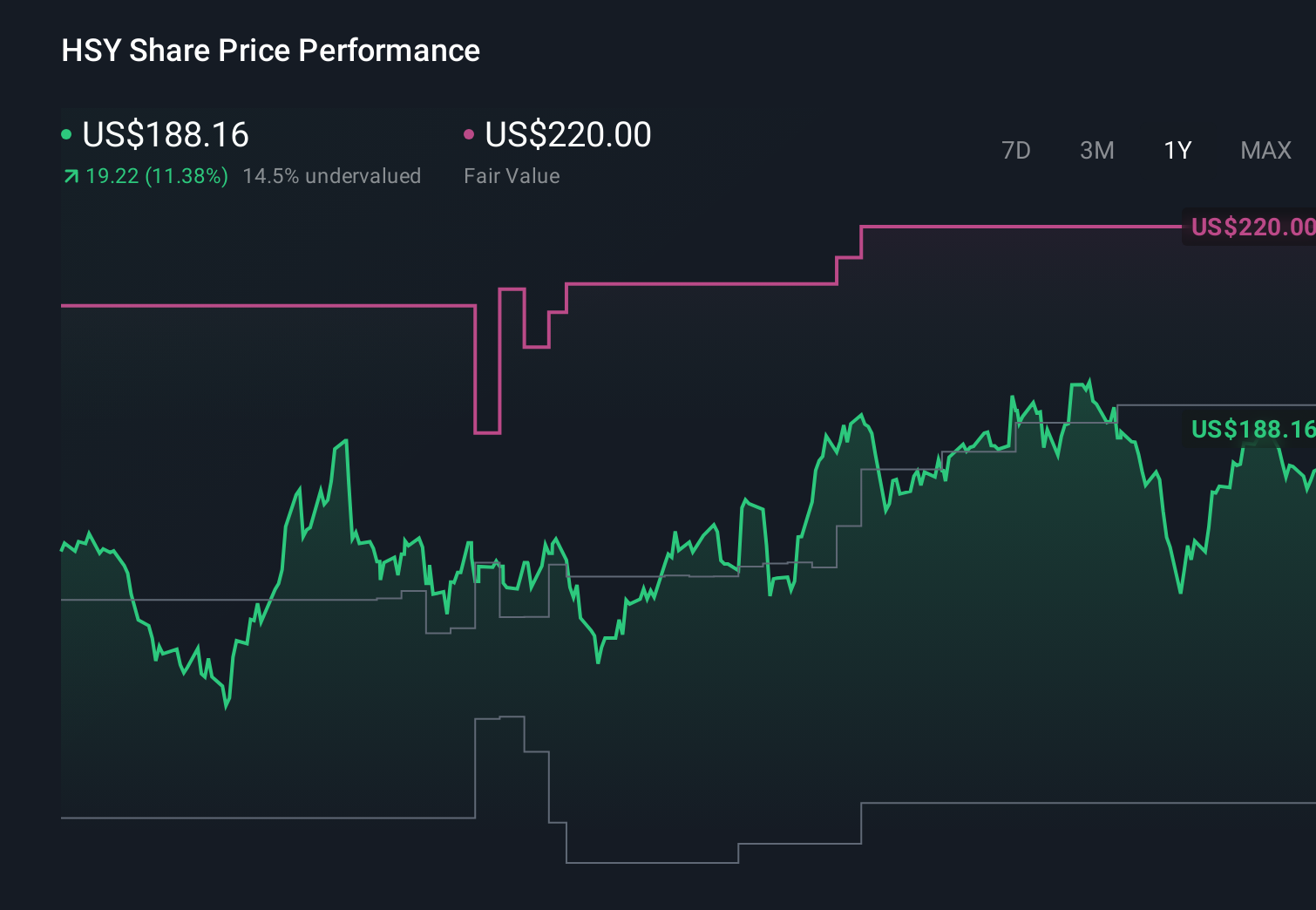

The most relevant recent announcement here is Hershey’s Q1 2026 report, with US$3,104.17 million in sales and diluted EPS of US$2.13. Those results frame how investors see demand resilience and cocoa cost relief today, and they are the baseline against which any benefit from new digital oversight on the Audit and Finance and Risk Management Committees will likely be assessed as the earnings story evolves.

Yet while cocoa costs are easing, investors should be aware that Hershey’s margin pressure and tariff exposure could still...

Hershey's narrative projects $12.9 billion revenue and $2.1 billion earnings by 2029. This requires 3.4% yearly revenue growth and about a $1.2 billion earnings increase from $883.3 million today.

Uncover how Hershey's forecasts yield a $227.78 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a much tougher picture for you, even with Joe Park joining the board, assuming only about 2.1 percent annual revenue growth and US$2.1 billion of earnings by 2029, so it is worth comparing that more cautious view with the idea that diversification and digital upgrades might gradually strengthen Hershey’s resilience.

Explore 6 other fair value estimates on Hershey - why the stock might be worth as much as 64% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hershey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hershey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hershey's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 32 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.