Is InterDigital's (IDCC) 2026 Guidance Quietly Rewriting Its Licensing-Led Investment Narrative?

InterDigital, Inc. IDCC | 0.00 |

- InterDigital, Inc. reported past first-quarter 2026 results with sales of US$205.42 million and diluted EPS of US$2.14, and issued second-quarter and full-year 2026 guidance alongside plans to present at four major investor conferences.

- The combination of softer earnings, detailed revenue and EPS guidance, and upcoming conference presentations gives investors fresh insight into InterDigital’s licensing, R&D, and AI priorities.

- We’ll now examine how InterDigital’s updated 2026 revenue and EPS guidance could reshape the company’s investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

InterDigital Investment Narrative Recap

To own InterDigital, I think you need to believe its licensing engine and R&D in wireless, video, and AI can keep converting patents into resilient, high-margin cash flows. The latest Q1 2026 results, with softer earnings and tighter full year guidance, put more focus on execution against that outlook and on how quickly new licenses and renewals can offset lumpier revenue, but they do not yet appear to fundamentally alter the core long term thesis or the biggest near term risk: earnings volatility tied to licensing timing.

Against that backdrop, the reaffirmed full year 2026 guidance of US$675 million to US$775 million in revenue and diluted EPS of US$5.77 to US$8.51 is especially important. It anchors expectations after a weaker quarter and gives investors a yardstick to assess whether upcoming investor conferences and licensing updates are moving the needle on the key catalyst of stabilizing recurring revenue versus the risk that lumpier deals and slower new agreements keep near term earnings choppy.

Yet despite the long term licensing visibility, there is a meaningful risk investors should be aware of if...

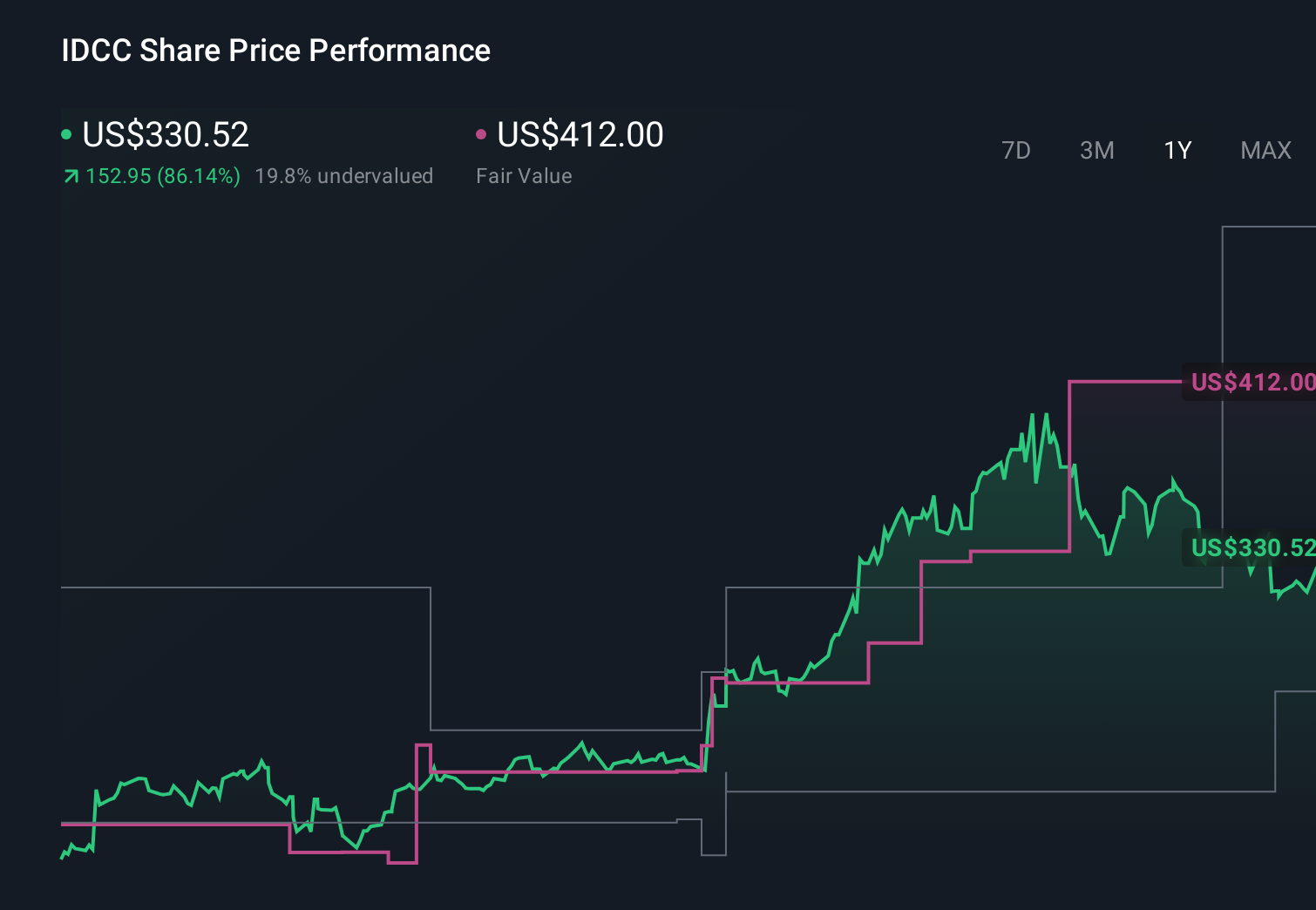

InterDigital’s narrative projects $1.0 billion revenue and $490.5 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 61% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts tell a more cautious story, even before this Q1 miss, assuming revenue only reaches about US$1.0 billion and earnings about US$504.9 million by 2029, which is far less generous than the consensus narrative and highlights how differently you and other investors might view today’s softer quarter, updated guidance, and the risk that legal and regulatory pressures could limit how much of InterDigital’s patent portfolio actually converts into...

Explore 6 other fair value estimates on InterDigital - why the stock might be worth 36% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.