Is Iridium (IRDM) Pricing In Too Much Satellite Optimism After Oppenheimer’s Upgrade And Insider Moves?

Iridium Communications Inc. IRDM | 0.00 |

- In early June 2026, Oppenheimer upgraded Iridium Communications, citing growing confidence in its role within the expanding satellite connectivity and communications services market.

- At the same time, a cluster of routine tax-related insider share withholdings and debate over Iridium’s high earnings multiple highlighted the tension between enthusiasm for its technology footprint and concerns about how fully expectations are already reflected in the share price.

- Next, we’ll explore how Oppenheimer’s renewed confidence in Iridium’s satellite connectivity positioning may influence the company’s existing investment narrative.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Iridium Communications Investment Narrative Recap

To own Iridium today, you need to believe its satellite network, IoT offerings, and PNT services can keep attracting sticky, mission critical demand despite slowing service growth and a rich valuation. Oppenheimer’s upgrade and the 8% price jump sharpen that contrast: they may support the short term catalyst of rising interest in satellite connectivity, but they also amplify the biggest risk right now, which is how much optimism is already embedded in a high earnings multiple.

The most relevant recent update is Iridium’s Q1 2026 earnings, where revenue grew modestly to US$219.1 million while net income and margins slipped and management guided 2026 service revenue to be flat to up 2%. Against that backdrop, the upgrade and sharp share price move sit alongside routine tax related insider withholdings and an F valuation grade, reinforcing how much the near term story hinges on confidence in future growth rather than current financial momentum.

Yet behind the excitement over Iridium’s technology, investors should also be aware that...

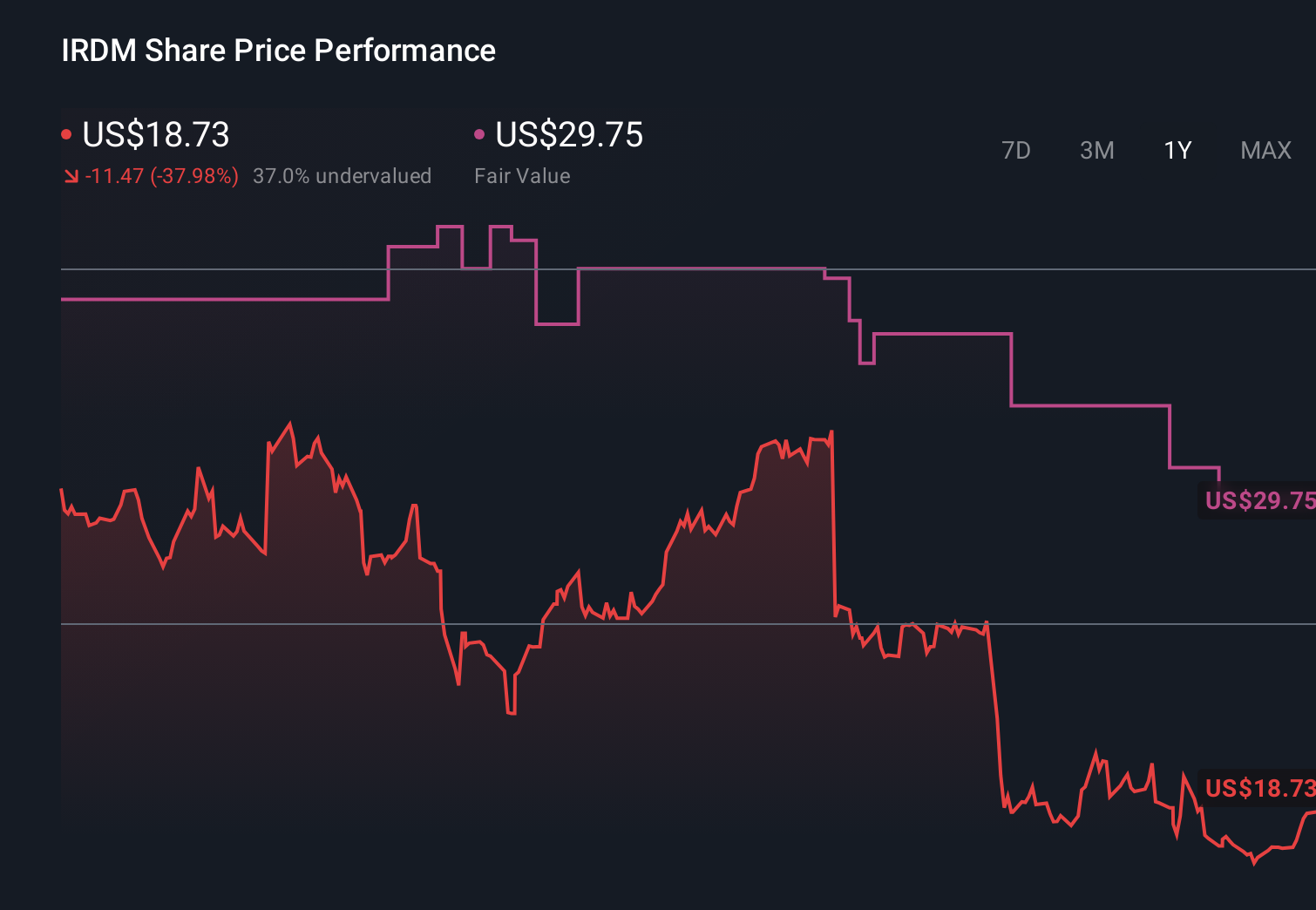

Iridium Communications' narrative projects $931.3 million revenue and $189.9 million earnings by 2029.

Uncover how Iridium Communications' forecasts yield a $30.38 fair value, a 36% downside to its current price.

Exploring Other Perspectives

Before this upgrade, the most optimistic analysts were already modeling revenue of about US$1.1 billion and earnings near US$211 million by 2029, so compared with consensus they paint a far more upbeat picture that could shift again as Iridium’s high P/E, insider activity, and new satellite connectivity catalysts play out.

Explore 7 other fair value estimates on Iridium Communications - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Iridium Communications research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Iridium Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Iridium Communications' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.