Is Iridium (IRDM) Recalibrating Its Growth Story With Flat 2026 Guidance Despite New Services?

Iridium Communications Inc. IRDM | 0.00 |

- In February 2026, Iridium Communications reported fourth-quarter 2025 results showing essentially flat quarterly revenue at US$212.94 million and lower net income of US$24.87 million, while full-year 2025 revenue rose to US$871.66 million and net income edged up to US$114.37 million.

- The company paired this with cautious 2026 guidance calling for flat to 2% total service revenue growth and Operational EBITDA of US$480 million to US$490 million, even as it highlighted new IoT, PNT, and NTN Direct offerings as longer-term growth avenues.

- We’ll now examine how Iridium’s flat-to-low service revenue guidance for 2026 affects its pre-existing investment narrative built on growth.

Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

Iridium Communications Investment Narrative Recap

To own Iridium Communications, you need to believe its specialized L‑band network, government ties, and emerging IoT and PNT services can offset pressures in legacy maritime and equipment revenue. The new 2026 outlook for flat to 2% service revenue growth tempers the near term growth story and makes IoT service momentum the key catalyst to watch, while intensifying competition in direct to device and satellite services remains the biggest risk.

Against this backdrop, the most relevant new development is Iridium’s plan to launch Iridium NTN Direct and an ASIC-enabled PNT platform in 2026, framed as a roughly US$200 million incremental revenue opportunity by the end of the decade. This matters because it directly targets the same IoT and PNT themes that underpin the long term growth thesis, even as the 2026 guidance reminds investors that these products may take time to translate into visible service revenue.

Yet behind Iridium’s cautious 2026 guide, investors should also be aware of the growing risk that mega constellations and terrestrial 5G could eventually compress pricing and...

Iridium Communications' narrative projects $982.9 million revenue and $174.8 million earnings by 2028. This requires 4.7% yearly revenue growth and about a $61.6 million earnings increase from $113.2 million today.

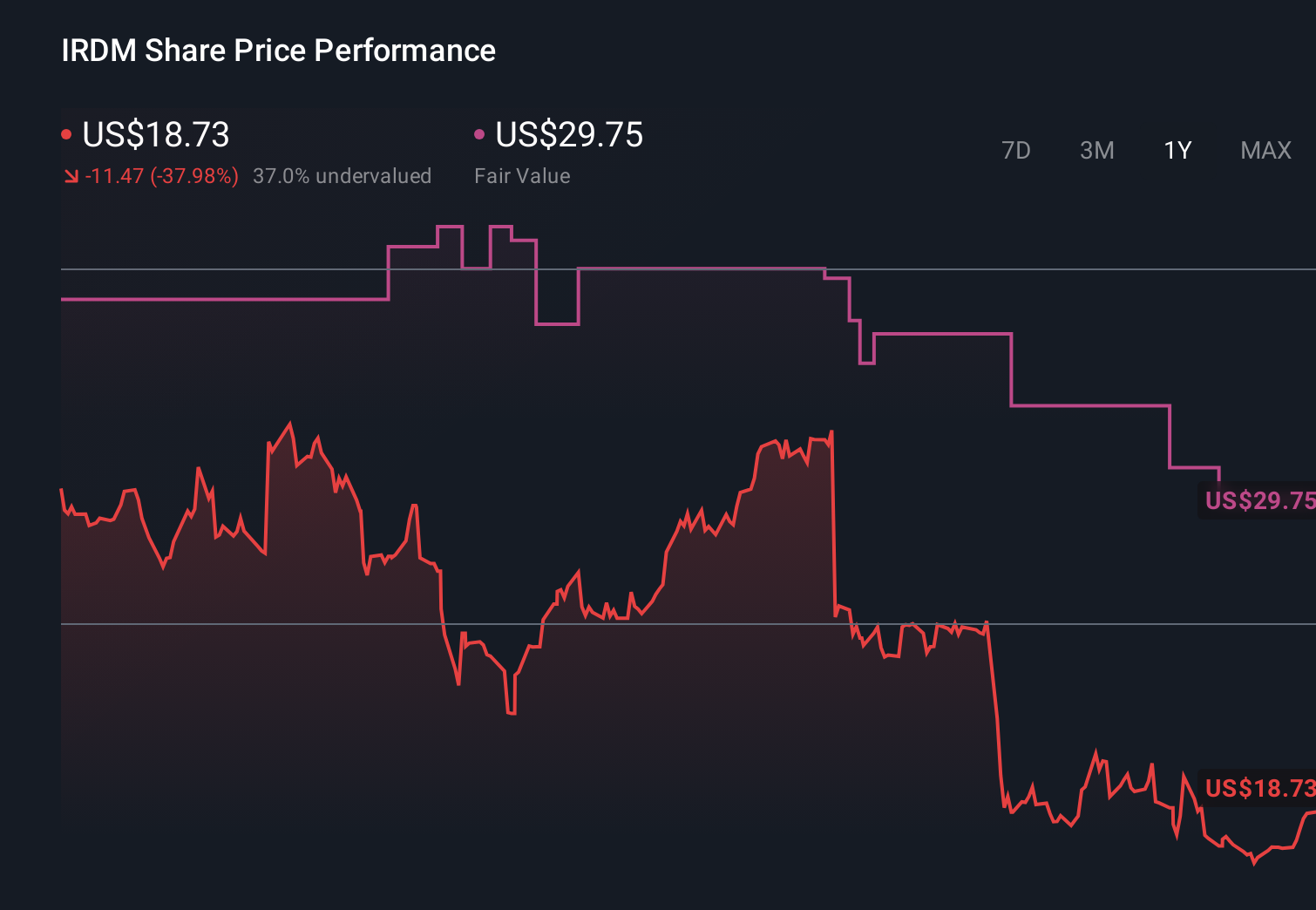

Uncover how Iridium Communications' forecasts yield a $29.75 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Before this report, the most optimistic analysts were modeling roughly US$1.0 billion of revenue and about US$195 million of earnings by 2028, which is far more upbeat than consensus, and assumes competitive pressures from mega constellations will not materially slow Iridium’s growth, a view that could easily shift in light of the flat 2026 service revenue guidance.

Explore 7 other fair value estimates on Iridium Communications - why the stock might be worth over 3x more than the current price!

Build Your Own Iridium Communications Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Iridium Communications research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Iridium Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Iridium Communications' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.