Is International Paper’s Lowered EBITDA Outlook Reshaping the Turnaround Investment Case for IP?

International Paper Company IP | 0.00 |

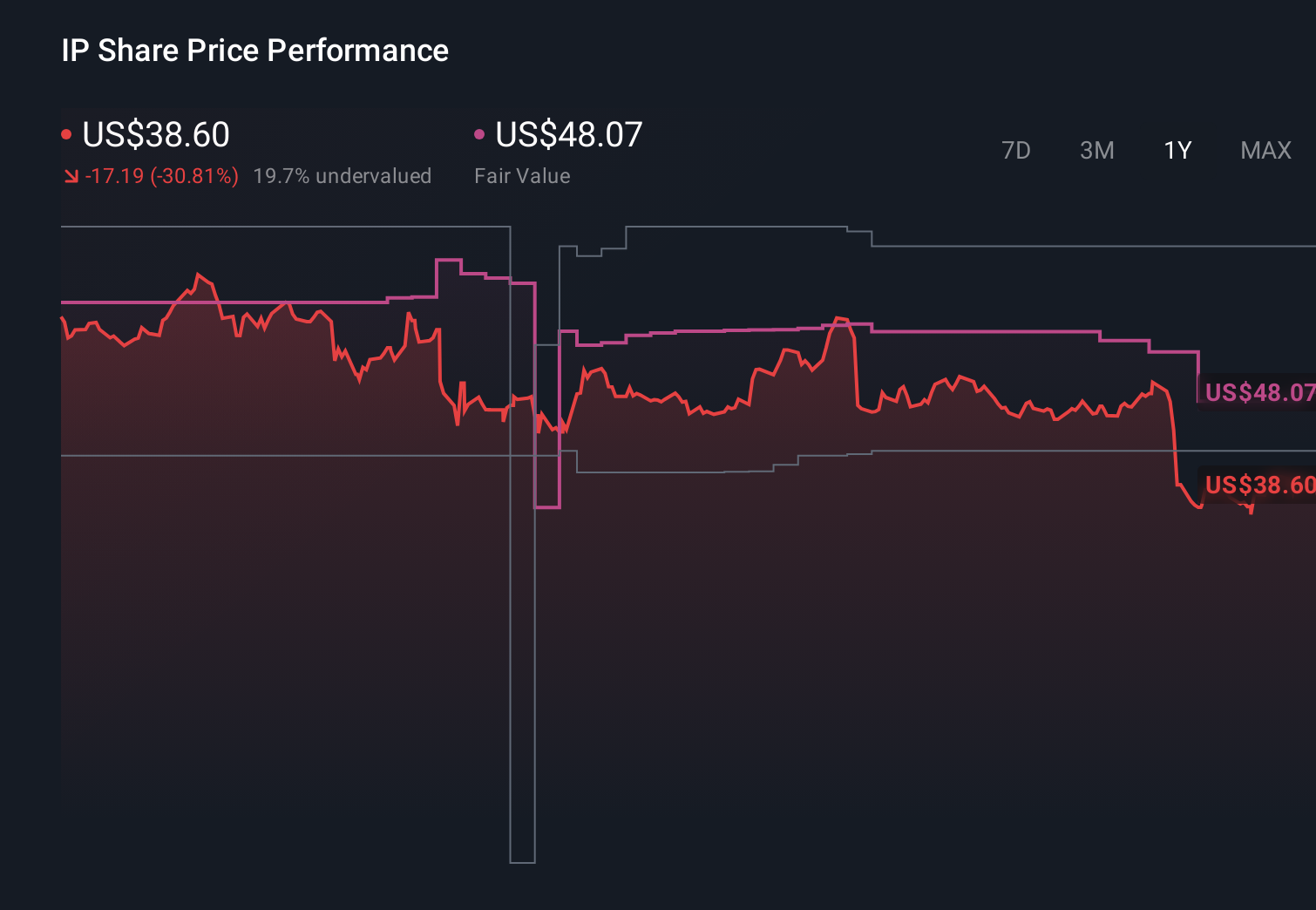

- In the past quarter, International Paper reported mixed Q1 2026 results, with higher net sales helped by acquisitions and volume gains, while cutting its full-year adjusted EBITDA guidance amid macroeconomic uncertainty and rising freight, energy, and restructuring costs.

- This combination of improving top-line momentum but a more cautious profit outlook highlights the tension between International Paper’s growth initiatives and the cost and execution challenges shaping its turnaround efforts.

- We’ll now examine how the lowered full-year EBITDA guidance affects International Paper’s existing investment narrative and expectations for operational improvement.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

International Paper Investment Narrative Recap

To own International Paper, you need to believe its fiber-based packaging focus and cost improvements can eventually outweigh current margin pressures from volatile freight, energy, and restructuring costs. The lowered full-year EBITDA guidance does matter here, because it directly challenges the near term catalyst of better profitability while reinforcing the biggest risk today: whether execution issues and unstable input costs keep eroding the benefits of volume gains and acquisitions.

The recent groundbreaking of a US$225,000,000 sustainable corrugated packaging facility in Rankin County ties directly into this tension. It supports the long term case for growth and efficiency in packaging, but it also adds to capital and execution demands at a time when the company is already dealing with mill reliability work, asset optimization, and the integration of past moves, all while trimming its earnings outlook.

But while International Paper is investing for the future, the combination of lower guidance and ongoing cost volatility is something investors should be aware of...

International Paper's narrative projects $26.2 billion revenue and $1.7 billion earnings by 2029. This requires 2.5% yearly revenue growth and a $4.3 billion earnings increase from -$2.6 billion today.

Uncover how International Paper's forecasts yield a $39.36 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about 2 percent annual revenue growth and US$1.8 billion in earnings by 2029, so this guidance cut may push that more pessimistic view even further or, if execution improves, prove too harsh.

Explore 4 other fair value estimates on International Paper - why the stock might be worth just $39.36!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your International Paper research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.