Is Ingersoll Rand’s (IR) M&A-Heavy Playbook Quietly Redefining Its Long-Term Investment Story?

Ingersoll Rand Inc. IR | 0.00 |

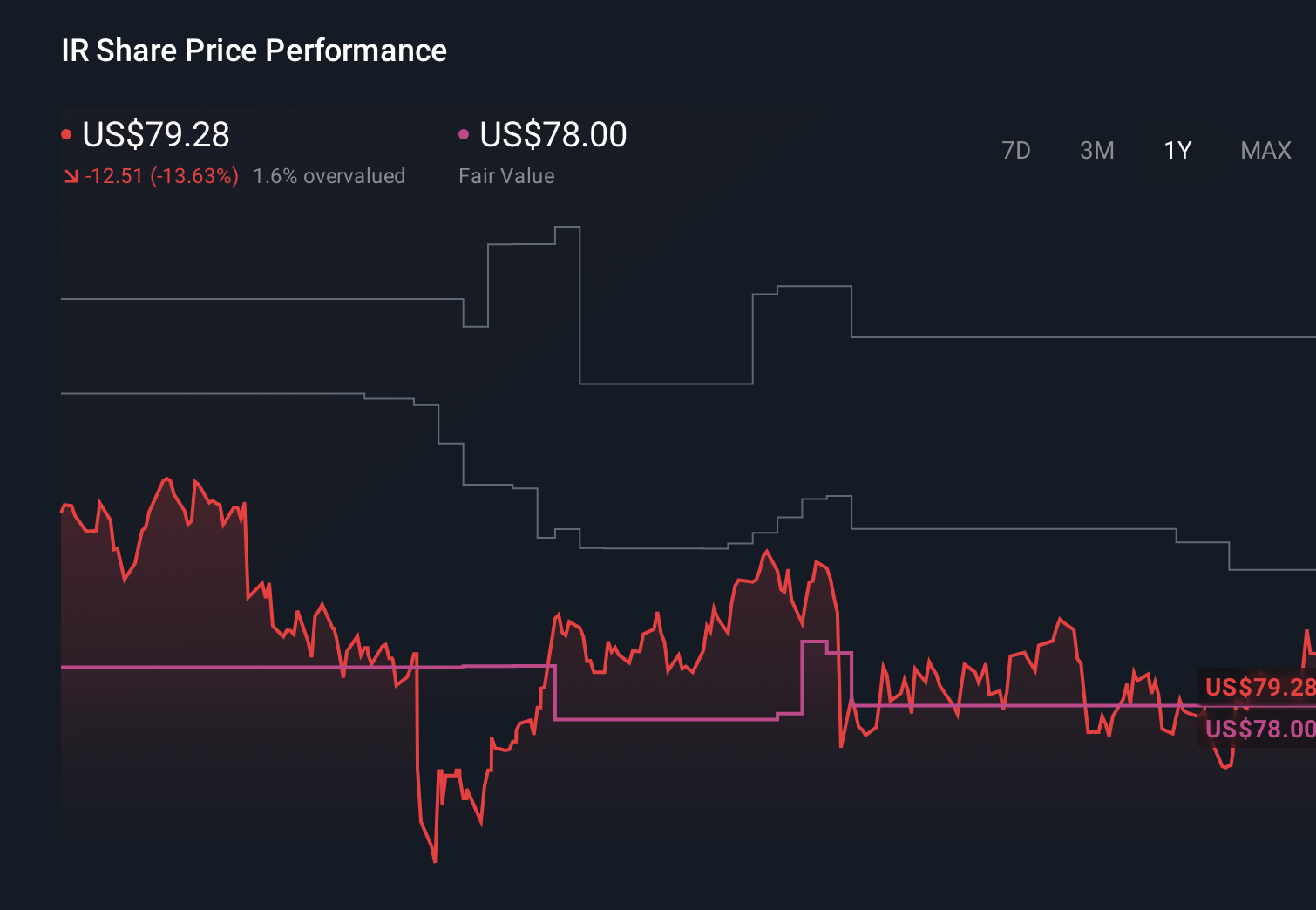

- In the past week, Ingersoll Rand Inc. reported first-quarter 2026 results that exceeded analyst expectations, with sales rising to US$1,847.2 million and net income edging up to US$192.1 million, while management reaffirmed full-year 2026 guidance and highlighted a continued disciplined focus on bolt-on acquisitions plus ongoing dividends and buybacks.

- Management’s emphasis on prioritizing mergers and acquisitions, backed by a funnel of more than 200 potential bolt-on targets and recent deals like Fox s.r.l., underlines how capital deployment is being used to expand core technologies and adjacent markets rather than relying solely on organic growth.

- We’ll now examine how Ingersoll Rand’s earnings beat and reaffirmed 2026 guidance could influence its investment narrative and future expectations.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to be comfortable with a story built around disciplined bolt-on acquisitions, steady capital returns, and exposure to industrial cycles. The latest earnings beat and reaffirmed 2026 guidance support that narrative in the near term, while the most important short term catalyst remains management’s ability to execute M&A without repeating past impairment issues. The biggest risk is that acquisition-heavy growth runs into integration or profitability challenges.

The reaffirmed 2026 revenue growth guidance of 2.5% to 4.5% is especially relevant here, because it frames how much room the company has to layer inorganic growth from its active M&A funnel over a relatively modest top line outlook. In this context, the ongoing US$0.02 per share quarterly dividend and continued buybacks look more like supporting features than primary drivers of the story, with bolt-on deals still at the center of future expectations.

Yet against this constructive picture, investors should also be aware of how quickly acquisition missteps or prolonged project delays could...

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029. This requires 5.0% yearly revenue growth and about an $813.0 million earnings increase from $587.0 million today.

Uncover how Ingersoll Rand's forecasts yield a $96.47 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting about US$8.8 billion in revenue and US$1.5 billion in earnings by 2028, which contrasts sharply with the more cautious consensus tied to today’s bolt-on driven guidance and shows how differently you might weigh the same M&A and expansion risks.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 21% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.