Is Hubbell (HUBB) Fairly Priced After Strong Growth In Revenue Earnings And Free Cash Flow Margins

Hubbell Incorporated HUBB | 0.00 |

Investor interest in Hubbell (HUBB) is being driven by its long term financial profile, with 10.2% annual revenue growth, 19.7% annual earnings per share growth supported by share buybacks, and expanding free cash flow margins.

Despite a recent pullback, with the share price down 16.1% over the past month and 12.5% over the past quarter, the stock still carries a 1 year total shareholder return of 19.9% and a 5 year total shareholder return of 161.9%. This points to longer term momentum that contrasts with the current cool off in sentiment around its US$460.98 share price.

If Hubbell’s grid and electrical exposure has caught your eye, it can be useful to see what else is moving in related areas through our 35 power grid technology and infrastructure stocks

So with Hubbell’s pullback, solid growth record, and a current share price of about US$461, are you looking at a rare opening in a quality grid supplier, or is the market already pricing in years of future growth?

Most Popular Narrative: 16% Undervalued

Hubbell’s most followed narrative pegs fair value at about $547 per share, which sits well above the recent $460.98 close and frames the current pullback against longer term assumptions.

The Utility Solutions segment is experiencing organic growth resurgence, particularly in grid infrastructure, supported by strong transmission and substation markets due to increasing grid modernization and electrification. This growth trend should drive higher future revenues.

Curious what underpins that higher fair value? The narrative leans on steady top line growth, firmer margins, and a richer earnings base several years out. The precise mix might surprise you.

Result: Fair Value of $547.15 (UNDERVALUED)

However, the picture can change quickly if cost inflation and tariff pressures squeeze margins, or if weaker grid automation demand weighs on the Utility Solutions segment.

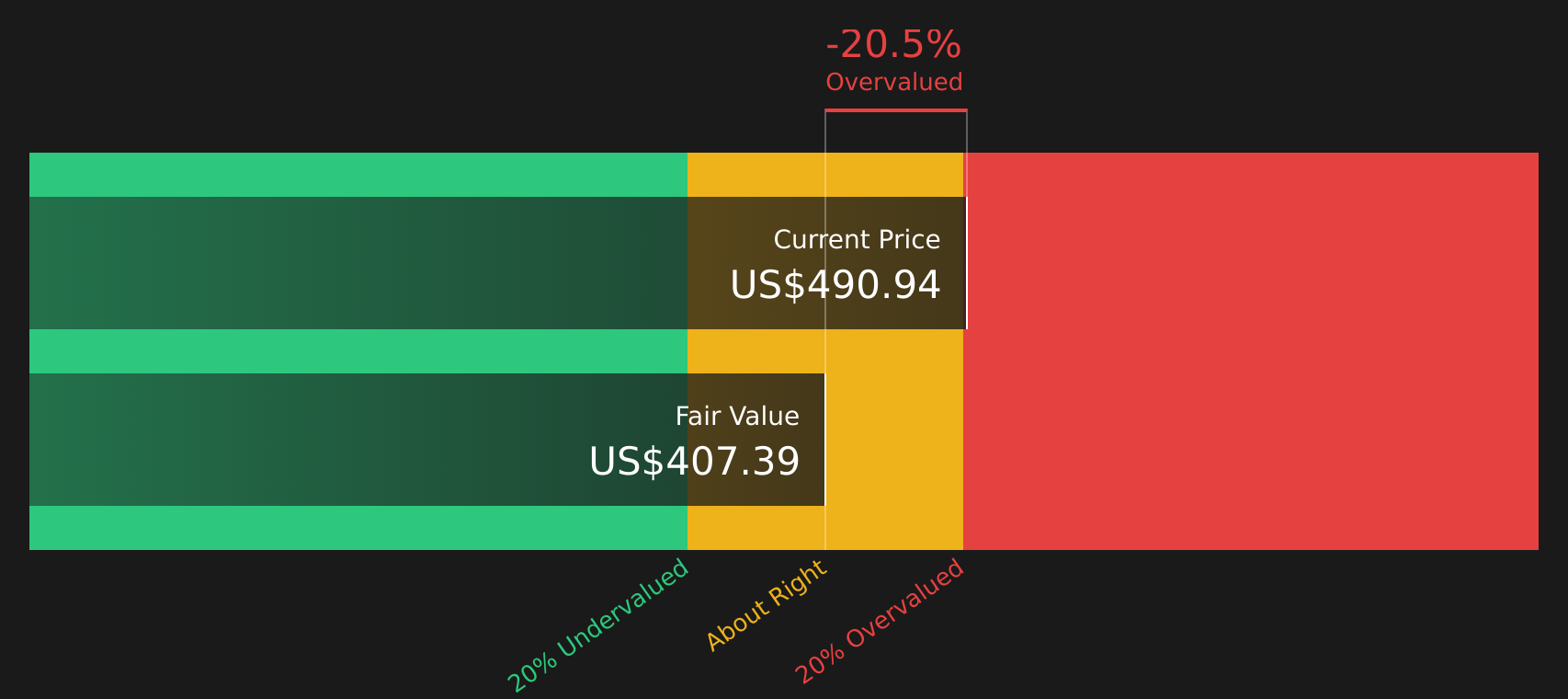

Another View: DCF Flags Overvaluation

While analysts see Hubbell as about 16% undervalued at a fair value of roughly $547 per share, the Simply Wall St DCF model tells a very different story. On that framework, the stock around $460.98 sits above an estimated future cash flow value of $338.77, which points to an overvalued outcome instead.

That gap matters because it raises a simple question for you to answer: do you trust the earnings-based fair value or the cash-flow-based view more for a business like this?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hubbell for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment, it helps to move fast, review the underlying data, and decide where you stand. To balance the upside story with the concerns on the table, take a closer look at the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop at one stock, you risk missing others that fit your style just as well, so give yourself options and broaden your opportunity set.

- Target potential upside by scanning for quality companies that look mispriced using the 53 high quality undervalued stocks.

- Strengthen your income stream by focusing on dependable payers filtered through the 10 dividend fortresses.

- Sleep easier by hunting for companies with resilient finances and lower risk profiles via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.