Is Houlihan Lokey (HLI) Quietly Reframing Its Advisory Edge Around GP-Led Secondaries Expertise?

Houlihan Lokey, Inc. Class A HLI | 0.00 |

- Earlier this month, Houlihan Lokey, Inc. said that Dan Buffery had joined its Capital Solutions Group in New York as a Managing Director, where he will help lead the firm’s North American GP-led secondaries advisory practice within Equity Capital Solutions.

- By adding an executive with deep GP- and LP-led secondaries experience at HarbourVest Partners and OPTrust, Houlihan Lokey is reinforcing its focus on growing capabilities in the expanding GP-led secondaries and infrastructure-related advisory space.

- We’ll now examine how Buffery’s hire to strengthen GP-led secondaries advisory could influence Houlihan Lokey’s existing investment narrative and growth drivers.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Houlihan Lokey Investment Narrative Recap

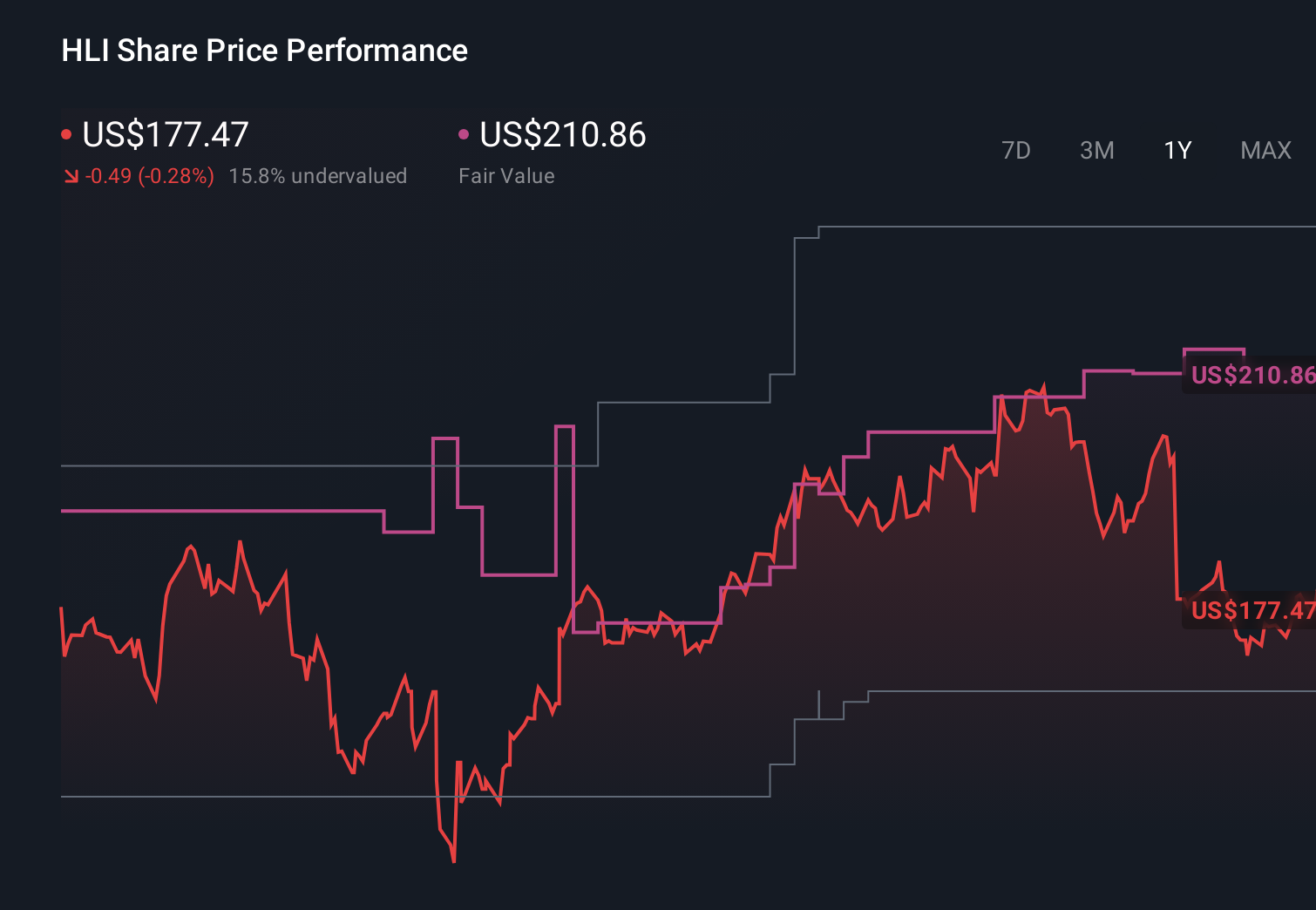

To own Houlihan Lokey, you have to believe in its ability to compound fee-based earnings across M&A, restructuring, and capital solutions while managing costs and senior talent risk. Buffery’s hire supports the firm’s dependence on experienced rainmakers and strengthens its GP led secondaries capability, but it does not materially change the near term swing factor, which remains overall deal activity versus elevated cost ratios.

The most relevant recent development alongside Buffery’s arrival is the May dividend increase to US$0.70 per share, following full year net income of US$425.7 million. Together, ongoing senior hires and a higher dividend suggest management is committing more resources to fee earning platforms while continuing to return cash, a combination that could matter if revenue growth slows or restructuring volumes normalize.

Yet beneath these positives, investors should still be aware of the concentration risk tied to a relatively small group of senior dealmakers and...

Houlihan Lokey's narrative projects $3.6 billion revenue and $583.7 million earnings by 2029. This requires 11.0% yearly revenue growth and about a $158 million earnings increase from $425.7 million today.

Uncover how Houlihan Lokey's forecasts yield a $172.50 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$3.4 billion and earnings of roughly US$601 million by 2029, and your view on Buffery’s hire might challenge that more pessimistic outlook built around technology pressure and fee compression.

Explore 2 other fair value estimates on Houlihan Lokey - why the stock might be worth as much as 31% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.